米国の飲料受託瓶詰め・充填:市場シェア分析、産業動向、成長予測(2025~2030年)

United States Beverage Contract Bottling And Filling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644370

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

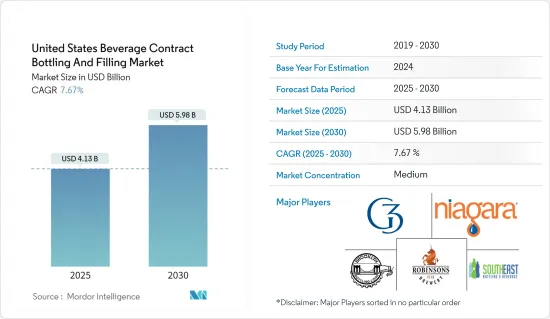

米国の飲料受託瓶詰め・充填市場規模は2025年に41億3,000万米ドルと推定・予測され、2030年には59億8,000万米ドルに達し、予測期間(2025~2030年)のCAGRは7.67%です。

米国の飲料受託瓶詰め・充填市場の成長は、主に製造企業の嗜好の変化によるもので、製造企業は通常、こうした特定の業務を第三者企業に委託しています。これは、製造業者がコストの最適化と本業に重点を置いているためです。ボトリングと充填の請負には、いくつかの利点があります。第一に、メーカーの運営コストを削減できます。多くの場合、ボトリングや充填作業を請負業者に委託し、機械や人件費を削減することで、運営コストを大幅に削減できると推定されます。

主要ハイライト

- 米国では、特に飲料製品の製造規制が急速に進化しています。このような厳しい規則や規範を満たすには、いくつかの検査や品質チェック作業が必要となります。ボトリングや充填作業をアウトソーシングすることで、こうした規制を満たすための慌ただしい作業は請負業者に委ねられるため、内製よりも請負を好むメーカーが増えています。さらに、この産業は急速に成長しており、多くの新製品や新技術が導入されています。そのため、企業は変化する顧客のニーズに応えるため、常に最新の情報を入手する必要があります。

- Admiral Beverage Corp.は、米国西部で最大の炭酸飲料(CSD)サプライヤーです。山間部、西部諸州、アラスカにまたがる複数のディストリビューターに炭酸飲料、スティル飲料、ボトルウォーター、ファウンテンミックスを供給する3つの大規模な施設に成長しました。Admiral Beverage Corp.は、ベブコープのMicrO2システムを採用することで、脱気を簡素化し、ブレンドを最適化し、充填と切り替えを迅速化しました。このシステムは溶存酸素(DO)を制限し、泡立ちを抑えることで、ラインの高速化を実現しています。速度が速くなれば、スループットが向上し、単位あたりのコストが減少し、原料を冷蔵する必要がなくなるため、エネルギーコストが削減されます。

- 米国では毎年3,000種類以上の新しい飲料製品が誕生しており、飲料のボトリングや充填を請け負う施設の需要は高いです。2020年2月、Big Beverages Contract Manufacturing(BBCM)は、ノースカロライナ州に飲料の共同充填施設を新設すると発表しました。新施設では、BBCMはまず毎分1,200缶の生産が可能な高速缶ライン1本からスタートし、今後18ヶ月で2本目、3本目のラインを追加する計画です。BBCMは、国内と地域の大口顧客向けに様々な缶飲料製品を提供する計画です。

- 米国に本社を置くHCI Equity Partnersが支援するMSI Expressは、Power Packagingを買収しました。MSI Expressは、保存可能な人間向け食品やペットフードのセグメントで、有名ブランドの受託包装や受託製造サービスを提供しています。Powerはまた、MSI Expressを粉末飲料、スープ、ベース、飲料ミックス、飲食品、コーヒー、紅茶などのカテゴリーにも参入させています。パワー包装社は、シカゴ郊外に2ヶ所、ウィスコンシン州に1ヶ所、テキサス州に1ヶ所の計4ヶ所を拠点としています。無菌飲料充填、スティック包装、瓶や缶への充填などの機能を追加することで、様々な企業にサービスを提供しています。

米国の飲料受託瓶詰め・充填市場動向

ビールが大きなシェアを占める見込み

- ビールは米国で最も好まれるアルコール飲料です。米国の消費者の大半はライトビールを好みます。通常のビールとは対照的に、こタイプはアルコール度数とカロリーが抑えられています。小規模で独立系ビール醸造所は、消費者の嗜好が進化し、飲料市場が競合し成熟していく中で、革新と繁栄のための新たな方法を見出しながら、全米の重要な地域社会に貢献し続けています。

- ビールメーカーが初めて事業を立ち上げたり、規模を拡大し始めたりする際には、充填機を購入するか、レンタル充填ラインや受託充填ソリューションを選択することになります。適切な充填機を見つけるのは複雑で、ビール会社に大きな問題を引き起こす可能性がありました。

- 異なる充填機は異なる液体粘度に対応できるが、ビールは粘度や包装によって充填要件が異なります。こうした理由から、米国では多くの企業が瓶詰め・充填の受託を選択しており、瓶詰め・充填の最大効率化に大きく貢献しています。

- 2023年、米国のビール生産量と輸入量は合わせて5%減少しました。同時に、クラフトビールメーカーの数量は1%減少し、小規模・独立系ビールメーカーの市場シェアは13.3%になった、ビール酒造組合は発表しています。ビール数量が包装販売からバーやレストランに戻ったことが、販売額増加の主要要因です。

ボトル入り飲料水は大幅な成長が見込まれる

- ボトル入り飲料水は米国で最も急成長している飲み物であり、米国人は毎年何10億米ドルもかけて購入しています。IBWA(Beverage Marketing Corporation)は、ボトル入り飲料水は最も健康的な包装飲料であり、米国が肥満と糖尿病の増加率に直面しているため、特に重要であると主張しています。継続的な成長と消費量の増加にもかかわらず、ボトル入り飲料水は包装飲料の中で最も水とエネルギーの使用量が少ないです。完成品1リットルに必要な水の量はわずか1.39リットル、エネルギーの量は平均0.21メガジュールです。災害救援には欠かせないです。さらに、この産業が年間を通じて強く、存続可能でなければ、非常時に利用することはできないです。

- 米連邦緊急事態管理庁(FEMA)は、非常時のために1日1人当たり最低1ガロンの水を用意しておくことを推奨しています。ボトル入り飲料水の購入・保存は、必要なときに十分な供給量を確保できる安全で便利な方法であり、これがボトル入り飲料水の需要を押し上げ、ひいては米国のボトル詰め・充填受託市場にプラスの影響を与えると予想されます。

- 国際ボトルウォーター協会が2024年5月に発表したデータによると、米国では2023年に159億4,000万ガロンのボトル入り飲料水が販売されました。ここ数年、同国のボトル入り飲料水の数量は毎年大幅に増加しています。

- さらに、米国食品医薬品局はボトル入りの水を食品として規制しています。FDAは、ボトル入り飲料水メーカーに対し、認定検査所による水質検査結果の使用や報告を義務付けていないです。しかしFDAは、ボトルウォーターのラベルに成分や栄養価の情報を記載することを義務づけています。

- 最近、Nestleは米国におけるボトル入り飲料水事業の大半の売却を検討しました。この事業はスイスの食品大手Nestleの売上高のかなりの割合を占めており、環境保護団体から批判を浴びています。環境保護活動家たちは、少なくとも水道水が飲める国では、ボトル入り飲料水を店まで運ぶのにエネルギーが必要なため、ボトル入り飲料水は本質的に無駄が多いと見なしています。このような事例は、国内のボトル入り飲料水の受託ボトリングと充填市場に悪影響を及ぼす可能性があります。

米国の飲料受託瓶詰め・充填産業概要

米国の飲料受託瓶詰め・充填市場は半固定化されており、Brooklyn Bottling Group、G3 Enterprises Inc.、Southeast Bottling & Beverages、Niagara Bottling LLCのような重要な参入企業が存在します。国内企業は市場シェアを拡大するために、複数の提携や合併を行っています。

- 2024年1月、アルミニウム平板圧延製品の世界的リーダーであり、アルミニウムリサイクル最大手のNovelis Inc.は、Ardagh Metal Packaging USA Corp.との新規契約を発表しました。この契約により、Novelisは飲料用アルミ包装シートをArdagh Metal Packaging USA Corp.に供給することになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 米国飲料産業におけるCOVID-19の影響

- 市場促進要因

- 小規模飲料メーカー向けのボトラー契約による設備投資メリット

- 新時代の飲料とクラフトビールセグメントからの需要の高まり

- コンタクト包装ャーのビジネスモデルが徐々に変化し、デザインと配置を含むコンサルタティブ・アプローチに移行

- 市場課題

- 製造プロセスにおける柔軟性と敏捷性の欠如と規制の動的性質

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 飲料タイプ別

- ビール

- 炭酸飲料・果実飲料

- ボトル入り飲料水

- その他の飲料タイプ(スポーツドリンク)

第6章 競合情勢

- 企業プロファイル

- Brooklyn Bottling Group

- CSD Co-Packers Inc.

- Southeast Bottling & Beverages

- G3 Enterprises Inc.

- Robinsons Breweries(Frederic Robinson Limited)

- Western Innovations Inc.

- Niagara Bottling LLC

第7章 市場の将来展望

目次

The United States Beverage Contract Bottling And Filling Market size is estimated at USD 4.13 billion in 2025, and is expected to reach USD 5.98 billion by 2030, at a CAGR of 7.67% during the forecast period (2025-2030).

Growth in the US beverage contract bottling and filling market is mainly influenced by the changing preferences of manufacturing firms, which usually outsource these specific activities to third-party players. This is because manufacturers focus on cost optimization and their core business. Contract bottling and filling provide several advantages. Firstly, it reduces the operational costs of the manufacturers. In many cases, it is estimated that operational costs can be reduced significantly through outsourcing bottling and filling activities to contract companies and decreasing the costs of machines and labor.

Key Highlights

- The manufacturing regulations, especially for beverage products in the United States, are evolving rapidly. Meeting such stringent rules and norms requires several inspection and quality check operations. By outsourcing bottling and filling activities, the hectic task of meeting such regulations is passed on to the contracting agency, motivating more manufacturers to prefer contracting over in-house manufacturing activities. Moreover, the industry is rapidly growing, introducing many new products and technologies. Therefore, companies need to stay updated to meet customers' changing needs.

- Admiral Beverage Corp. is among the largest suppliers of carbonated soft drinks (CSD) in the western United States. It has grown to three extensive facilities supplying carbonated and still beverages, bottled water, and fountain mixes to multiple distributors throughout the mountain, western states, and Alaska. Adopting Bevcorp's MicrO2 system, Admiral Beverage simplified deaeration, optimized blending, and sped up filling and changeovers. The system limits dissolved Oxygen (DO) to reduce foaming, which allows the line to run faster. Faster speeds result in more throughput, decreasing costs per unit, and the correlating reduction in energy costs by not having to refrigerate ingredients.

- With over 3,000 new beverage products being created each year in the United States, beverage contract bottling and filling facilities are in high demand. In February 2020, Big Beverages Contract Manufacturing (BBCM) announced its new beverage co-packing facility in North Carolina. In its new facility, BBCM will begin with one highspeed can line capable of producing 1,200 cans per minute, with plans to add lines two and three over the next 18 months. BBCM plans to provide various canned beverage products for large national and regional customers.

- MSI Express, backed by HCI Equity Partners, headquartered in the United States, acquired Power Packaging. MSI Express provides contract packaging and contract manufacturing services for well-known brands in the shelf-stable human and pet food space. Power also brings MSI Express into categories such as powdered beverages, soups, bases, beverage mixes, food service beverages, coffees, and teas. Power Packaging has four locations: two outside Chicago, one in Wisconsin, and one in Texas. It serves various companies by adding capabilities such as aseptic beverage filling, stick packaging, and filling of jars and cans.

United States Beverage Contract Bottling And Filling Market Trends

Beer is Expected to Hold Significant Share

- Beer is the most favored alcoholic beverage in the United States. The majority of U.S. consumers showed a preference for a light beer. In contrast to regular beer, this variety has reduced alcohol content and calories. Small and independent breweries continue to be critical contributors to significant communities across the country, finding new ways to innovate and thrive amid evolving consumer preferences and a competitive and maturing beverage market.

- As brewers first launch their operations or begin to grow larger, they can either buy their filling machines or opt for rented filling lines or contract filling solutions. Finding the right filling machinery was complex and could cause significant trouble for beer companies.

- Different filling machines could handle different liquid viscosities, whereas beer has varying filling requirements depending on viscosity and packaging. For these reasons, many companies in the United States are opting for contract bottling and filling, which significantly helps the companies to provide maximum efficiency in bottling and packing.

- In 2023, U.S. beer production and imports collectively dipped by 5%. Concurrently, craft brewer volume sales saw a 1% decline, propelling the market share of small and independent brewers to 13.3%, according to the Brewers Association. The return of beer volume from packaged sales to bars and restaurants was the main factor in the larger dollar sales increase.

Bottled Water is Expected to Witness Significant Growth

- Bottled water is the fastest-growing drink choice in the United States, and Americans spend billions of dollars each year to buy it (Beverage Marketing Corporation). IBWA claimed that bottled water is the healthiest packaged beverage and is particularly crucial as the United States is faced with increased rates of obesity and diabetes. Despite continued growth and increased consumption, bottled water uses the least amount of water and energy of any packaged beverage. One liter of finished product requires only 1.39 liters of water and 0.21 megajoules of energy on average. It is critical in disaster relief. Furthermore, it can only be available in times of emergency if the industry is strong and viable all year.

- The Federal Emergency Management Agency (FEMA) recommends that one should have a minimum of 1 gallon of water per person within a day available for emergencies. Buying and storing bottled water is a safe and convenient way to ensure an adequate supply is available when needed, and this is expected to boost the demand for bottled water, which, in turn, is expected to positively impact the contract bottling and filling market in the United States.

- According to data published in May 2024 by the International Bottled Water Association, 15.94 billion gallons of bottled water were sold in the United States in 2023. Over the last few years, the country's bottled water sales volume has increased each year significantly.

- Furthermore, the US Food and Drug Administration regulates bottled water as a food product. The FDA does not require bottled water companies to use or report water quality testing results from certified laboratories. The FDA does require ingredient and nutritional information on bottled water labels.

- Recently, Nestle considered selling most of its bottled water operations in the United States. That business accounts for a significant share of the Swiss food giant's sales and has drawn criticism from environmental groups. Environmental activists regard bottled water as inherently wasteful, at least in countries with drinkable tap water, because of the energy required to transport it to the store. Instances such as this may negatively affect the bottled water contract bottling and filling market in the country.

United States Beverage Contract Bottling And Filling Industry Overview

The US beverage contract bottling and filling market is semiconsolidated, with significant players such as Brooklyn Bottling Group, G3 Enterprises Inc., Southeast Bottling & Beverages, and Niagara Bottling LLC occupying the majority of the market's share. The companies in the country are forming multiple partnerships and mergers to increase their market share.

- January 2024: Novelis Inc., a global leader in flat-rolled aluminum products and the largest aluminum recycler, announced a new contract with Ardagh Metal Packaging USA Corp. The agreement entails Novelis supplying aluminum beverage packaging sheets to Ardagh Metal Packaging USA Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Impact of COVID-19 on the US Beverage Industry

- 4.3 Market Drivers

- 4.3.1 CapEx Benefits Offered by Contract Bottlers for Small-scale Beverage Manufacturers

- 4.3.2 Rise in Demand From New-age Drinks and Craft Beer Segment

- 4.3.3 Gradual Change in the Business Model of Contact Packagers Toward a Consultative Approach Involving Design and Placement

- 4.4 Market Challenges

- 4.4.1 Lack of Flexibility and Agility in Manufacturing Processes and Dynamic Nature of Regulations

- 4.5 Value Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Beverage Type

- 5.1.1 Beer

- 5.1.2 Carbonated Drinks and Fruit-based Beverages

- 5.1.3 Bottled Water

- 5.1.4 Other Beverage Types (Sport Drinks)

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Brooklyn Bottling Group

- 6.1.2 CSD Co-Packers Inc.

- 6.1.3 Southeast Bottling & Beverages

- 6.1.4 G3 Enterprises Inc.

- 6.1.5 Robinsons Breweries (Frederic Robinson Limited)

- 6.1.6 Western Innovations Inc.

- 6.1.7 Niagara Bottling LLC

7 FUTURE OUTLOOK OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日