|

市場調査レポート

商品コード

1641985

薬局管理システム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Pharmacy Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 薬局管理システム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

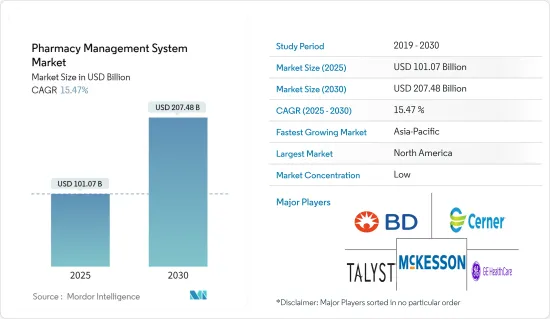

薬局管理システムの市場規模は2025年に1,010億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは15.47%で、2030年には2,074億8,000万米ドルに達すると予測されます。

主要ハイライト

- 薬局管理システム(PMS)は、データを保存し機能を実現することで、薬局内の医薬品使用プロセスを整理・管理するシステムです。医療における医薬品管理システムの用途の拡大と、さまざまな用途に医薬品管理システムを採用する薬局の増加が、市場の成長を促進する主要要因となっています。

- 薬剤師は、医薬品管理システムベースのプラットフォームを使用して医薬品を規制し、バリューチェーンに関与する多数の利害関係者を管理しています。コミュニケーションギャップを埋め、本物の医薬品を供給し、医薬品の偽造率を下げるこれらのシステムの能力は、薬局がシステムを採用し、ワークフローを合理化することを促し、市場成長を促進しています。

- さらに、独立系薬局とチェーン薬局の両方で薬局管理システム(PMS)の需要が高まっているのは、規制遵守が極めて重要な原動力となっています。これらのシステムは、e-Rx機能を組み込むことにより、しばしば処方箋の誤読に起因する投薬ミスを軽減する上で重要な役割を果たします。その結果、患者の安全性を高めるだけでなく、コンプライアンスへの取り組みも合理化します。また、PMSの使用は薬局の記録管理、電子処方箋、投薬の安全性、データセキュリティに役立つため、規制遵守のための導入が促進されます。

- さらに、世界中で慢性疾患や感染症の負担が増加しており、これらの疾患は処方薬の消費を増加させるため、市場で事業を展開する参入企業に大きな成長機会を提供すると期待されています。その結果、自動化された管理ソリューションに対する需要が高まると予想されます。しかし、導入コストの高さ、ソフトウェアハッカーの増加、ソフトウェアの使用法に関する理解の乏しさが、市場成長の課題となっています。

- COVID-19パンデミックは、世界の薬局管理ソフトウェアシステム市場にさまざまな影響を与えました。サプライチェーンの混乱と特定の医薬品に対する需要の急増は、PMSが提供する堅牢な在庫管理機能の重要性を浮き彫りにしました。さらに、パンデミックの間にオンライン薬局が増加したことで、eコマース機能を統合できるPMSのニーズが高まった。

薬局管理システム市場動向

チェーン薬局が市場成長を牽引する見込み

- 連鎖薬局の増加により、業務効率の向上、在庫管理、規制遵守、データ統合と一元化、顧客関係管理、処方箋処理の合理化などを目的とした薬局管理システムの需要が高まっている

- 医療産業の成長は、合理化された医療サービスに対する需要の高まりと、在庫管理における先進技術(特にAI)の採用によって推進されています。さらに、薬局産業の在庫管理ソフトウェアに対する意欲は、薬局自動化システムの受け入れ拡大や投薬ミスの削減への注目の高まりに後押しされ、急増するとみられます。

- 薬局チェーンの拡大は、効率的で拡大性があり、コンプライアンスに準拠したソリューションを必要とする複雑性を導入することで、薬局管理システムの必要性を高めています。例えば、インドを拠点とするMedPlus薬局チェーンは、インド南部で大きな存在感を示しており、全国最大規模の組織的小売薬局としての地位を確立しています。同社は、市場浸透と新規州への進出に注力し、年間600~700店舗の増加を計画しています。

- さらに、世界参入企業は世界の事業拡大に向けた戦略的な取り組みを行っています。2023年12月、病院・薬局チェーンのアスターDM医療社は、10億米ドルで湾岸事業を切り離した後、インドでの事業拡大に弾みをつけるため、民間事業者を買収する計画を発表しました。現在、アスターはインドと湾岸地域で34の病院と数百のクリニック、薬局を運営しています。

北米が大きな市場シェアを占める

- 北米諸国の医療産業は、新しい技術や新しい医療法・改革の実施に後押しされ、大きな変化を遂げつつあります。保険適用や効率的な治療計画を立てるための医療データ分析など、医療のほぼすべての側面が進化しています。

- 多くの薬局は歴史的なビジネスモデルを採用しているが、現代的な技術や顧客ケアの改善も含まれ始めています。免許を最大限に活用する(カウンセリングやポイントオブケア検査の提供など)のとは対照的に、米国の小売化学者は高学歴の医療専門家であり、錠剤の計数や臨床修正対応に不釣り合いな多くの時間を費やしています。冗長なプロセスや重要度の低い部分を自動化することで、従業員がこれらの活動に集中できるようにすることも可能可能性があります。

- 薬剤師の負担が増加しているため、市販薬(OTC)や処方箋薬の消費が増加しており、この地域では薬局管理システムの導入が進んでいます。例えば、カナダ統計局によると、カナダにおける処方薬の小売売上高は大幅に増加しています。処方薬の売上高は、2022年第3四半期の84億カナダドル(約60億7,000万米ドル)から2023年第3四半期には96億カナダドル(約69億3,000万米ドル)に増加しました。

- さらに、ほとんどの新しい処方薬は、他国に届く前にまず米国で販売されます。PMSは医薬品情報データベースと統合し、これらの新薬の最新の配合情報、潜在的な副作用、薬剤相互作用の警告にリアルタイムでアクセスできるため、薬剤師はこれらの情報を常に最新の状態に保つことができます。

- 米国の薬局・薬店数は、2022年11月の2万7,848店から2023年11月には3万739店に増加しました。このような薬局数の増加は、在庫管理、投薬ミスの防止、投薬量計算の自動化などの作業を自動化する薬局管理ソフトウェアの需要を促進すると予想されます。

薬局管理システム産業概要

薬局管理ソフトウェアシステム市場は細分化されており、McKesson Corporation、Becton Dickinson and Clanwilliam Health Ltd、Allscripts Healthcare Solution Inc.、Cerner Corporation、GE Healthcare Inc.、Talyst LLCのような参入企業が存在します。これらの企業は、市場シェアを拡大するために、パートナーシップ、提携、買収、製品発表などの戦略的取り組みを行っています。

- 2024年4月、Walgreensは、複雑な慢性疾患を持つ患者のケアへのアクセスを拡大し、Walgreensの薬局事業の収益性を高めるパートナーシップを可能にする総合的なサービスであるWalgreens Specialty Pharmacyを開始。

- 2023年11月、PHC Holdings Corporationの100%子会社であるWemex Corporationは、薬局向けソフトウェアPharnesXシリーズを日本で発売。同シリーズは、電子薬歴システム「PharnesX-MX」とレセプトシステム「PharnesX-EX」で構成され、薬歴管理に関する情報プロセスや業務の高度化により、薬剤師やスタッフの業務負担軽減を支援します。

- 2023年10月、薬局ソリューションプロバイダーのTitan PMRは、地域薬局を変革する最新の薬局管理ソフトウェアシステム「Titanverse」を発表し、その開発に100万英ポンド以上の私財を投じた。このプラットフォームにより、薬局チェーンのオーナーは、別々の薬局間でのデジタルによる業務移管、患者との直接のコミュニケーション、診察の実施、予約の管理、専門的な臨床サービスの促進が可能になります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が薬局管理ソフトウェアシステム市場に与える影響

第5章 市場力学

- 市場促進要因

- 処方箋枚数の増加による薬剤師の負担が市場成長を後押し

- 最近の技術革新と自動調剤システムの発売

- 医療における薬局管理システムの用途拡大が市場を独占

- 市場課題

- ベンダーロックインが薬局管理システム導入の大きな障壁に

第6章 市場セグメンテーション

- コンポーネント別

- ソリューション

- 在庫管理

- 発注管理

- サプライチェーン管理

- 規制・コンプライアンス情報

- 臨床・管理パフォーマンス

- その他のソリューション

- サービス

- ソリューション

- 展開別

- クラウドベース

- オンプレミス

- 組織規模別

- 独立系薬局

- チェーン薬局

- 地域別

- 北米

- 欧州

- アジア太平洋

- その他

第7章 競合情勢

- 企業プロファイル

- McKesson Corporation

- Cerner Corporation

- Becton Dickinson and Co.

- GE Healthcare Inc.

- Talyst LLC

- Allscripts Healthcare Solution Inc.

- Epicor Software Corporation

- Omnicell Inc.

- ACG Infotech Ltd

- Clanwilliam Health Ltd

- DATASCAN(DCS Pharmacy Inc.)

- GlobeMed Ltd

- Health Business Systems Inc.

- Idhasoft Ltd

- MedHOK Inc.

第8章 投資分析

第9章 市場の将来

The Pharmacy Management System Market size is estimated at USD 101.07 billion in 2025, and is expected to reach USD 207.48 billion by 2030, at a CAGR of 15.47% during the forecast period (2025-2030).

Key Highlights

- Pharmacy management systems (PMS) are the systems that organize and manage the drug usage process within pharmacies by storing data and enabling functionality. Growing applications of pharmacy management systems in healthcare and a rise in the number of pharmacies that are adopting pharmacy management systems for various applications are the key factors fueling the growth of the market.

- Chemists use pharmaceutical management system-based platforms to regulate drugs and manage numerous stakeholders engaged in the value chain. These systems' abilities to bridge the communication gap, supply authentic pharmaceuticals, and lower the rates of drug counterfeiting are encouraging pharmacies to adopt them and streamline workflows, thus driving market growth.

- In addition, regulatory compliance stands out as a pivotal driver for the growing demand for pharmacy management systems (PMS) in both independent and chained pharmacies. These systems, by incorporating e-Rx functionalities, play a crucial role in mitigating medication errors that often stem from misinterpreted prescriptions. Consequently, they not only bolster patient safety but also streamline compliance efforts. Also, the use of PMS helps pharmacies with record-keeping, e-prescriptions, medication safety, and data security, thus driving their adoption to comply with regulations.

- Furthermore, the rising burden of chronic and infectious diseases worldwide is expected to offer significant growth opportunities for players operating in the market, as these diseases increase the consumption of prescription drugs. This, in turn, is expected to increase demand for automated management solutions. However, high implementation costs, a rise in the number of software hackers, and a limited understanding of software usage are the factors challenging the market's growth.

- The COVID-19 pandemic had a mixed impact on the pharmacy management software systems market globally. Supply chain disruptions and surges in demand for certain medications highlighted the importance of the robust inventory management functionalities offered by PMS. Further, the growth of online pharmacies during the pandemic boosted the need for PMS that could integrate e-commerce functionalities.

Pharmacy Management System Market Trends

Chained Pharmacies Expected to Drive Market Growth

- The growing number of chained pharmacies creates demand for pharmacy management systems to enhance operational efficiency, inventory management, regulatory compliance, data integration and centralization, customer relationship management, and streamline prescription processing.

- The healthcare industry's growth is propelled by a rising demand for streamlined healthcare services and the adoption of advanced technologies, notably AI, in inventory management. Additionally, the pharmacy industry's appetite for inventory management software is set to surge, fueled by a growing embrace of pharmacy automation systems and a heightened focus on reducing medication errors.

- The expansion of pharmacy chains is driving the need for pharmacy management systems by introducing complexities that require efficient, scalable, and compliant solutions. For instance, the India-based MedPlus pharmacy chain has established itself as one of the largest organized retail pharmacies nationwide, with a significant presence in southern India. The company plans to add 600-700 stores annually, focusing on market penetration and expansion into new states.

- Moreover, global players are engaging in strategic initiatives to expand their business worldwide. In December 2023, hospital and pharmacy chain Aster DM Healthcare Ltd stated its plan to acquire private operators to fuel expansion in India after hiving off its Gulf business for USD 1 billion. Currently, Aster operates 34 hospitals and hundreds of clinics and pharmacies across India and the Gulf.

North America to Hold a Major Market Share

- The healthcare industry across North American countries is undergoing enormous alterations, fueled by new technologies and the implementation of new healthcare statutes and reforms. Almost all facets of healthcare are evolving, including insurance coverage and healthcare data analytics to create efficient treatment regimens.

- Many pharmacies use a historical business model, although it has begun to include modern technologies and improvements in customer care. In contrast to using their licenses to the fullest extent possible (such as offering counseling and point-of-care testing), retail chemists in the United States are highly educated medical professionals who spend a disproportionate amount of time counting pills and handling clinical corrections. It might also be possible to help employees concentrate on these activities by automating redundant processes and less critical aspects of their profession.

- Due to the rise in the burden on pharmacists, increasing consumption of over-the-counter (OTC) and prescription drugs is driving the adoption of pharmacy management systems in the region. For instance, according to Statistics Canada, retail sales of prescription drugs in Canada have seen a significant rise. The sales of prescription drugs increased to CAD 9.6 billion (~USD 6.93 billion) in the third quarter of 2023 from CAD 8.4 billion (~USD 6.07 billion) in the third quarter of 2022.

- Moreover, most new prescription drugs are sold first in the United States before they reach other nations. PMS allows pharmacists to stay up to date on this information as it can integrate with drug information databases to provide real-time access to the latest prescribing information, potential side effects, and drug interaction warnings for these new medications.

- The number of pharmacies and drug stores in the United States increased from 27,848 in November 2022 to 30,739 in November 2023. This rise in the number of pharmacies is anticipated to drive demand for pharmacy management software to automate tasks such as inventory management, prevent medication errors, and automate dosage calculations.

Pharmacy Management System Industry Overview

The pharmacy management software systems market is fragmented, with players such as McKesson Corporation, Becton Dickinson and Clanwilliam Health Ltd, Allscripts Healthcare Solution Inc., Cerner Corporation, GE Healthcare Inc., and Talyst LLC operating in the market. These players are engaging in strategic initiatives like partnerships, collaborations, acquisitions, and product launches to expand their market share.

- April 2024: Walgreens launched Walgreens Specialty Pharmacy, a holistic offering that expands access to care for patients with complex, chronic conditions and enables partnerships that drive profitability for Walgreens' pharmacy business.

- November 2023: Wemex Corporation, a wholly owned subsidiary of PHC Holdings Corporation, launched the PharnesX series of software for pharmacies in Japan. This series includes PharnesX-MX, an electronic medication history system, and PharnesX-EX, a medical receipt system, which helps pharmacists and staff reduce their workload by enhancing information processes and operations related to medication record-keeping.

- October 2023: Titan PMR, a pharmacy solutions provider, introduced its latest pharmacy management software system, Titanverse, to transform community pharmacy and invested more than GBP 1 million of private funds in its development. This platform enables pharmacy chain owners to digitally transfer workloads between separate pharmacies, communicate directly with patients, carry out consultations, manage appointments, and promote specialist clinical services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Pharmacy Management Software Systems Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Burden on Pharmacists due to Rising Number of Prescriptions Set to Encourage Market Growth

- 5.1.2 Recent Innovations and the Launch of Automated Dispensing Systems

- 5.1.3 Growing Applications of Pharmacy Management Systems in Healthcare to Dominate the Market

- 5.2 Market Challenges

- 5.2.1 Vendor Lock-in is a Major Barrier to Adoption of Pharmacy Management Systems

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Solutions

- 6.1.1.1 Inventory Management

- 6.1.1.2 Purchase Orders Management

- 6.1.1.3 Supply Chain Management

- 6.1.1.4 Regulatory and Compliance Information

- 6.1.1.5 Clinical and Administrative Performance

- 6.1.1.6 Other Solutions

- 6.1.2 Services

- 6.1.1 Solutions

- 6.2 By Deployment

- 6.2.1 Cloud-based

- 6.2.2 On-premise

- 6.3 By Size of the Organization

- 6.3.1 Independent Pharmacies

- 6.3.2 Chained Pharmacies

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 McKesson Corporation

- 7.1.2 Cerner Corporation

- 7.1.3 Becton Dickinson and Co.

- 7.1.4 GE Healthcare Inc.

- 7.1.5 Talyst LLC

- 7.1.6 Allscripts Healthcare Solution Inc.

- 7.1.7 Epicor Software Corporation

- 7.1.8 Omnicell Inc.

- 7.1.9 ACG Infotech Ltd

- 7.1.10 Clanwilliam Health Ltd

- 7.1.11 DATASCAN (DCS Pharmacy Inc.)

- 7.1.12 GlobeMed Ltd

- 7.1.13 Health Business Systems Inc.

- 7.1.14 Idhasoft Ltd

- 7.1.15 MedHOK Inc.