ハイブリッド複合材料:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Hybrid Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641941

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

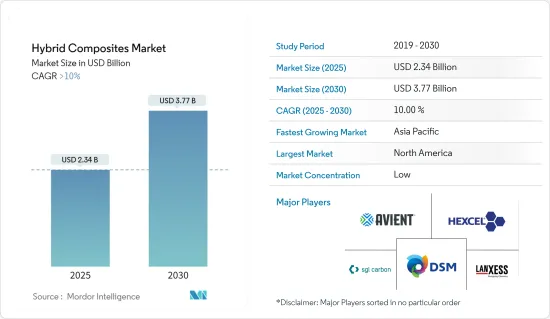

ハイブリッド複合材料の市場規模は2025年に23億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは10%を超え、2030年には37億7,000万米ドルに達すると予測されています。

COVID-19の大流行がハイブリッド複合材料市場に与えた影響はまちまちでした。当面の課題となった一方で、この材料の可能性を浮き彫りにし、長期的な成長に貢献しうる動向の引き金ともなりました。

ロックダウンや渡航制限によって原料や完成品の流れが途絶え、生産の遅れや材料不足につながりました。航空宇宙、自動車、風力エネルギーなど、ハイブリッド複合材料に大きく依存している産業は、旅行制限や景気減速のために大幅な景気後退に見舞われ、材料需要が減退しました。その反面、パンデミックは医療機器や装置における先端材料の必要性を浮き彫りにし、人工装具、インプラント、手術器具に生体適合性ハイブリッド複合材料のビジネス機会を生み出しました。

主要ハイライト

- 軽自動車セグメントで複合材料の採用が拡大しており、従来の複合材料と比較してハイブリッド複合材料が示す優れた特性が、調査対象市場の主要促進要因となっています。

- その反面、ハイブリッド複合材料の加工と製造には、複雑で労働集約的な技術を伴うことが多く、コストを押し上げ、調査対象市場の成長の抑制要因になる可能性があります。

- 複合材製造のための自動化、デジタル化、付加製造技術の探求は、プロセスを合理化し、コストを削減し、製品の一貫性を改善することができ、世界市場に有利な機会を提供することができます。

- アジア太平洋は、中国からの高い需要により、予測期間中に最も高い成長率を示すと予想されます。

ハイブリッド複合材料市場の動向

炭素/ガラスが市場を独占

- 最も一般的に使用されているハイブリッド複合材料は、ガラス繊維強化ポリマー(GFRP)複合材料と炭素繊維強化ポリマー(CFRP)複合材料であり、アラミド繊維や天然繊維で強化された複合材料がこれに続きます。

- 炭素繊維とガラス繊維のハイブリッド材料は、自動車・輸送、建築・建設、その他の産業市場において、従来のガラス繊維や金属の用途に代わる軽量で高強度の代替材料です。

- このハイブリッド材料は、高性能ガラス繊維と同程度のコストで、炭素繊維の性能上の利点を記載しています。

- ハイブリッド複合材料は、オートメーションや高速製造プロセスへの応用が増加しており、自動車やその他のセグメントにおける大量生産の要求に応えています。

- OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、2022年には世界中で約8,501万台の自動車が生産され、2021年の8,020万5,000台と比較して5.99%の成長率を示しました。2022年には、世界中で約6,000万台の乗用車が生産され、2021年と比較して7.35%近く増加しました。

- 使用事例は、炭素繊維を使用する場合よりもはるかに低いコストで、カーボンの利点の最大90%を得ることができます。

- これらのハイブリッド複合材料から作られた部品は、高い強度対重量比を提供し、腐食がないです。耐用年数も長く、メンテナンスも少なくて済みます。その特殊な特性は、安全性と強度を最も重視する用途のニーズに合致しています。

- 建築・建設のセグメントでは、多くの複合材製品や用途が、そのユニークな特性(耐食性、断熱性、軽量性など)のおかげで、ますます支持を集めています。コンクリート補強用の複合鉄筋から、窓枠用の引抜形材や複合屋根瓦まで、複合製品はよりサステイナブル設計を可能にするだけでなく、既存の建物や橋などの補修、アップグレード、補強に効果的なソリューションを記載しています。

- JEC Compositesによると、材料のリサイクルや再利用に対する関心は高く、複合材料産業の主要企業は多くの取り組みを行っています。例えば、欧州の風力産業は、2025年までにタービンブレードの100%を再利用、リサイクル、回収することを約束しています。

- 上記の要因から、予測期間中は炭素/ガラス繊維タイプが市場を独占する可能性が高いです。

アジア太平洋の成長率が最も高い

- アジア太平洋のインフラ産業は、近年健全な成長を続けています。したがって、この地域は評価期間中にセメントボード市場で驚異的な成長率を示すと推定されます。

- アジア太平洋では現在、特に中国、日本、台湾、韓国、インド、マレーシア、インドネシア、ベトナムなどの新興経済諸国において、住宅や商業施設の建設に高い投資が行われています。

- JEC Compositesによると、今後、長期的な動向はアジア新興国が経済成長を牽引する形で再開されるはずです。中国の成長率はCAGR年率5%を超え、欧州や米国を上回ると予想され、インド、フィリピン、インドネシア、マレーシアも同程度の成長が見込まれます。中期的(2021~2026年)には、複合材料市場はすべての地域で成長を再開するはずであり、特にアジア(エネルギー、E&E、...)では長期的成長の可能性がまだかなり残っています。

- 自動車セグメントでは、様々な繊維と樹脂の長所を組み合わせたこれらのユニークな材料は、軽量化、性能向上、燃費改善という勝利の組み合わせを提供し、アジア太平洋市場でのハイブリッド複合材料の消費拡大につながります。

- 中国の自動車製造産業は世界最大です。同産業は2022年にわずかながら成長し、生産と販売が増加しました。同様の動向は2021年も続き、2022年の生産台数は3%増となりました。中国汽車工業協会(CAAM)によると、BYD、SAIC Motorsなどの企業が燃料走行車や電気自動車セグメントで自動車生産の売上を伸ばしており、自動車生産は今後も成長すると予想されています。

- 中国汽車工業協会によると、中国の自動車メーカーは、2022年の690万台から、前年には約940万台の電気自動車とハイブリッド車の販売を報告すると予想されています。同協会はさらに、2024年の販売台数は引き続き増加し、1,150万台に達すると予測しています。

- 例えば、中国の自動車大手BYDは、2023年に300万台以上のバッテリー駆動車を販売し、そのうちバッテリーとガソリンの両方を動力源とする完全な電気自動車が160万台、さらにハイブリッド車が140万台です。これは2022年比で62%の増加です。BYDによると、BYDは収益も上げており、昨年上半期の利益は3倍の15億米ドルに達しました。

- India Todayによると、2023年には国内市場で410万8,000台の自動車が販売されました。暦年で400万台を超えたのはこれが初めてです。2022年の販売台数は379万2,000台でした。インドでは、Maruti、Hyundai、Tata、Honda、Mahindraといった大手自動車メーカーが、売れ残り在庫のために生産を停止しています。これは近い将来、インドの自動車生産に大きな悪影響を及ぼすと予想されます。

- 中国は世界最大の医療セクターのひとつです。第13次5ヵ年計画では、中国政府は健康と技術革新を優先しており、予測期間中に医療機器製造セクターへの投資が増加すると予想されます。さらに、COVID-19の発生により、同国では医療セグメントへの投資が徐々に拡大しています。

- ハイブリッド複合材料は、場合によっては鋼鉄をも凌ぐ、非常に優れた強度対重量比を達成することができます。そのため、耐荷重構造物、橋梁、耐震建築物に理想的です。

- 中国の成長は、住宅と商業建築部門の急速な拡大と、同国の経済拡大にも後押しされています。中国は継続的な都市化プロセスを奨励し、それに耐えており、2030年までにその割合は70%に達すると予測されています。その結果、中国のような国々における建築活動の活発化が、この地域の接着剤産業に拍車をかけると予測されています。すべてのそのような要因は、地域全体の接着剤の需要を増加させる傾向があります。

- 中国国家統計局によると、建設生産額は2021年の29兆3,100億人民元(4兆2,000億米ドル)から増加し、2022年には31兆2,000億人民元(4兆5,000億米ドル)を占めます。さらに、住宅・都市・農村開発省の予測によると、中国の建設部門は2025年以降もGDPの6%を維持すると予想されています。

- Invest Indiaによると、インドの建設産業は2025年までに1兆4,000億米ドルに達すると予想されており、インドの建設産業は250のサブセクターにまたがり、セクターを越えて連携しており、PMAY-Uの技術サブミッションの下で特定された54以上の世界の革新的建設技術がインドの建設セクターの新時代を切り開きます。

- さらに、アジア、北米、太平洋からの旺盛な需要により、韓国の建設業者の海外建築受注は2022年に3年連続で300億米ドルを突破しました。

- これらの要因はすべて、同地域で増え続ける人口、都市化、購買力の増加によって支えられています。VOC排出に関する規制は現在アジア太平洋の多くの地域で実施されており、このことも繊維セメント板(FCB)やセメント接着パーティクルボード(CBPB)などのセメント板の使用を促進する可能性があります。

- したがって、上記の要因から、アジア太平洋は予測期間中に最も高い成長を遂げる可能性が高いです。

ハイブリッド複合材料産業概要

ハイブリッド複合材料市場は適度にセグメント化されています。主要参入企業(順不同)には、LANXESS、DSM、Avient Corporation、Hexcel Corporation、SGL Carbonなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 軽自動車セグメントにおける複合材使用の増加

- 特定のハイブリッド車が複数の脅威から身を守る

- その他の促進要因

- 抑制要因

- 高い加工・製造コスト

- 持続可能性と環境への影響に関する懸念

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 繊維タイプ

- カーボン/ガラス

- カーボン/アラミド

- HMPP/カーボン

- 木材/プラスチック

- その他の繊維タイプ(天然繊維、バサルト繊維など)

- 樹脂タイプ

- 熱硬化性樹脂

- 熱可塑性樹脂

- その他の樹脂タイプ(PEEK(ポリエーテルエーテルケトン)など)

- エンドユーザー産業

- 自動車・輸送機器

- 建設インフラ

- 航空宇宙・防衛

- 海洋

- その他のエンドユーザー産業(スポーツ用品、医療など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Avient Corporation

- DSM

- Gurit Services AG

- Hexcel Corporation

- Huntsman International LLC

- KINECO-KAMAN

- LANXESS

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- RTP Company

- Owens Corning

- SABIC

- SGL Carbon

- Simcas Composites

- Solvay

- TEIJIN LIMITED

- Textum OPCO, LLC

- Toray Advanced Composites

第7章 市場機会と今後の動向

- 様々な市場におけるハイブリッド複合材料の採用拡大

- 複合材料製造の自動化、デジタル化、積層造形技術の探求

目次

The Hybrid Composites Market size is estimated at USD 2.34 billion in 2025, and is expected to reach USD 3.77 billion by 2030, at a CAGR of greater than 10% during the forecast period (2025-2030).

The impact of the COVID-19 pandemic on the hybrid composites market was mixed. While it presented immediate challenges, it also highlighted the potential of these materials and triggered trends that could contribute to long-term growth.

Lockdowns and travel restrictions disrupted the flow of raw materials and finished products, leading to production delays and material shortages. Industries heavily reliant on hybrid composites, such as aerospace, automotive, and wind energy, experienced significant downturns due to travel restrictions and economic slowdown, dampening demand for material. On the flip side, the pandemic highlighted the need for advanced materials in medical devices and equipment, creating opportunities for biocompatible hybrid composites in prosthetics, implants, and surgical instruments.

Key Highlights

- The growing adoption of composite materials in the light vehicle sector and compared to traditional composites, better properties exhibited by hybrid composites in comparison to the traditional composites is a major driving factor for the market studied.

- On the flip side, the processing and manufacturing of hybrid composites often involve complex and labor-intensive techniques, driving up costs and may act as a hindrance to the growth of the market studied.

- Exploring automation, digitalization, and additive manufacturing techniques for composite production can streamline processes, reduce costs, and improve product consistency can provide lucrative opportunities in the global market.

- Asia-Pacific is expected to witness the highest growth rate during the forecast period owing to the high demand from China.

Hybrid Composites Market Trends

Carbon/Glass to Dominate the Market

- The most commonly used hybrid composites are glass fiber-reinforced polymer (GFRP) and carbon fiber-reinforced polymer (CFRP) composites, followed by composites reinforced by aramid or natural fibers.

- Hybrid carbon fiber/glass fiber material is a lightweight and high-strength alternative for traditional fiberglass and metal applications in the automotive & transportation, building & construction, and other industrial markets.

- The hybrid material offers the performance benefits of carbon fiber at a cost similar to high-performance fiberglass.

- Increased application of hybrid composites in automation and fast-paced manufacturing processes meet mass production requirements in automotive and other sectors.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), in 2022, around 85.01 million vehicles were produced across the globe, witnessing a growth rate of 5.99% compared to 80.205 million vehicles in 2021, thereby indicating an increased demand for metal hoses from the automotive industry. In 2022, around 60 million passenger cars were manufactured worldwide, up nearly 7.35% compared to 2021.

- Users can get up to 90% of carbon's benefits at a cost much lower than what they would have to incur in case of using carbon fiber.

- Parts made out of these hybrid composites provide a high strength-to-weight ratio and are devoid of corrosion. These have extended service life, requiring less maintenance. Their particular properties meet the needs of applications that lay utmost importance on safety and strength.

- In building and construction, many composite products and applications are gaining more and more traction thanks to their unique properties (e.g., corrosion resistance, insulation, lightweight). From composite rebars for reinforcing concrete to pultruded profiles for window frames and composite roofing tiles, composite products not only enable more sustainable designs but also provide an effective solution to repair, upgrade, or strengthen existing buildings, bridges, etc.

- As per JEC Composites, interest in recycling and reusing materials is high, and key players in the composites industry are involved in many initiatives. The application sectors are also setting ambitious goals in this area, e.g., Europe's wind industry is committing to reusing, recycling, or recovering 100% of turbine blades by 2025.

- Owing to the factors mentioned above, carbon/glass fiber type is likely to dominate the market during the forecast period.

Asia-Pacific to Witness the Highest Growth Rate

- The infrastructure industry in Asia-Pacific has been growing at a healthy rate in recent times. Hence, it is estimated that the region will witness a tremendous growth rate in the cement board market over the assessment period.

- The Asia-Pacific region is currently experiencing high investments in residential and commercial construction, especially in China, Japan, Taiwan, and South Korea, and in developing economies such as India, Malaysia, Indonesia, and Vietnam.

- According to JEC Composites, In the future, long-term trends should resume, with economic growth driven by emerging Asia: China's growth is expected to exceed 5% CAGR per annum, higher than Europe and the US; India, Philippines, Indonesia, and Malaysia should grow at a comparable rate. In the mid-term (2021-2026), the composites market should resume growth in all regions, and there is still substantial potential for long-term growth, especially in Asia (energy, E&E, ...).

- In automotive, these unique materials, combining the strengths of various fibers and resins, offer a winning combination of lightweight, enhanced performance, and improved fuel efficiency, leading to increased consumption of hybrid composites in the Asia-Pacific market.

- The Chinese automotive manufacturing industry is the largest in the world. The industry witnessed a slight growth in 2022, wherein production and sales increased. A similar trend continued in 2021, with production witnessing a 3% incline in 2022. According to the China Association of Automobile Manufacturers (CAAM), automotive production is expected to grow in the future, with companies like BYD, SAIC Motors, and more increasing their automotive production sales in the fuel-run and electric vehicles segment.

- According to the China Association of Automobile Manufacturers, Chinese automakers are anticipated to report sales of approximately 9.4 million electric vehicles and hybrids in the previous year, up from 6.9 million in 2022. The association further projects a continued increase in sales for 2024, reaching 11.5 million units.

- For Example, China's automotive giant BYD sold over 3 million battery-powered cars in 2023, of which both batteries and gasoline power 1.6 million fully electric vehicles and another 1.4 million hybrids. Together, that is a 62 percent increase over 2022. BYD is also making money, tripling its profit to USD 1.5 billion in the first half of last year, according to BYD.

- According to India Today, 4,108,000 cars were sold in the domestic market in 2023. This was the first time during a calendar year that over 4 million units were sold in the country. In 2022, the industry witnessed sales of 3,792,000 units. In India, major automotive manufacturers, like Maruti, Hyundai, Tata, Honda, and Mahindra, have shut down their production owing to the unsold stock. This is expected to have a substantial negative impact on India's automotive production in the near future.

- China has one of the largest healthcare sectors in the world. Under the 13th Five-Year Plan, the Government of China prioritized health and innovation, which is expected to increase investments in the medical device manufacturing sector during the forecast period. Additionally, due to the COVID-19 outbreak, investment in the healthcare sector has been gradually growing in the country.

- Hybrid composites can achieve exceptional strength-to-weight ratios, exceeding even steel in some cases. This makes them ideal for load-bearing structures, bridges, and earthquake-resistant buildings.

- China's growth is also fueled by rapid expansion in the residential and commercial building sectors and the country's expanding economy. China is encouraging and enduring a continuous urbanization process, with a projected rate of 70% by 2030. As a result, increased building activity in nations like China is projected to fuel the region's adhesive industry. All such factors tend to increase the demand for adhesives across the region.

- According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.31 trillion (USD 4.2 trillion) in 2021. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- As per Invest India, the construction industry in India is expected to reach USD 1.4 Trillion by 2025, and the construction industry in India works across 250 sub-sectors with linkages across sectors and over 54 global innovative construction technologies identified under a Technology Sub-Mission of PMAY-U to start a new era in Indian Construction Sectors.

- Furthermore, South Korean builders' overseas building orders have surpassed 30 billion US dollars for the third consecutive year in 2022, owing to strong demand from Asia, North America, and the Pacific Ocean regions.

- All of these factors will be supported by the ever-increasing population in the region, urbanization, ion, and their increasing purchasing power. Regulations related to VOC emissions are currently being implemented in many regions of Asia-Pacific, and this might also drive the usage of cement boards such as fiber cement board (FCB) and cement bonded particleboard (CBPB).

- Hence, owing to the factors mentioned above, Asia-Pacific is likely to witness the highest growth during the forecast period.

Hybrid Composites Industry Overview

The hybrid composites market is moderately fragmented in nature. The major players (not in any order) include LANXESS, DSM, Avient Corporation, Hexcel Corporation, and SGL Carbon, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Composite Material in Light Vehicle Segment

- 4.1.2 Specific Hybrids offer Multi-threat Protection

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Processing and Manufacturing Costs

- 4.2.2 Concerns about Sustainability and Environmental Impact

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Fiber Type

- 5.1.1 Carbon/Glass

- 5.1.2 Carbon/Aramid

- 5.1.3 HMPP/Carbon

- 5.1.4 Wood/Plastic

- 5.1.5 Other Fiber Types (Natural Fibers, Basalt Fibers, etc.)

- 5.2 Resin Type

- 5.2.1 Thermoset Resins

- 5.2.2 Thermoplastic Resins

- 5.2.3 Other Resin Types (PEEK(Polyether Ether Ketone), etc.)

- 5.3 End-user Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Construction and Infrastructure

- 5.3.3 Aerospace and Defense

- 5.3.4 Marine

- 5.3.5 Other End-user Industries (Sporting Goods, Medical, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East & Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 UAE

- 5.4.5.7 Rest of Middle-East & Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Avient Corporation

- 6.4.2 DSM

- 6.4.3 Gurit Services AG

- 6.4.4 Hexcel Corporation

- 6.4.5 Huntsman International LLC

- 6.4.6 KINECO - KAMAN

- 6.4.7 LANXESS

- 6.4.8 Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- 6.4.9 RTP Company

- 6.4.10 Owens Corning

- 6.4.11 SABIC

- 6.4.12 SGL Carbon

- 6.4.13 Simcas Composites

- 6.4.14 Solvay

- 6.4.15 TEIJIN LIMITED

- 6.4.16 Textum OPCO, LLC

- 6.4.17 Toray Advanced Composites

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Adoption of Hybrid Composites into Various Markets

- 7.2 Exploring Automation, Digitalization, and Additive Manufacturing Techniques for Composite Production

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日