インドの食品および飲料パッケージング:市場シェア分析、産業動向、成長予測(2025~2030年)

India Food & Beverage Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1643030

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

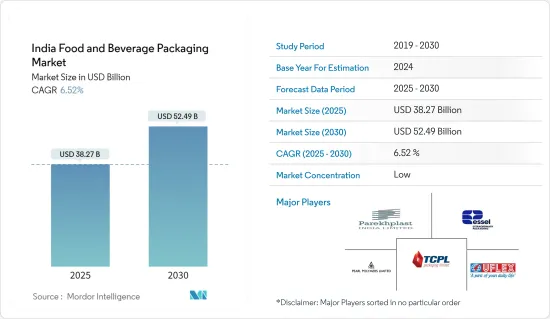

インドの食品および飲料パッケージング市場規模は2025年に382億7,000万米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは6.52%で、2030年には524億9,000万米ドルに達すると予測されます。

インドの食品パッケージング業界は、今後数年間で大幅な成長を遂げる構えです。これは、同国における包装食品の消費の増加、高品質製品に対する意識の高まり、持続可能な包装に対する並行需要によるところが大きいです。

主なハイライト

- 飲食品産業はパッケージングの拡大を推進する上で極めて重要です。農業廃棄物の削減に焦点を当て、食品加工分野への投資が拡大することで、革新的なパッケージング・ソリューションに新たな道が開かれています。こうした投資は廃棄物を最小限に抑えるだけでなく、パッケージングプロセスの効率と効果を高め、食品パッケージング業界の成長を支えています。

- 組織小売の拡大、中間所得層の増加、輸出の増加といった要因が業界を後押ししています。保存性を高め、生産を合理化し、製品の品質を確保するために、均一な包装が重視されるようになっています。中間所得層の購買力向上は包装食品への需要増につながり、進化する消費者の嗜好と規制基準を満たす先進パッケージング・ソリューションの必要性を後押ししています。

- インドの生活水準の向上、富の増加、ペースの速い都市型ライフスタイルが、オンライン食品配達の動向と包装食品の消費に拍車をかけています。Zomato、Swiggy、Dunzoなど、この分野の主要企業は、パッケージング革新の波に後押しされ、オンライン食品宅配サービスの急増を目の当たりにしています。これらの企業は、宅配食品の安全性、品質、利便性を確保する革新的なパッケージング・ソリューションを採用することで、消費者体験を向上させる新たな方法を継続的に模索しています。

- しかし、COVID-19の大流行によるサプライチェーンの混乱が業界の成長を妨げる要因となった。原材料価格の変動や、プラスチックの使用に関して政府が課す厳しい規制は、成長率をさらに低下させる可能性があります。環境に対する懸念の高まりと、環境に優しい代替品の入手可能性も、成長の妨げになると予想されます。

- 業界は、特に規制の進化に伴う大きな課題に直面しています。環境問題、特にプラスチック包装廃棄物に関する懸念の高まりは、環境破壊を抑制し廃棄物管理を強化するためにより厳しい規制の実施を政府に促しています。こうした規制の変化により、企業はより持続可能な包装材料や慣行を採用せざるを得なくなっており、これは業界にとって課題であると同時にチャンスでもあります。業界がこうした変化に適応できるかどうかが、今後の成長軌道を決定する上で極めて重要な役割を果たすことになります。

インドの食品および飲料パッケージング市場の動向

革新的で持続可能な食品パッケージングへの需要の高まりが業界の成長を牽引すると予想される

- インドでは、多忙な仕事のスケジュール、働く女性の増加、外出先での消費へのシフトにより、包装食品が高い支持を集めています。このため、食品業界では革新的で持続可能なパッケージングの利用が増加し、予測期間中の業界の成長に拍車がかかると予想されます。

- ナノ加工技術は、パッケージ、コーティング、包装技術の設計に使用する活性材料を作り出す画期的なソリューションとして台頭してきています。これらのソリューションは、官能特性と栄養特性を維持・改善し、食品の安全性を高め、賞味期限を延ばすのに役立ちます。

- 意識の高まりとともに、環境に優しく持続可能なパッケージングへの要求も着実に高まっています。国内では、持続可能なソリューションが重視され、ビジネスにとって不可欠なものとなりつつあります。食品販売店、レストラン、ホテル、病院、産業、ケータリング業者、および他のすべてのユーザーは、インドのEvirocorのような企業から環境に優しい食品パッケージング用品を得ることができます。環境に優しい包装の使用の増加は業界の拡大に拍車をかけると予想されます。

- IBEFによると、インドの食品加工業界は、可処分所得の増加や都市化によるライフスタイルや食生活の嗜好の進化に牽引され、大きな成長を遂げようとしています。同産業は堅調な拡大を見せており、2015年から2022年にかけてCAGR約7.3%を維持しています。予測では、加工青果物の輸出額は2021年度の15億3,400万米ドルから、2024年度には24億8,900万米ドルに急増すると見られています。

- インドでは、環境保護を重視する政府政策の転換が起きています。その結果、市場ベンダーは環境に配慮したパッケージング・ソリューションを展開しています。その多くは、持続可能な方法で調達された木材繊維から作られた包装ラインを発表しており、リサイクル可能性を確保しています。こうした取り組みは、廃棄物を抑制し、完全に再利用可能、リサイクル可能、堆肥化可能な製品群を推進するという業界のコミットメントを強調するものです。

パウチと袋の用途拡大が業界の成長を後押しする見込み

- フレキシブル・パッケージングのパウチや袋は、大幅な拡大を目の当たりにしています。食品パッケージング業界では、フレキシブル包装の中で最も使用されているタイプです。最も効果的で手頃なパッケージングオプションの一つとして、この業界で活動するプレーヤーはパウチ包装を選択しています。

- プラスチックパウチの拡大は、共重合を可能にし、可塑剤、発泡剤、抗菌剤、変色剤を添加することによって促進されます。パウチは適応性があり、携帯可能で軽いです。パウチの特徴(リシーラブルクロージャー、スパウト、ティアノッチなど)やパウチ製造技術(ラインスピードが改善された装置など)の改善は生産コストを下げ続け、パウチをより手頃な価格にしています。

- 生産者は、ジッパー付きクロージャーシステムや軽量オプションのように、消費者の生活を楽にする機能をアイテムに組み込むことを重視しています。例えば、ニクロム社はインド初の縦型パウチ包装機を使って、スナック菓子、ドライフルーツ、シリアル、豆類などを包装しています。

- プラスチック袋は、国内で最も普及しているプラスチック包装のひとつです。国内でのプラスチック袋の増加は、主にスーパーマーケット・チェーンやキラナ・アウトレットの拡大によるものです。プラスチック製キャリーバッグは、ベーカリー、キャンディー、スーパーマーケット、肉屋などの製品に全国的に広く利用されています。

- さらに、数多くの小売店が食品の鮮度を保ち、栄養価を保持するために包装材に頼っています。スーパーマーケット商品、特に冷凍食品とチルド食品の需要は今後数年で急増すると予測され、それによって業界の成長が促進されます。IBEFによると、インドの紙・プラスチック包装の生産量は、2021年の4億3,520万トンから2028年には6億9,000万トンに増加すると予想されています。これらの数字は、多様な包装資材の採用が拡大していることを裏付けており、市場の拡大を下支えしています。

インドの食品および飲料パッケージング業界の概要

インドの食品パッケージング業界は、多数の企業がシェア拡大を競っているため断片化しています。市場の主なプレーヤーには、Parekhplast India Limited、Essel Propack Limited、Pearl Polymers Ltd、TCPL Packaging Ltd、UFlex Ltdなどがあります。各社は市場での存在感を高めるため、多数のエンドユーザー市場に足跡を広げています。

- 2024年4月包装業界のChemco Groupは、革新的なストレッチフィルムラインを導入してリーダーシップを発揮。この技術は年間1,000トンを超える生産能力を誇っており、企業は品質に妥協することなく高まる需要に応えることができます。このラインのデビューは、Chemcoグループの卓越性への献身を強調するものであり、企業が求める業務効率と信頼性を保証するものです。

- 2024年3月スイスの包装会社SIGは、アーメダバード工場への段階的投資計画を発表しました。第1期では年間40億パックの生産を目指し、第2期では100億パックの生産を目指します。国連の「持続可能な開発目標」に沿って、SIG社は2050年までに温室効果ガス排出量を正味ゼロにすることを目標としています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場促進要因

- 加工食品の普及拡大が包装の成長を牽引する見込み

- 包装機械輸入の加速、食品および飲料パッケージング産業の増殖につながる

- 市場抑制要因

- 最善の管理および製造慣行への曝露不足

- COVID-19の業界への影響評価

第5章 市場セグメンテーション

- インドの食品パッケージング市場のセグメンテーション

- 材料別

- プラスチック

- 板紙

- 金属

- ガラス

- 製品タイプ別

- パウチ・袋

- ボトルとジャー

- トレー・容器

- フィルム・ラップ

- その他の製品タイプ

- 用途別

- 乳製品

- 肉・鶏肉・魚介類

- ベーカリー・菓子

- 果物・野菜

- その他の用途

- 材料別

- インドの飲料パッケージング市場セグメンテーション

- 材料別

- プラスチック

- 板紙

- 金属

- ガラス

- 製品タイプ別

- ボトル

- 缶

- パウチとカートン

- キャップ・クロージャー

- その他の製品タイプ

- 用途別

- 炭酸飲料・果実飲料

- ビール

- ワイン・蒸留酒

- ボトルウォーター

- 牛乳

- エナジー・スポーツドリンク

- その他の用途

- 材料別

第6章 競合情勢

- 企業プロファイル

- Parekhplast India Limited

- Essel Propack Limited

- Pearl Polymers Ltd

- TCPL Packaging Ltd

- UFlex Ltd

- Haldyn Glass Limited(HGL)

- Piramal Glass Limited

- HSIL Ltd

- Hindusthan National Glass & Industries Limited

- Hi-Can Industries Pvt. Ltd

- Hindustan Tin Works Ltd

- Deccan Cans & Printers Pvt. Ltd

- Autofits Packaging Private Limited

- P.R. Packagings Ltd

- Parksons Packaging Ltd

- OJI India Packaging Pvt. Ltd

- WestRock India Private Limited

第7章 投資分析

第8章 市場機会と今後の動向

目次

The India Food & Beverage Packaging Market size is estimated at USD 38.27 billion in 2025, and is expected to reach USD 52.49 billion by 2030, at a CAGR of 6.52% during the forecast period (2025-2030).

The food packaging industry in India is poised for substantial growth in the coming years. This is largely attributed to the country's increasing consumption of packaged food, a heightened awareness of quality products, and a parallel demand for sustainable packaging.

Key Highlights

- The food and beverage industry is pivotal in driving the expansion of packaging. With a focus on reducing agricultural waste, the growing investments in the food processing segment are creating new avenues for innovative packaging solutions. These investments are not only helping minimize waste but also enhancing the efficiency and effectiveness of packaging processes, thereby supporting the food packaging industry's growth.

- Factors such as the expansion of organized retail, a rising middle-income group, and an uptick in exports are bolstering the industry. There is a heightened emphasis on uniform packaging to enhance shelf life, streamline production, and ensure product quality. The increasing purchasing power of the middle-income group is leading to higher demand for packaged food products, driving the need for advanced packaging solutions that meet evolving consumer preferences and regulatory standards.

- India's improving standards of living, increasing wealth, and fast-paced urban lifestyles are fueling the trend of online food delivery and the consumption of packaged foods. Key players in this space, including Zomato, Swiggy, and Dunzo, are witnessing a surge in their online food delivery services, backed by a wave of packaging innovations. These companies are continuously exploring new ways to enhance the consumer experience by adopting innovative packaging solutions that ensure the safety, quality, and convenience of delivered food items.

- However, supply chain disruptions owing to the COVID-19 pandemic created hindrances to the industry's growth. Fluctuations in the prices of raw materials and stringent regulations imposed by the government on the application of plastic may further dampen the growth rate. The rising environmental concerns and the availability of environmentally friendly alternatives are also anticipated to hamper growth.

- The industry faces significant challenges, especially with the evolving regulations. Heightened environmental concerns, particularly around plastic packaging waste, have prompted governments to implement stricter regulations to curb environmental damage and enhance waste management practices. These regulatory changes are compelling companies to adopt more sustainable packaging materials and practices, which can be both a challenge and an opportunity for the industry. The industry's ability to adapt to these changes will play a crucial role in determining its future growth trajectory.

India Food & Beverage Packaging Market Trends

Rising Demand for Innovative and Sustainable Food Packaging is Expected to Drive the Industry's Growth

- In India, packaged foods are gaining high traction owing to busy work schedules, the rising number of working women, and the shift toward on-the-go consumption. This is expected to increase the utilization of innovative and sustainable packaging in the food industry, fueling the industry's growth over the forecast period.

- Nanofabrication technologies are emerging as ground-breaking solutions to create active materials for use in the design of packages, coatings, and packaging technologies. These solutions can help maintain and improve sensory and nutritional characteristics, increase food safety, and increase shelf life.

- With growing awareness, the requirement for eco-friendly and sustainable packaging is steadily rising. The country is focusing more on sustainable solutions, which is increasingly becoming imperative for business. Food outlets, restaurants, hotels, hospitals, industries, caterers, and all other users can get eco-friendly food packaging goods from companies like Evirocor in India. The increased use of eco-friendly packaging is anticipated to fuel the industry's expansion.

- As per IBEF, India's food processing industry is poised for significant growth, driven by evolving lifestyles and dietary preferences due to increasing disposable incomes and urbanization. The industry has seen robust expansion, maintaining an average annual growth rate of approximately 7.3% between 2015 and 2022. Projections suggest that exports of processed fruits and vegetables will surge from USD 1,534 million in FY 2021 to an estimated USD 2,489 million by FY 2024.

- India is experiencing a shift in governmental policies, emphasizing environmental conservation. Consequently, market vendors are rolling out eco-conscious packaging solutions. Many are unveiling packaging lines crafted from sustainably sourced wood fibers, ensuring recyclability. These initiatives underscore the industry's commitment to curbing waste and promoting a product range that is entirely reusable, recyclable, and compostable.

Growing Usage of Pouches and Bags is Expected to Boost the Industry's Growth

- Pouches and bags under flexible packaging are witnessing significant expansion. In the food packaging industry, they are the most used type of flexible packaging. As one of the most effective and affordable packaging options, players operating in this industry are choosing pouch packaging.

- The expansion of plastic pouches is fueled by their capacity to permit co-polymerization and by adding plasticizers, blowing agents, antibacterial chemicals, and color-changing additives. Pouches are adaptable, portable, and light. Improvements in pouch features (such as resealable closures, spouts, and tear notches) and pouch manufacturing technologies (such as equipment with improved line speeds) continue to reduce production costs, making pouches more affordable.

- Producers are emphasizing integrating features in items that make life easier for consumers, like zippered closure systems and lightweight options. For instance, Nichrome packages snacks, dry fruits, cereals, and pulses, among others, using India's first vertical pouch packaging equipment.

- Plastic bags are one of the nation's most popular types of plastic packaging. The rise in plastic bags in the nation is mainly due to expanding supermarket chains and Kirana outlets. Plastic carry bags are widely utilized nationwide for bakery, candy, supermarket, and butcher products.

- Furthermore, numerous retail outlets rely on packaging materials to preserve food freshness and retain its nutritional value. The demand for supermarket goods, particularly frozen and chilled meals, is projected to surge in the coming years, thereby propelling the growth of the industry. As per IBEF, the production volume of paper and plastic packaging in India is anticipated to climb from 435.2 million tons in 2021 to 690.0 million tons by 2028. These figures underscore the escalating adoption of diverse packaging materials, underpinning market expansion.

India Food & Beverage Packaging Industry Overview

The food packaging industry in India is fragmented due to the numerous businesses vying to increase their shares. Some major players in the market include Parekhplast India Limited, Essel Propack Limited, Pearl Polymers Ltd, TCPL Packaging Ltd, and UFlex Ltd. Companies are expanding their footprints across numerous end-user markets to increase their market presence.

- April 2024: Chemco Group, a player in the packaging industry, showcased its leadership by introducing an innovative stretch film line. This technology boasts an annual production capacity exceeding 1,000 tons, empowering businesses to meet rising demands without compromising quality. The debut of this line underscored Chemco Group's dedication to excellence, ensuring businesses have the operational efficiency and reliability they seek.

- March 2024: SIG, a Swiss packaging company, unveiled plans for a phased investment in its Ahmedabad plant. The first phase aims to boost production to 4 billion packs annually, with subsequent phases set to elevate this figure to 10 billion. In line with the UN Sustainable Development Goals, SIG is targeting net-zero greenhouse gas emissions by 2050.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Increasing Penetration of the Processed Food is Expected to Drive the Growth in Packaging

- 4.4.2 Acceleration in Packaging Machinery Imports, Leading to Proliferation of Food and Beverage Packaging Industry

- 4.5 Market Restraints

- 4.5.1 Lack of Exposure to Best Management and Manufacturing Practices

- 4.6 Assessment of COVID-19 Impact on the Industry

5 MARKET SEGMENTATION

- 5.1 India Food Packaging Market Segmentation

- 5.1.1 By Material

- 5.1.1.1 Plastic

- 5.1.1.2 Paperboard

- 5.1.1.3 Metal

- 5.1.1.4 Glass

- 5.1.2 By Type of Product

- 5.1.2.1 Pouches and Bags

- 5.1.2.2 Bottles and Jars

- 5.1.2.3 Trays and Containers

- 5.1.2.4 Films and Wraps

- 5.1.2.5 Other Types of Products

- 5.1.3 By Application

- 5.1.3.1 Dairy Products

- 5.1.3.2 Meat, Poultry, and Seafood

- 5.1.3.3 Bakery and Confectionary

- 5.1.3.4 Fruits and Vegetables

- 5.1.3.5 Other Applications

- 5.1.1 By Material

- 5.2 India Beverage Packaging Market Segmentation

- 5.2.1 By Material

- 5.2.1.1 Plastic

- 5.2.1.2 Paperboard

- 5.2.1.3 Metal

- 5.2.1.4 Glass

- 5.2.2 By Type of Product

- 5.2.2.1 Bottles

- 5.2.2.2 Cans

- 5.2.2.3 Pouches and Cartons

- 5.2.2.4 Caps and Closures

- 5.2.2.5 Other Types of Products

- 5.2.3 By Application

- 5.2.3.1 Carbonated Soft Drinks and Fruit Beverages

- 5.2.3.2 Beer

- 5.2.3.3 Wine and Distilled Spirits

- 5.2.3.4 Bottled Water

- 5.2.3.5 Milk

- 5.2.3.6 Energy and Sports Drinks

- 5.2.3.7 Other Applications

- 5.2.1 By Material

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Parekhplast India Limited

- 6.1.2 Essel Propack Limited

- 6.1.3 Pearl Polymers Ltd

- 6.1.4 TCPL Packaging Ltd

- 6.1.5 UFlex Ltd

- 6.1.6 Haldyn Glass Limited (HGL)

- 6.1.7 Piramal Glass Limited

- 6.1.8 HSIL Ltd

- 6.1.9 Hindusthan National Glass & Industries Limited

- 6.1.10 Hi-Can Industries Pvt. Ltd

- 6.1.11 Hindustan Tin Works Ltd

- 6.1.12 Deccan Cans & Printers Pvt. Ltd

- 6.1.13 Autofits Packaging Private Limited

- 6.1.14 P.R. Packagings Ltd

- 6.1.15 Parksons Packaging Ltd

- 6.1.16 OJI India Packaging Pvt. Ltd

- 6.1.17 WestRock India Private Limited

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日