プライマー-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Primer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641865

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

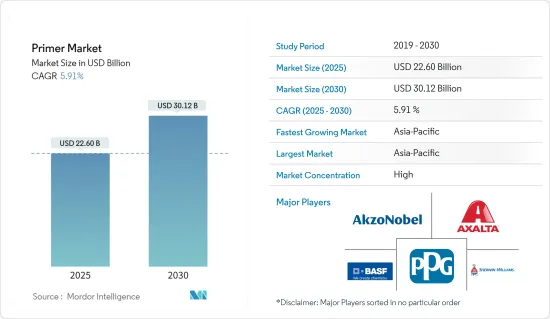

プライマー市場規模は2025年に226億米ドルと推定され、予測期間(2025~2030年)のCAGRは5.91%で、2030年には301億2,000万米ドルに達すると予測されます。

COVID-19パンデミックは、新たなCOVID-19感染者の拡大を抑えるために建設と自動車製造活動が一時的に停止され、それによってこれらのエンドユーザー産業におけるプライマーの消費が減少したため、市場にマイナスの影響を与えました。しかし、この状況は2021年に回復し始めました。このため、予測期間中は同製品の需要が増加すると見込まれます。

主要ハイライト

- 短期的には、アジア太平洋における建設活動の増加と自動車産業の成長が市場の成長を牽引するとみられます。

- その反面、プライマーの使用に関する規制が市場成長の妨げになる可能性が高いです。

- バイオベースのプライマー使用における技術革新は、市場成長の機会として作用すると予想されます。

- アジア太平洋は世界最大の市場であり、インド、中国、その他の国々からの需要と消費が最も多く、世界市場を独占すると予想されます。

プライマー市場動向

建築・建設セグメントが市場を独占する

- プライマーは建築・建設セグメントで広く使用されています。塗料を塗る前に、壁やその他の下地に下塗りとして使用されます。

- プライマーは、アンダーコートやトップコートを塗布する前に、新しい表面や古い表面に塗布される顔料塗料です。建設産業の成長は、塗料とコーティング剤の需要増加に大きな役割を果たしています。建設活動の数が増えれば増えるほど、塗料やコーティング剤の需要も増え、それが最終的にプライマー市場を押し上げることになります。

- 建築・建設産業は、人口の増加、新都市の開発、都市部における移民の増加、既成都市における老朽インフラの更新などの要因により、ここ数年成長を続けており、2030年には4兆4,000億米ドルの売上高に達すると予想されています。

- 北米の建設産業では米国が大きなシェアを占めています。米国、カナダ、メキシコも建設部門投資に大きく貢献しています。

- 米国国勢調査局によると、2023年の米国の年間建設額は1兆9,787億米ドルで、2022年比で約7.03増加しました。

- アジア太平洋の建設セクターは世界最大です。人口増加、中間所得層の増加、都市化により、健全な成長率を示しています。

- 中国とインドにおける住宅建設市場の拡大により、アジア太平洋で最も高い成長が見込まれています。これらの国々は、2030年までに世界の中間層の43.3%以上を占めるようになると予想されています。

- したがって、上記の要因は今後数年間、市場に大きな影響を与えると予想されます。

アジア太平洋が市場を独占する

- 予測期間中、アジア太平洋が最大の成長を遂げると予想されます。これは、同地域の建設産業と自動車生産が成長しているためです。

- アジア太平洋には、インド、中国、インドネシア、ベトナムのような新興経済国が多数あります。そのため、投資家が関心を寄せる市場となっています。

- 2030年までに、世界の建設市場は8兆米ドル規模になると予想されています。インド、中国、米国といった国々がこの成長の大部分を牽引すると予想されています。

- 中国は建設ブームに沸いています。同国は世界最大の建築市場を有しており、世界の建設投資全体の20%を占めています。2030年までに、中国だけで約13兆米ドルの建築投資が見込まれています。

- 中国国家統計局によると、2023年の中国の建設産業の総生産額は1.99%増加し、71兆2,847億2,000万人民元(10兆867億8,000万米ドル)を占めます。

- さらに、インドでは住宅部門が成長しており、政府の支援とイニシアチブが需要をさらに押し上げています。2022~2023年の予算で、住宅都市開発省(MoHUA)は住宅建設と停止中のプロジェクトを完了させるための資金作りに約98億5,000万米ドルを割り当てました。

- 建設産業とともに、自動車産業もこの地域の主要産業であり、プライマーの大きな需要に貢献しています。

- アジア太平洋は、世界で最も価値のある自動車メーカーの本拠地です。中国、インド、日本、韓国のような国々は、収益性を高めるため、製造拠点の強化と効率的なサプライチェーンの開発に力を入れています。

- 中国汽車工業協会(CAAM)によると、中国は世界で最も重要な自動車生産拠点であり、2023年の自動車総生産台数は3,016万台で、昨年の2,702万台に比べて11.6%の増加を記録します。国際貿易局(ITA)によれば、国内の自動車生産台数は2025年までに3,500万台に達すると予想されています。

- さらに、インドの自動車産業は世界第5位であり、2030年には第3位になると予測されています。国際自動車建設機構(OICA)によると、2023年のインドの自動車生産台数は約7%増加し、585万台となりました。

- 上記の要因は、今後数年間、市場に大きな影響を与えると考えられます。

プライマー産業概要

プライマー市場は統合された性質を持っています。主要企業(順不同)には、AkzoNobel NV、The Sherwin-Williams Company、Axalta Coating Systems LLC、PPG Industries Inc.、BASF SEが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア太平洋における建設活動の増加

- 成長する自動車産業

- その他の促進要因

- 抑制要因

- プライマーの使用に関する厳しい環境規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- コンポーネント別

- 樹脂

- アクリル

- エポキシ樹脂

- ポリ酢酸ビニル

- アルキド

- その他の樹脂(マレイン酸、ポリエステル、ポリアミドなど)

- 添加剤別

- 分散剤

- 殺生物剤

- 表面改質剤

- その他添加剤(防錆剤、塩害防止剤、乳化剤、安定剤など)

- その他の成分(溶剤、顔料など)

- 樹脂

- エンドユーザー産業別

- 自動車

- 建築・建設

- 家具

- 工業用

- 包装

- その他のエンドユーザー産業(金属加工、プラスチック、ゴム)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AkzoNobel NV

- Asian Paints

- Axalta Coating Systems LLC

- BASF SE

- Berger Paints India Limited

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd

- Masco Corporation

- NIPSEA Group

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

- Tikkurila

第7章 市場機会と今後の動向

- バイオベースプライマーの革新

- その他の機会

目次

The Primer Market size is estimated at USD 22.60 billion in 2025, and is expected to reach USD 30.12 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market as construction and automotive manufacturing activities were temporarily halted to reduce the spread of new COVID-19 cases, thereby decreasing the consumption of primer in these end-user industries. However, the condition started recovering in 2021. This is expected to increase the demand for the product during the forecast period.

Key Highlights

- Over the short term, the growth of the market is likely driven by increasing construction activities in Asia-Pacific and the growing automotive industry.

- On the flip side, regulations regarding the use of primers are likely to hinder market growth.

- Innovations in the use of bio-based primers are expected to act as opportunities for market growth.

- Asia-Pacific is the largest market in the world and is expected to dominate the global market, with the highest demand and consumption from India, China, and other countries.

Primer Market Trends

Building and Construction Segment to Dominate the Market

- Primer is extensively used in the building and construction sectors. It is used as a preparatory coat on walls and other substrates before applying the paint.

- Primers are pigmented coatings that are applied to new or old surfaces prior to the application of undercoats or topcoats. The growing construction industry plays a keen role in the increasing demand for paints and coatings. The greater the increase in the number of construction activities, the greater the demand for paints and coatings, which will eventually boost the market for primers.

- The building and construction industry has been growing for the past few years, owing to factors such as increasing population, development of new cities, growing migration in urban areas, renewal of old infrastructure in established cities, and others, and it is expected to reach a revenue of USD 4.4 trillion by 2030.

- The United States includes a significant share of the construction industry in North America. The United States, Canada, and Mexico also contribute significantly to the construction sector investments.

- According to the US Census Bureau, the annual value for construction in the United States accounted for USD 1,978.7 billion in 2023, which was an increase of about 7.03 compared to 2022.

- The construction sector in Asia-Pacific is the largest in the world. It is growing at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization.

- The highest growth for housing is expected to be registered in Asia-Pacific, owing to the expanding housing construction markets in China and India. These countries are expected to represent over 43.3% of the global middle class by 2030.

- Therefore, the factors mentioned above are expected to have a significant impact on the market in the coming years.

Asia-Pacific to Dominate the Market

- During the forecast period, Asia-Pacific is expected to witness the maximum growth. This is because the construction industry and automotive production in the region are growing.

- Asia-Pacific has a lot of countries with emerging economies, like India, China, Indonesia, and Vietnam. This has made it a market that investors are interested in.

- By 2030, the global construction market is expected to be worth USD 8 trillion. Countries like India, China, and the United States are expected to drive most of this growth.

- China is amid a construction boom. The country has the world's largest building market, accounting for 20% of all construction investment globally. The country alone is expected to spend nearly USD 13 trillion on buildings by 2030.

- According to the National Bureau of Statistics of China, the gross output value of the construction industry in China in 2023 increased by 1.99%, accounting for CNY 71,284.72 billion (USD 10,086.78 billion).

- In addition, the residential sector in India is growing, and government support and initiatives are further boosting demand. In the budget of 2022-2023, the Ministry of Housing and Urban Development (MoHUA) allocated about USD 9.85 billion to construct houses and create funds to complete the halted projects.

- Along with the construction industry, the automotive industry is another major industry in the region contributing to significant demand for primers.

- Asia-Pacific is home to some of the world's most valuable vehicle manufacturers. Countries like China, India, Japan, and South Korea have been working hard to strengthen their manufacturing bases and develop efficient supply chains for greater profitability.

- According to the China Association of Automobile Manufacturers (CAAM), China has the most significant automotive production base in the world, with a total vehicle production of 30.16 million units in 2023, registering an increase of 11.6% compared to 27.02 million units produced last year. As per the International Trade Administration (ITA), domestic automotive production is expected to reach 35 million units by 2025.

- Further, the Indian automotive industry is the fifth largest in the world and is projected to become the third largest by 2030. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), Indian automotive production in 2023 increased by about 7% and was valued at 5.85 million units.

- The above factors are likely to have a significant effect on the market in the coming years.

Primer Industry Overview

The primer market is consolidated in nature. The major players (not in any particular order) include AkzoNobel NV, The Sherwin-Williams Company, Axalta Coating Systems LLC, PPG Industries Inc., and BASF SE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Construction Activities in the Asia-Pacific Region

- 4.1.2 Growing Automotive Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding the Use of Primers

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Ingredient

- 5.1.1 Resin

- 5.1.1.1 Acrylic

- 5.1.1.2 Epoxy

- 5.1.1.3 Poly Vinyl Acetate

- 5.1.1.4 Alkyd

- 5.1.1.5 Other Resins (Maleic, Polyester, Polyamide, etc.)

- 5.1.2 By Additives

- 5.1.2.1 Dispersant

- 5.1.2.2 Biocides

- 5.1.2.3 Surface Modifier

- 5.1.2.4 Other Additives (Rust Inhibitors, Salt Inhibitors, Emulsifiers, Stabilizers, etc)

- 5.1.3 Other Ingredients (Solvent, Pigments, etc.)

- 5.1.1 Resin

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Furniture

- 5.2.4 Industrial

- 5.2.5 Packaging

- 5.2.6 Other End-user Industries (Metalworking, Plastic, and Rubber)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AkzoNobel NV

- 6.4.2 Asian Paints

- 6.4.3 Axalta Coating Systems LLC

- 6.4.4 BASF SE

- 6.4.5 Berger Paints India Limited

- 6.4.6 Hempel A/S

- 6.4.7 Jotun

- 6.4.8 Kansai Paint Co. Ltd

- 6.4.9 Masco Corporation

- 6.4.10 NIPSEA Group

- 6.4.11 PPG Industries Inc.

- 6.4.12 RPM International Inc.

- 6.4.13 The Sherwin-Williams Company

- 6.4.14 Tikkurila

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation of Bio-based Primers

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日