作業指示管理-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Work Order Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1643194

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

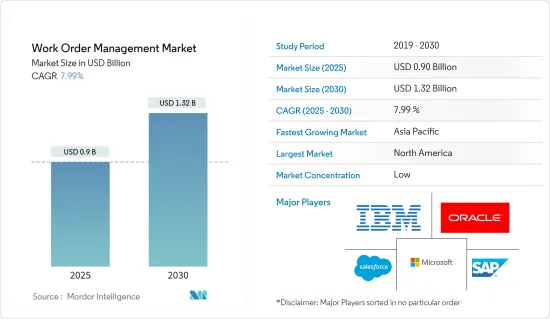

作業指示管理市場規模は2025年に9億米ドルと推定され、予測期間(2025~2030年)のCAGRは7.99%で、2030年には13億2,000万米ドルに達すると予測されます。

世界の企業はデジタル変革への動きを強めており、保守・管理を監督するためにさまざまなソリューションを採用しています。

主要ハイライト

- 作業指示管理は、企業の保守、設置、修理作業のスケジュール、計画、追跡、管理です。コスト削減、機器のダウンタイム削減、オペレーションの最適化により、世界中の施設のデジタル化が進んでいます。作業指示管理システムを採用することで、企業は予防保守を選択できるようになり、サービス依頼やリアルタイムの最新情報の入手が容易になります。

- 同市場は、メンテナンス業務の合理化、資産パフォーマンスの向上、全体的な業務効率の最適化のために、作業指示管理ソフトウェアを採用する組織の普及が進んでいることに起因する、消費者需要の増加に煽られた上昇軌道によって著しい大幅な成長を遂げています。

- さらに、管理された作業指示、より良いプロジェクトの実行、受注を管理し一元的に追跡するための業種を超えた企業間の要件の増加、作業指示管理システムのためのクラウドベースのソリューションへのフォーカスの増加は、市場の成長を促進する主要要因です。

- しかし、業務発注管理市場の成長には、既存システムとの統合の複雑さ、データセキュリティの懸念、熟練人材の不足などの課題があります。進化する技術のシームレスな統合によってこれらの課題に対処することで、市場の成長は加速すると予想されます。

- COVID-19の流行は、調査対象市場にさまざまな影響を与えました。リモートワークへの移行は、作業指示書へのアクセスと更新に課題をもたらし、生産性とコミュニケーションに影響を与えました。接客業や旅行業などの産業は景気後退に見舞われ、こうしたソリューションに対する需要の減少につながりました。一方、クラウドベースの業務指示管理ソリューションの採用により、リモートアクセスやコラボレーションが容易になり、製造業、eコマース、医療などの産業では、分散チームの管理や事業継続性の確保に不可欠なものとなりました。

作業指示管理市場の動向

製造業で大きな導入が見込まれる

- 作業指示管理は、製造業務の不可欠な一部となり、生産タスクの実行、リソースの割り当て、スケジューリングを導きます。しかし、デジタル化が進むにつれて、製造業は作業指示管理を合理化・最適化する技術を採用するようになっています。

- 製造産業では、作業指示管理ソリューションの導入が急増しています。この動向の背景には、効率性の向上、コストの最適化、最終的には有効性の向上という、さまざまな要因があります。

- インダストリー4.0は、レガシーシステムからスマートコンポーネントや機械に至るまで産業を変革し、デジタル工場と接続された工場や企業のエコシステムの開発を促進しています。インダストリー4.0は、OEMが自社の事業全体でIoTを採用するよう説得しています。製造産業でIoTが提供するメリットは、機械の稼働率向上、予知保全と生産、データ分析、モニタリング、自動化、コストメリットなど、採用率を高める原動力となっています。

- さらに2022年11月、中国工業情報化省は新たに3つの国家製造イノベーションセンターを承認しました。また、これらのセンターは重要な汎用技術に焦点を当て、これらの産業における技術研究開発を後押しするとしています。また、同省は、製造業の主要セグメントの質の高い開発に重要な支援を提供するため、技術革新を求める能力を強化するよう、新たな製造革新センターを指導すると述べました。

- 製造業生産性革新同盟(MAPI)財団の報告書によると、2025年までに、製造業は生産スケジューリングと制御のためのデジタル技術への投資を46%増加させると予測されています。この統計は、作業指示と製造プロセスの将来にとってデジタル変革の重要性が高まっていることを浮き彫りにしています。

北米が市場を独占する見込み

- IoT技術は、特に米国などの先進国において、製造部門の労働力不足を克服しつつあります。米国の連邦政府と民間組織は、米国の産業基盤を拡大するためにインダストリー4.0のIoT技術に投資しています。

- AI、IoT、スマートデバイス、3Dプリンティングなど、いくつかの技術はすでに米国の主要工場の業績指標を伸ばしています。また、同地域の政府は、ロボット市場における最新技術の成長を支援するイニシアチブをとることで、ロボット工学の採用を促進しています。

- 例えば、米国連邦政府は、国内の国産ロボット製造能力を強化し、このセグメントの研究活動を後押しするため、国家ロボット工学イニシアチブ(NRI)プログラムを開始しました。ワークオーダー管理はサプライチェーンのリスクを低減し、インバウンド・アウトバウンドのロジスティクスを完全に調査することで、輸送中の製品の品質と真正性を保証します。

- さらに、労働統計局によると、2023年2月現在、米国の建設部門の雇用者数は約800万人で、2021年の729万人から増加しています。このような建設労働力需要の高まりが、現場作業員のウェアラブル端末需要を押し上げ、市場成長を加速させています。

- 北米地域は、IBM、Microsoft、Oracle、Salesforceなど複数の大手ベンダーが存在し、技術採用における優位性と相まって、作業指示管理市場を独占すると予想され、様々な産業に作業指示管理ソリューションを提供しています。

作業指示管理産業概要

作業指示管理市場の競合情勢は、セールスフォース、IBM、Microsoft、SAP SE、Oracleなど複数のソリューションプロバイダーが世界中に存在するため、半固体化しています。市場参入企業は、市場での存在感を高めるために、製品の発売、M&A、提携などの戦略的イニシアチブを確認しています。

2024年2月-Gootenは、オンデマンド生産用に設計された作業指示管理プラットフォーム、OrderMeshTMを発表。このプラットフォームは、小売業者、製造業者、eコマースブランド、市場が、商品提供の幅を広げ、注文処理を合理化し、オンデマンドサプライチェーンの運用の複雑さとコストを大幅に削減できるよう支援することを目的としています。

2023年9月、英国を拠点とするソフトウェア会社Everfieldは、電気通信、公益事業、インフラ部門に特化した作業指示管理ソフトウェアプロバイダであるDepotnetを買収しました。買収により、DepotnetはEverfieldのサポートとリソースを活用し、成長とイノベーションに投資できるようになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の産業への影響評価

第5章 市場力学

- 市場促進要因

- 現場作業員におけるモバイルとウェアラブルデバイスの採用

- より良いプロジェクト遂行のための作業最適化に対する企業の傾向

- 市場抑制要因

- 現場作業員の専門知識不足

第6章 市場セグメンテーション

- コンポーネント別

- ソリューション

- サービス別

- 導入形態別

- オンプレミス

- クラウド

- エンドユーザー産業別

- 製造業

- 運輸・物流

- エネルギー公益事業

- 医療

- BFSI

- 通信・IT

- その他

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Salesforce.com, Inc.

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- IFS AB

- Infor Inc.

- Hippo CMMS

- ServiceMax, Inc.

- Innovapptive Inc.

- eMaint Enterprises, LLC

第8章 投資分析

第9章 市場の将来

目次

The Work Order Management Market size is estimated at USD 0.90 billion in 2025, and is expected to reach USD 1.32 billion by 2030, at a CAGR of 7.99% during the forecast period (2025-2030).

Enterprises worldwide are increasingly moving towards digital transformation, adopting various solutions to oversee maintenance and management.

Key Highlights

- Work order management is scheduling, planning, tracking, and managing work orders for a business's maintenance, installation, and repair tasks. Reducing costs, equipment downtime, and optimizing operations are augmenting the digitalization of facilities across the globe. Adopting a work order management system allows enterprises to opt for preventive maintenance, making it easy to place service requests and gain real-time updates.

- The market is experiencing substantial growth marked by a rising trajectory fueled by increased consumer demand attributed to the growing prevalence of organizations embracing work order management software to streamline maintenance operations, enhance asset performance, and optimize overall operational efficiency.

- Furthermore, the increasing requirement to have managed work orders, better execution of projects, increasing requirement among businesses across industries to manage and centrally track orders and increasing focus towards cloud-based solutions for work order management system are key factors driving the growth of the market.

- However, the work order management market growth is challenged by the integration complexities of work order management with existing systems, data security concerns, and a lack of skilled personnel. The market growth is expected to be accelerated by addressing these challenges with seamless integration of evolving technologies.

- The COVID-19 pandemic had a mixed impact on the studied market. The transition to remote work posed challenges in accessing and updating work orders, impacting productivity and communications. The industries like hospitality and travel experienced downturns, leading to decreased demand for these solutions. Whereas the adoption of cloud-based work order management solutions facilitated remote access and collaborations, becoming essential for managing distributed teams and ensuring business continuity in industries like manufacturing, e-commerce, healthcare, and others.

Work Order Management Market Trends

Manufacturing Expected to Exhibit Significant Adoption

- Work order management becomes an integral part of manufacturing operations, guiding the execution of production tasks, resource allocation, and scheduling. However, with the rise of digitalization, manufacturers are increasingly embracing technologies to streamline and optimize work order management.

- The manufacturing industry is witnessing a significant surge in adopting work order management solutions. This trend is driven by a multitude of factors, all pointing toward enhanced efficiency, cost optimization, and ultimately, improved effectiveness.

- Industry 4.0 is transforming industries, from legacy systems to smart components and machines, to promote digital factories and the development of an ecosystem of connected plants and enterprises. Industry 4.0 has persuaded OEMs to adopt IoT across their operations. The benefits offered by IoT in the manufacturing industry drive the adoption rates, such as increased machine utilization, predictive maintenance and production, data analytics, monitoring, automation, and cost benefits.

- Moreover, in November 2022, China's Ministry of Industry and Information Technology approved three new national manufacturing innovation centers. They also stated that these centers would focus on vital generic technologies and boost technological research and development in these industries. Also, the ministry stated that it would guide the new manufacturing innovation centers in strengthening their capabilities to seek technological innovation to provide critical support for the high-quality development of primary fields in manufacturing.

- According to a report by Manufacturers Alliance for Productivity and Innovation (MAPI) Foundation, by 2025, manufacturers are projected to increase their investment in digital technologies for production scheduling and control by 46%. This statistic highlights the increasing importance of digital transformation for the future of the work order and manufacturing processes.

North America Expected to Dominate the Market

- IoT technologies are overcoming the labor shortage in the manufacturing sector, especially in developed countries such as the United States. The Federal Government and private sector organizations in the United States are investing in Industry 4.0 IoT technologies to expand the American industrial base.

- Several technologies like AI, IoT, smart devices, and 3D printing are already growing the performance metrics of major US-based factories. The government in the region is also promoting the adoption of robotics by taking initiatives to support the growth of modern technologies in the robotics market.

- For instance, the US federal government initiated the National Robotics Initiative (NRI) program to strengthen the capabilities of building domestic robots in the country and boost research activities in the field. Work order management decreases supply-chain risk and ensures the quality and authenticity of in-transit products with a full survey of inbound and outbound logistics.

- Moreover, according to the Bureau of Labor Statistics, the construction sector employed around 8 million people in the United States as of February 2023, which increased from 7.29 million in 2021. Such rising demand for construction labor has propelled the demand for wearable devices among field workers, thus accelerating market growth.

- The North American region is expected to dominate the Work Order Management Market owing to the resence of several large vendors such as IBM, Microsoft, Oracle, and Salesforce, among others, coupled with the region's dominance in technology adoption and caters work order management solutions to various industries.

Work Order Management Industry Overview

The competitive landscape of the Work Order Management Market is semi-consolidated owing to the presence of several solution providers, such as Salesforce, IBM, Microsoft, SAP SE, and Oracle, amongst others, across the world. The market players are witnessing strategic initiatives such as product launch, mergers & acquisition, collaborations, and other to enhance their market presence.

In February 2024 - Gooten launches OrderMeshTM, an order management platform designed for on-demand production. This platform is designed to support retailers, manufacturers, eCommerce brands, and marketplaces as they broaden their product offerings, streamline order processing, and substantially reduce the operational complexities and costs of a made on-demand supply chain.

In September 2023 - Everfield, the UK-based software firm acquired Depotnet, a work order management software provider that specialized in the Telecoms, Utilities, and Infrastructure sectors. With the acquisition, Depotnet will be able to invest in growth and innovation with the support and resources of Everfield.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Mobile and Wearable Devices Among Field Workers

- 5.1.2 Enterprise Propensity Towards Optimizing Work for Better Execution of Projects

- 5.2 Market Restraints

- 5.2.1 Lack of Expertise Among Field Workers

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Solutions

- 6.1.2 Services

- 6.2 By Deployment Mode

- 6.2.1 On-Premise

- 6.2.2 Cloud

- 6.3 By End-user Industry

- 6.3.1 Manufacturing

- 6.3.2 Transportation and Logistics

- 6.3.3 Energy & Utilities

- 6.3.4 Healthcare

- 6.3.5 BFSI

- 6.3.6 Telecom and IT

- 6.3.7 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle-East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Salesforce.com, Inc.

- 7.1.2 IBM Corporation

- 7.1.3 Microsoft Corporation

- 7.1.4 Oracle Corporation

- 7.1.5 SAP SE

- 7.1.6 IFS AB

- 7.1.7 Infor Inc.

- 7.1.8 Hippo CMMS

- 7.1.9 ServiceMax, Inc.

- 7.1.10 Innovapptive Inc.

- 7.1.11 eMaint Enterprises, LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日