|

市場調査レポート

商品コード

1910812

ペイメントプロセッサ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Payment Processor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ペイメントプロセッサ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

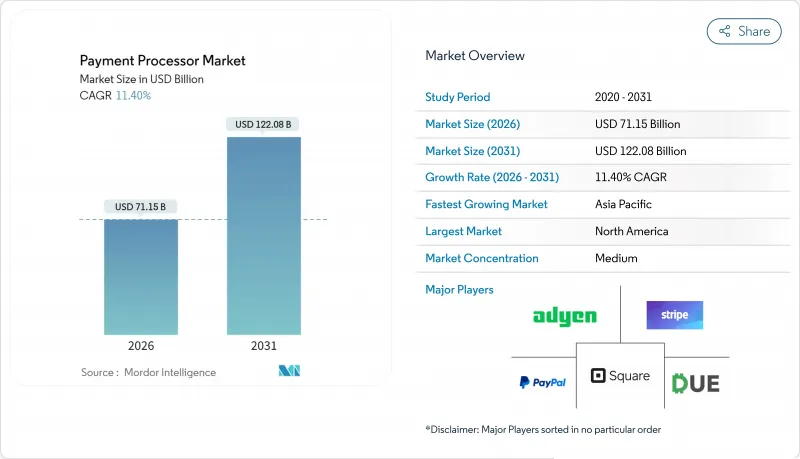

ペイメントプロセッサ市場は、2025年の638億7,000万米ドルから2026年には711億5,000万米ドルへ成長し、2026年から2031年にかけてCAGR11.4%で推移し、2031年までに1,220億8,000万米ドルに達すると予測されています。

堅調な成長は、組み込み金融の採用、リアルタイム決済の近代化、および対応可能な取引量を拡大する規制枠組みに起因しています。ソフトウェア・アズ・ア・サービス(SaaS)ベンダーは現在、収益の半分以上を組み込み決済から得ており、1,850億米ドル規模の組み込み金融エコシステムを支えています。ただし、このエコシステムは依然として総潜在機会の5分の1未満しか捉えていません。アジアおよび北欧諸国における口座間決済(A2A)スキームの導入加速により、決済時間が数日から数秒に短縮され、国境を越えた手数料が最大75%削減されました。EUおよび英国におけるオープンバンキング義務化により、2025年3月までに2,720万件・129億ポンド(162億米ドル)相当の決済が発生し、前年比67%増となりました。これはペイメントプロセッサ量に対する規制の触媒効果を実証するものです。地域別では、2024年に北米がペイメントプロセッサ市場で30%のシェアを占める一方、アジア太平洋地域は14.48%のCAGRで最速の成長を見せております。クレジットカードは45%で依然として主要な取引手段ですが、電子財布は2027年までに世界の財布価値が25兆米ドルに達する見通しの中で、15.12%のCAGRで成長を続けております。

世界のペイメントプロセッサ市場の動向と洞察

埋め込み金融APIの急速な普及が収益モデルを変革

SaaSプラットフォームは決済受入に加え、発行・融資・資金管理機能を統合し、プロセッサーが高付加価値取引を獲得可能に。単独サービスと比較し加盟店あたり40~60%の収益増を実現します。直接的な銀行関係と堅牢なコンプライアンス体制は、規制当局がフィンテックと銀行の提携を精査する中で競争優位性を創出。中堅企業は運用簡素化を実現する統合金融プラットフォームに注力し、予測期間を通じて組み込み金融の浸透を加速させます。

口座間リアルタイム決済スキームが国境を越えたインフラを再構築

プロジェクト・ネクサスはインド、マレーシア、フィリピン、シンガポール、タイを接続し、17億人の住民を対象とした即時送金を実現します。ISO 20022メッセージングと直接ネットワーク接続を統合するプロセッサーは、第二段階の財務効率化を求めるeマーケットプレースへの優先アクセスを獲得します。リアルタイム決済システムは決済サイクルと運用コストを圧縮し、従来型プロセッサーにスイッチアーキテクチャの近代化を迫るか、仲介機能喪失のリスクを強いることになります。

ライセンシングの分断化が新興市場で業務の複雑化を招く

タンザニアの2025年支払いサービスプロバイダーライセンスやカメルーンのサービス定義拡大は、別個の法人格と高い資本要件を求め、市場参入コストを押し上げています。

セグメント分析

2025年、クレジットカードはペイメントプロセッサ市場収益の44.55%を占め、世界の利用基盤により中核的地位を維持しています。電子ウォレット取引におけるペイメントプロセッサ市場規模はCAGR14.82%で拡大し、2027年までにウォレット取引高25兆米ドルを目標としています。デビットカード取引はA2A決済経路を通じて増加し、ミレニアル世代の即時資金アクセス需要に応えています。ステーブルコイン決済機能を追加したプロセッサーは、新興の暗号資産から法定通貨への取引量を獲得しています。その好例がStripeの11億米ドル規模のBridge取引で、これにより同社のプラットフォームはコンプライアンス対応のステーブルコイン処理が可能となりました。

カード、ウォレット、A2A送金、規制対象デジタル資産を統合的にサポートするプラットフォームを巡る競合が激化しています。従来型ネットワークはブロックチェーンの直接統合よりも提携を追求する一方、技術主導のプロセッサーはネイティブ暗号資産レールを追求します。加盟店は、トラフィックを動的に最低コストまたは最高受容率の方法へルーティングするオーケストレーションエンジンを好んで採用し、これにより決済コスト全体の削減とカート放棄率の低減を図っています。

ソリューション提供は2025年に66.35%のシェアを占め、年間12.1%の成長が見込まれます。これは加盟店が不正防止・照合・コンプライアンス業務を統合したダッシュボードを要求しているためです。ペイメントプロセッサ業者市場はPayFac-as-a-Serviceモデルを活用し、大規模なエンジニアリングリソースを必要とせずに加盟店オンボーディングを加速させています。サービス収益は並行して拡大する一方、コモディティ化が進むことで価格圧力に直面しています。

世界のペイメンツ社の2025年動向レポートでは、AI駆動型サービスの進化、ユニファイドコマース、高度なオーケストレーションが戦略的優先事項として示されています。分析ツール、融資機能、支払いツールを単一プラットフォームに統合するベンダーは、ペイメントプロセッサ業界全体でより高いウォレットシェアを獲得し、顧客離脱率を低減することで、より持続的な収益源を創出しています。

ペイメントプロセッサ業者市場レポートは、タイプ別(クレジットカード、デビットカード、電子財布取引)、コンポーネント別(ソリューション、サービス)、企業規模別(大企業、中小企業)、エンドユーザー産業別(小売・Eコマース、旅行・ホスピタリティなど)、地域別に分類されています。市場予測は金額ベース(米ドル)で提供されます。

地域別分析

北米のペイメントプロセッサ業者市場シェアは2025年に29.60%を占め、カードネットワークの高度な普及、確立された処理業者関係、透明性の高い規制環境を反映しています。成長は拡大よりも近代化に重点が置かれ、AI駆動型不正防止ツールやFedNow参加による微増が見込まれます。インターチェンジ手数料を巡る継続的な訴訟や進化するステーブルコイン枠組みは、既存事業者にとって短期的な戦略的不確実性をもたらしています。

アジア太平洋地域は、リアルタイム決済連携、モバイルファースト消費、越境電子商取引を原動力に、2031年までCAGR14.25%で将来の成長を牽引します。日本では2023年に540億9,000万円(3億6,000万米ドル)に達した不正利用を抑制するため、2025年4月より3-Dセキュアの導入が義務付けられます。キャッシュレス比率は2023年に39.3%に達し、80%目標に向けて進展中です。地域プロセッサーは、現地ウォレット・QRコード決済基盤・多通貨決済を統合することで、シームレスな越境機能を求める加盟店需要の恩恵を受けています。

欧州ではPSD3(第3次決済サービス指令)と決済サービス規制により消費者保護が強化される一方、銀行インフラへの第三者アクセスが拡大するなど、動向は複雑です。ラテンアメリカは依然としてパッチワーク状で、POSにおける現金とクレジットカードのシェアは各29%ですが、Pixなどの即時A2Aスキームの利用は74%増加しました。

アフリカおよび中東地域は長期的な成長余地を有していますが、ライセンシング制度の分断により導入コストが膨らみ、収益化までの期間が長期化する課題に直面しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 北米および欧州全域における埋め込み型金融APIの急速な加盟店導入

- アジア及び北欧地域における口座間(A2A)リアルタイム決済スキームの加速

- オープンバンキング規制がEU・英国における第三者決済事業者の取扱高を牽引

- ラテンアメリカにおける中小企業(SMB)のB2B決済デジタル化

- 越境電子商取引の成長が複数通貨処理需要を促進

- 暗号資産から法定通貨へのゲートウェイサービスがプロセッサーに新たな収益源をもたらす

- 市場抑制要因

- アフリカ及び東南アジアにおける国別ライセンシング制度の分断化

- ネットワーク手数料及びインターチェンジ手数料の上昇がプロセッサーの利益率を圧迫

- 非対面取引チャネルにおける不正利用・チャージバック責任の増大

- 新興市場におけるクラウドインフラの冗長性の不足

- バリューチェーン分析

- 規制の見通し

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 市場に対するマクロ経済動向の評価

第5章 市場規模と成長予測

- タイプ別

- クレジットカード

- デビットカード

- 電子ウォレット(電子マネー)での取引

- コンポーネント別

- ソリューション

- サービス

- 企業規模別

- 大企業

- 中小企業

- エンドユーザー産業別

- 小売業・電子商取引

- 旅行・ホスピタリティ

- 食品・飲料

- ヘルスケア

- 公益事業・政府機関

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- 北欧諸国

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- カタール

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- PayPal Holdings Inc.

- Stripe Inc.

- Adyen N.V.

- Due Inc.

- Square Inc.

- Fiserv Inc.

- Global Payments Inc.

- Block Inc.

- Worldpay(FIS)

- Checkout.com

- PayU

- Payoneer

- Nexi/Nets Group

- Verifone Inc.

- WePay(J.P. Morgan Chase)

- Alipay Merchant Services

- Amazon Pay

- Razorpay

- Klarna Payments

- Mollie

- Paysafe Ltd.

- Marqeta Inc.

- Galileo Financial Technologies

- BitPay

- CCBill LLC

- Braspag

- Banwire S.A. de C.V.