|

市場調査レポート

商品コード

1852121

コンピュータ支援製造:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Computer Aided Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| コンピュータ支援製造:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

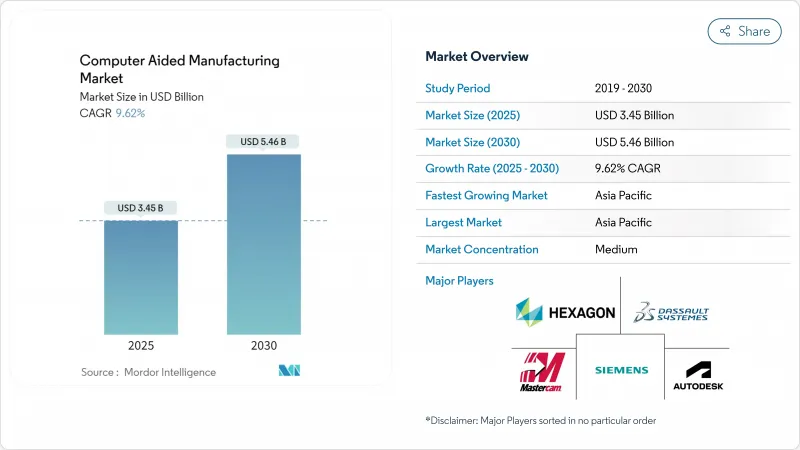

コンピュータ支援製造市場規模は2025年に34億5,000万米ドルに達し、2030年にはCAGR 9.62%を記録して54億6,000万米ドルに拡大すると予測されています。

サブトラクティブ+アディティブのハイブリッド生産セルへのシフト、人工知能とツールパス生成の融合、国産半導体パッケージングや電気自動車部品を優遇する政府の再シェアリング優遇措置などが成長の要因となっています。クラウドネイティブなコラボレーションとオンプレミスのセキュリティを融合できるベンダーは、防衛グレードの知的財産プロトコルを尊重しながら、複数の大陸にまたがる航空宇宙プログラムから利益を得ています。シーメンス、オートデスク、ダッソー・システムズは、リアルタイム機械分析を設計から製造までのスイート製品に組み込むことで、純粋なプログラミング速度に勝る予知保全の洞察をユーザーに提供し、プラットフォームの統合を強化しています。

世界のコンピュータ支援製造市場の動向と洞察

ハイブリッドマシニングセンタの台頭が生産経済性を変える

ハイブリッドシステムは、レーザーまたは指向性エネルギー蒸着と高速仕上げ加工を1つの筐体に統合することで、二次段取りを排除し、原材料の無駄を最大40%削減します。シーメンスNXは現在、ビードオンウォール蒸着と仕上げツールパスを自動化し、航空宇宙グレードの表面仕上げを達成する前に必要な箇所のみに材料を蒸着することで、複雑なチタン部品のサイクルタイム全体を25~30%短縮します。実際のロールアウトは、加法的および減法的動作をマイクロ秒単位で同期させるよう訓練されたオペレーターにかかっているが、このスキルはほとんどの加工工場で不足しています。

インダストリー4.0デジタルスレッドが予測製造を可能にする

クローズドループプラットフォームは、CAMプログラミングパラメータをリアルタイムのスピンドルパワー、振動、工具摩耗センサーに接続します。ヘキサゴンのアルゴリズムは、15~20分前に差し迫った工具の不具合を検出し、送り速度を自動調整して表面品質を公差内に維持することで、壊れやすい航空宇宙用合金のスクラップを軽減します。これらのソリューションは、高密度のセンサーネットワークと高スループットの分析を必要とするため、部品の価値が資本支出を正当化する工場への導入が制限されます。

オープンソースCAMが商用価格モデルに課題

FreeCAD PathWorkbenchは現在、ライセンス費用なしで2.5軸Gコードを出力できるため、学校やマイクロワークショップの入門レベルの選択肢として信頼できます。商用ベンダーは、AIを活用した最適化やクラウドコラボレーションなど、ほとんどのコミュニティプロジェクトの計算能力を超える機能をバンドルすることで対抗しているが、基本モジュールがコモディティ化するのを防がなければならないです。

セグメント分析

クラウドホスティング型スイートは、コンピュータ支援製造市場全体ではまだ少数派だが、2030年までのCAGRが10.9%であることは、不可逆的な方向性を示しています。3大陸に工場を持つ航空宇宙グループは、ブラウザベースのツールパス編集を利用して、夜間にジョブを引き渡し、リードタイムを20~25%短縮しています。防衛関連の請負業者は、ITAR規則が現場でのデータ主権を要求するため、完全移行に抵抗しています。その結果、クラウド・ソルバーにリンクされたローカル・ポストプロセッサーによるハイブリッド・スタックがブリッジを形成しています。エッジゲートウェイは、OPC-UAやMTConnectを持たない古いマシンに後付けすることで、コントローラを交換することなく暗号化されたデータをストリーミングできるようにします。サブスクリプション・モデルは、コストを資本予算から運用費にシフトさせる。クラウド分析により、ベンダーは匿名化されたフリート全体のスピンドル使用率をベンチマークし、予定外のダウンタイムを削減する予測メンテナンスダッシュボードに反映させることもできます。ゼロトラスト・アーキテクチャが成熟するにつれて、保守的なセクターでさえ2027年までに試験的な移行を計画しており、コンピュータ支援製造市場が次の予算サイクル内に心理的なクラウド採用のしきい値を超えることを示唆しています。

とはいえ、オンプレミスの基盤は、エアギャップ・ネットワークや独自の合金配合を持つ工場にとっては依然として不可欠です。ベンダーは、ファイアウォールの内側にありながら、選択したメタデータを遠隔地の専門家のためにクラウドの保管庫に同期させるデジタルスレッドモジュールをライセンシングすることで、これらのアカウントを獲得しています。このツイントラック戦略は、顧客がハイブリッド分析に移行するにつれて、ライセンス更新を安定させると同時に、経常収益を増加させる。プラットフォーム・サブスクリプションの段階がクラウド・コンピューティング・クレジットのオン・オフを切り替えるだけであるため、導入モード間の個別の価格設定は時間の経過とともに消滅する可能性があります。サイバー保険の保険料が機械工具のネットワークへの露出を反映するようになり、CFOはセキュリティ認定を総所有コストに反映させるようになっています。その結果、Computer-Aided Manufacturing市場は、クラウドかオンサイトかという二者択一ではなく、柔軟な入居形態へと進化しています。

2024年の売上高の36.2%を占める自動車は、より広範なComputer Aided Manufacturing市場の中心的セグメントです。しかし、内燃機関部品加工から電気自動車部品加工へのシフトは、長年のツールパスライブラリに課題を突きつけています。バッテリートレイのフライス加工では、高シリコンアルミニウムのスループットを維持しながら、びびりを管理する薄肉戦略が要求されます。一方、航空宇宙と防衛では、規模は小さいもの、5軸加工と複合材加工にプレミアムライセンスを要求しています。医療機器メーカーは、ISO 13485のトレーサビリティを満たすためにAIによるパラメータチューニングを採用し、手動で編集することなくシングルオペレーターセルで10μm以下の公差を達成できるようにしています。電子機器や半導体のパッケージング加工では、10万rpmのドリル加工で銅の剥離を防ぐために、熱を考慮したドリルシーケンシングが必要です。医療機器メーカーは、航空宇宙の表面仕上げルーチンを複製し、自動車メーカーは、バッテリーモジュールのウエハーファブの清浄度プロトコルを輸入し、コンピュータ支援製造の対応可能な市場を拡大しています。

自動車製造の多様化も同様に深刻です。構造部品のギガキャスティングは、何十ものプレス部品を排除しますが、アルミダイキャストの大規模なCNC仕上げを導入し、高い材料除去率と堅牢な工具寿命モデルを必要とします。このようなセルに投資するサプライヤーは、20時間の無人シフトで工具摩耗ドリフトを自動補正するソフトウェアを要求します。対照的に、ニッチなハイパーカーメーカーは、カーボンファイバー製トリムに重点を置き、5軸ルーターとプローブベースのパスアップデートを生産サイクルごとに使用しています。このような乖離は、1つの業種が複数のCAMライセンス層にまたがっていることを意味し、自動車の総生産台数が横ばいになっても、コンピュータ支援製造市場が厚みを保つことを保証しています。

地域分析

アジア太平洋地域のシェア47.1%は、その製造業の力強さを強調しているが、この地域は、プラグアンドプレイの相互運用性を複雑にするCNCプロトコルの分断とまだ格闘しています。中国の政策は、自国製のコントローラと結びついた自国製のCAMアルゴリズムを好んでおり、グローバルベンダーが二言語ポストプロセッサーやオープンAPIツールライブラリを通じて橋渡しをしなければならない並列エコシステムに拍車をかけています。日本の機械OEMは、CAMを制御ファームウェアに直接統合し、ツールパスのロード時間を短縮しているが、顧客は独自のスタックに閉じ込められています。インドのProduction Linked Incentive(生産連動型奨励金)制度は、労働力のスキルアップに結びつけばCAMライセンスを補助するもので、ベンダーは2030年までに従来の大手企業に匹敵する可能性のある新興の中堅市場への足がかりを得ることができます。

北米のユーザーがクラウドの導入でリードしているのは、CHIPS法が520億米ドルを地域のファブに流し込んでいるためです。欧州はエネルギー効率の高い加工を支持し、圧縮空気の削減と工具の再利用を義務付けており、CAM戦略シミュレータは現在、部品あたりのキロワット時でモデル化しています。データ主権ルールが摩擦を生んでいるが、ティアワン・サプライヤーは、工場横断的な最適化アルゴリズムと引き換えに、ローカライズされたデータレイクを受け入れています。このような地域的なニュアンスの違いにより、コンピュータ支援製造市場は幅広い多様化を維持し、地域的な不況を緩和しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ハイブリッド(サブトラクティブ+アディティブ)マシニングセンターの台頭

- インダストリー4.0対応デジタルスレッドの採用拡大

- 先端包装ラインにおける超精密部品の需要

- EVプラットフォーム現地化のための機動的生産ニーズ

- 多拠点コラボレーションを実現するクラウドネイティブCAMへのシフト

- 戦略部門に対する政府の再シェアリング優遇措置

- 市場抑制要因

- オープンソース/低コストCAM代替製品の普及

- NCプログラミングと後処理における根強い技能格差

- 防衛企業におけるクラウド導入に伴うIPセキュリティの懸念

- 細分化された工作機械コントローラー規格

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済要因の影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 展開モデル別

- オンプレミス

- クラウドベース

- エンドユーザー業界別

- 航空宇宙・防衛

- 自動車

- 医療機器

- エネルギーおよび公益事業

- エレクトロニクスと半導体

- 産業機械

- コンポーネント別

- ソフトウェア

- サービス

- 製造工程別

- 製粉

- ターニング

- 掘削

- 多軸/5軸

- 積層造形

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- 東南アジア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Autodesk Inc.

- Siemens Digital Industries Software(Siemens AG)

- Dassault Systemes SE

- Hexagon AB(Hexagon Manufacturing Intelligence)

- CNC Software LLC(Mastercam)

- HCL Technologies Ltd.

- OPEN MIND Technologies AG

- SolidCAM Ltd.

- Cimatron Ltd.

- NTT Data Engineering Systems Corp.

- BobCAD-CAM Inc.

- MecSoft Corporation

- PTC Inc.

- ZWSOFT Co. Ltd.

- SmartCAMcnc Inc.

- GibbsCAM(3D Systems Corp.)

- Hypertherm Inc.

- SprutCAM Tech Ltd.