|

市場調査レポート

商品コード

1641953

シンガポールの海事産業-市場シェア分析、産業動向、成長予測(2025年~2030年)Maritime Industry In Singapore - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シンガポールの海事産業-市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

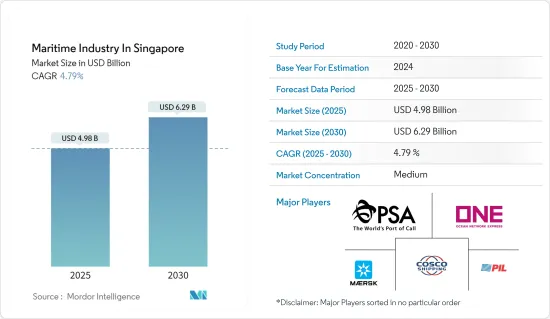

シンガポールの海事産業市場規模は2025年に49億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.79%で、2030年には62億9,000万米ドルに達すると予測されています。

シンガポール海事港湾庁(MPA)によると、シンガポールは現在進行中のコロナウイルス(COVID-19)パンデミック時に港で実施された乗組員交代が10万人を突破しました。2020年3月27日以降、MPAは5,000社以上、6,700隻以上の船舶が関与するさまざまな船籍の船舶から、あらゆる国籍の乗組員10万人のサインオン・サインオフを促進しました。

シンガポールは世界有数のハブ港であり、国際海事センターです。毎年、13万隻の船舶が入港します。シンガポール海域には常時、約1,000隻の船舶が入港しています。港湾では毎分1,000トン以上の貨物が取り扱われています。シンガポールは2020年においても、世界第2位のコンテナ港、世界第1位のバンカー港の地位を維持しています。また、コロナウイルス(COVID-19)パンデミックの中、8万人以上の船員の乗船交代を促進しました。

120カ国以上、600以上の港と結ばれているシンガポールの世界のネットワークは、どこでも効率的に物資を輸送することを可能にしています。しかし、地域の港湾が能力を増強し、新技術に投資するにつれ、競争も激化しています。自動化、デジタル化、リアルタイムのデータ共有により、港湾管理や海運業の効率は世界的に向上しています。

海運はシンガポールの生命線に深く関わっており、その輝かしい関係は、シンガポール建国当初にエントレポット貿易の拠点として始まったことにまで遡る。一世代で第三世界から第一世界へと発展したシンガポールの開発において重要な役割を果たした海運部門は、現在もシンガポール経済の重要な成長エンジンであり、国内総生産(GDP)の7%を占め、さまざまな技術職や商業関連職で17万人以上を雇用しています。

シンガポール海事市場の動向

新興諸国の港湾開発

シンガポール政府は、世界有数の都市として、またアジアと世界を結ぶ重要な輸送手段としての地位を維持するため、交通インフラへの投資を続けています。

トゥアス港は、シンガポールの次世代コンテナ港として開発が進められています。最大30年の建設期間を経て2040年代に完全に完成すれば、トゥアス港は年間最大6,500万TEUを処理できる世界最大のコンテナ港となります。この新港は、現在の市街地ターミナルのリース満了に伴う移転に対応するもので、シンガポールのすべてのコンテナ活動の集約場所となり、ターミナル間の運搬作業と温室効果ガス排出を大幅に削減します。

海面上昇に対応するため、トゥアス港は最高海面から5メートルの高さに運用プラットフォームを設置し、総盛土材料の50%以上を浚渫土と建設時の掘削土で賄う。このような資材を再利用することで、埋め立てのための砂への依存度を減らし、資材コストを20億SGD以上節約することができます。埋め立ては2015年に始まり、2021年に完了しました。

トゥアス港はデジタルで自動化されます。Digitalport@SGとジャスト・イン・タイム(JIT)システムは、船舶の通関プロセスを合理化し、船舶のターンアラウンド・タイムを向上させています。オートメーションとロボット工学を多用し、岸壁やヤードのハンドリングシステムと組み合わせて、遠隔地のオペレーションセンターからオペレーションを制御します。

海事セクターのデジタル化は産業の成長につながる

シンガポールの港湾をより効率的で費用対効果が高く、環境に優しいものにするため、最新の技術革新を活用することに特に力を入れています。

例えば、トゥアスのターミナルには先進的な港湾技術が導入され、数多くの自動化システムが導入される予定です。自動誘導車(AGV)、自動ヤード・岸壁クレーン、コンテナ用自動保管・検索システムなどが導入され、ヤードの保管能力が向上し、メガ・インテリジェント・コンテナ・ターミナルが誕生します。PSAシンガポールによると、シンガポール運輸省(MoT)はPSAコーポレーションと協力し、異なる港湾ターミナル間のコンテナトラック輸送需要の増加に対応するための自律型トラックプラトゥーニングシステムの設計・開発に取り組んでいます。

NGP2030の一環として、シンガポールの港湾はデジタル化を進めています。それによると、Tuas Terminalはビッグデータと予測分析機能を利用して、海洋学的・気象学的条件、海上交通と貨物の流れ、資材と機械の性能、さらには乗客と船員の情報に関するデータを管理し、レポートを共有します。内蔵アルゴリズムが船舶の交通パターンの異常を検知し、より安全な運航に貢献します。

港湾業務におけるグリーンエネルギーと再生可能エネルギーの利用は、高い優先事項です。NGP2030は、再生可能エネルギー利用の機会を特定し、実施するために、地元の大学を参加させています。PSA Singaporeは、ハイブリッド燃料車や電気自動車の利用以外にも、日本のソーラーフロンティアと提携し、超軽量で折り曲げ可能なCIS薄膜太陽電池モジュールをパシルパンジャン第3ターミナルを皮切りに港湾ターミナルに設置しています。クリーンエネルギー、特に船舶燃料としてのLNGの利用は、シンガポールをLNGバンカリング・ハブに発展させるNGP2030の主要開発となります。これを先導するため、MPAはすでにLNG燃料船の開発への資金援助や、エンド・ツー・エンドのLNGバンカリング供給ソリューションの開発など、いくつかのイニシアチブを実施しています。

シンガポール海事産業概要

シンガポールの海事産業は、世界の参入企業と地域的な参入企業が混在する断片的な産業です。主要参入企業には、PSA International、ONE (Ocean Network Express)、PIL (Pacific International Lines)、AP Moller Singapore Pte Ltd、NYK Groupなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 積み替え貿易に関する洞察

- コンテナ船と非コンテナ船に関する洞察

- バンカリングサービスに関する洞察

- 海事産業への投資に関する洞察

- 事業所数とサービス業全体に対する海運業の貢献に関する洞察

- 政府の規制と取り組み

- 港湾の技術動向と自動化

- COVID-19が市場に与える影響(市場への短期的・長期的な影響を論じる)

第5章 市場力学

- 市場促進要因

- 市場抑制要因

- 市場機会

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション(金額ベース市場規模)

- サービスタイプ別

- 水運サービス

- 船舶リース・レンタルサービス

- 荷役サービス(コンテナサービス、クレーンサービス、港湾荷役サービスなど)

- 水運支援サービス(海運代理店、船舶斡旋サービス、船舶管理サービスなど)

第7章 競合情勢

- 市場集中度概要

- 企業プロファイル

- PSA International

- ONE(Ocean Network Express)

- PIL(Pacific International Lines)

- AP Moller Singapore Pte Ltd

- Cosco Shipping (Singapore) Petroleum Pte Ltd

- NYK Group

- CMA CGM & ANL (Singapore) PTE LTD

- Evergreen Marine (Singapore) Pte Ltd

- Sea Consortium Private Ltd

- Hin Leong Marine International*

第8章 市場の将来

第9章 付録

The Maritime Industry In Singapore Market size is estimated at USD 4.98 billion in 2025, and is expected to reach USD 6.29 billion by 2030, at a CAGR of 4.79% during the forecast period (2025-2030).

Singapore has crossed the 100,000 mark for crew change carried out at the port during the ongoing coronavirus (COVID-19) pandemic, according to the Maritime and Port Authority of Singapore (MPA). Since 27 March 2020, MPA has facilitated 100,000 sign-on and sign-off crew of all nationalities from ships of different flags involving more than 5,000 companies and 6,700 ships.

Singapore is a premier global hub port and an international maritime center. Every year, 130,000 vessels enter into ports. At any given time, there are about 1,000 vessels in Singapore's waters. More than 1,000 tonnes of cargo are handled in the ports every minute. Singapore has retained its position as the world's second-busiest container port and the number-one bunkering port in 2020. It has also facilitated crew change for more than 80,000 seafarers amid the coronavirus (COVID-19) pandemic.

Connected to more than 600 ports in over 120 countries, Singapore's global network allows goods to be transported efficiently anywhere. However, competition is also heating up as regional ports build more capacity and invest in new technology. Emerging technologies are transforming the nature of shipping, with automation, digitalization, and real-time data sharing improving the efficiency of port management and sea transport industries globally.

Maritime is steeped in the lifeblood of Singapore, with its illustrious relationship tracing back to its beginning as a hub for entrepot trade in the nation's early days. After playing such a critical role in Singapore's development from a third-world to a first-world nation within one generation, the maritime sector now continues to be a significant engine of growth for Singapore's economy, making up 7% of the nation's GDP and employing more than 170,000 people in various technical and commerce-related functions.

Singapore Maritime Market Trends

Development of Ports in the Country

The Government of Singapore continues to invest in transport infrastructure to maintain the country's position as a world-class city and key transport mode between Asia and the world.

Tuas Port is being developed as the next-generation container port in Singapore. When fully completed in the 2040s, after construction of up to 30 years, Tuas Port will be the world's single largest container port, capable of handling up to 65 million TEU per annum. The new port is to accommodate the move of the current city terminals when their leases expire and will be the consolidated location for all of Singapore's container activities, significantly reducing inter-terminal haulage operations and greenhouse gas emissions.

To adapt to rising sea levels, Tuas Port will have an operational platform of five meters above maximum sea level, with over 50% of the total fill materials coming from dredged material and excavated earth from construction. Reusing such materials reduces reliance on the sand for reclamation, saving over SGD 2 billion in material costs. Reclamation began in 2015 and was completed in 2021.

Tuas Port will be automated digitally. Digitalport@SG and Just-in-Time (JIT) Systems will streamline vessel clearance processes, thereby enhancing vessel turnaround times. Extensive use of automation and robotics will be employed in conjunction with quayside and yard handling systems with operations controlled from a remote Operations Centre.

Digitalization in the Maritime Sector Would Lead to the Industry's Growth

A special focus has been on leveraging the latest technological innovations to make Singapore's ports more efficient, cost-effective, and environment-friendly.

The Tuas terminal, for example, will deploy advanced port technologies and will have numerous automated systems. In the works are Automated Guided Vehicles (AGVs), automated yard and quay cranes, and an Automated Storage and Retrieval System for containers to increase the yard storage capacity and create a mega intelligent container terminal. According to PSA Singapore, Singapore's Ministry of Transport (MoT) is working with PSA Corporation to design and develop an autonomous truck platooning system that will help meet the increasing demand for container truck haulage between different port terminals.

As a part of NGP 2030, Singapore's ports are embracing digitization. It reports that the Tuas Terminal will use Big Data and Predictive Analytics capabilities to manage data and share reports on oceanographic and meteorological conditions, maritime traffic and cargo flow, material and machinery performance, and even passengers' and seafarers' information. Built-in algorithms detect anomalies in vessel traffic patterns and contribute to safer operations.

The use of green and renewable energy in port operations is a high priority. The NGP 2030 brings local universities into the fold to identify and implement opportunities for using renewable energy. Apart from using hybrid-fuel and electric vehicles, PSA Singapore has partnered with the Japanese company Solar Frontier to install ultralight and bendable CIS thin-film solar energy modules at port terminals, starting with Pasir Panjang Terminal three. The use of clean energy, especially LNG as a ship fuel, will be a key development in the NGP 2030 to develop Singapore into the LNG bunkering hub. To spearhead this, the MPA has already implemented several initiatives, such as funding the development of LNG-fuelled vessels and developing an end-to-end LNG Bunkering supply solution.

Singapore Maritime Industry Overview

The Maritime Industry in Singapore is fragmented in nature, with a mix of global and regional players. Some of the major Players Include PSA International, ONE (Ocean Network Express), PIL (Pacific International Lines), AP Moller Singapore Pte Ltd, and NYK Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Insights of Transshipment Trade

- 4.3 Insights on Containerized and Non-containerized Shipments

- 4.4 Insights on Bunkering Services

- 4.5 Insights on Investments in the Maritime Industry

- 4.6 Insights on the Number of Establishments and the Maritime Sector's Contribution to the Total Services Sector

- 4.7 Government Regulations and Initiatives

- 4.8 Technological Trends and Automation in Ports

- 4.9 Impact of COVID-19 on the Market (discussing short-term and long-term effects on the market)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.2 Market Restraints

- 5.3 Market Opportunities

- 5.4 Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION (Market Size by Value)

- 6.1 By Services Type

- 6.1.1 Water Transport Services

- 6.1.2 Vessel Leasing and Rental Services

- 6.1.3 Cargo Handling (Container Services, Crane Services, Stevedoring Services, etc.)

- 6.1.4 Supporting Service Activities to Water Transport (Shipping Agencies, Ship Brokering Services, Ship Management Services, etc.)

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 PSA International

- 7.2.2 ONE (Ocean Network Express)

- 7.2.3 PIL (Pacific International Lines)

- 7.2.4 AP Moller Singapore Pte Ltd

- 7.2.5 Cosco Shipping (Singapore) Petroleum Pte Ltd

- 7.2.6 NYK Group

- 7.2.7 CMA CGM & ANL (Singapore) PTE LTD

- 7.2.8 Evergreen Marine (Singapore) Pte Ltd

- 7.2.9 Sea Consortium Private Ltd

- 7.2.10 Hin Leong Marine International*