|

市場調査レポート

商品コード

1640674

欧州の燃料電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Fuel Cell - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の燃料電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

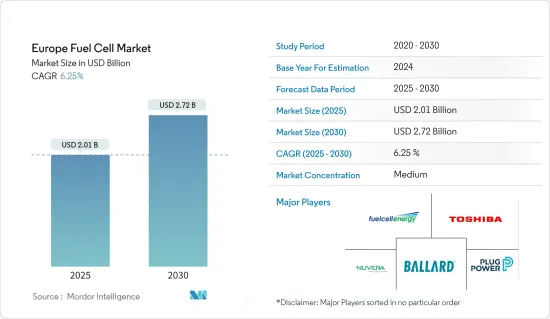

欧州の燃料電池市場規模は2025年に20億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.25%で、2030年には27億2,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、再生可能エネルギー源の適応拡大と政府の支援施策が予測期間中の市場を牽引するとみられます。

- 一方、初期費用が高いことが予測期間中の市場成長の妨げになると予想されます。

- 水素製造とインフラ開拓への注目の高まりは、欧州の燃料電池市場に大きな機会をもたらすと予想されます。

- 欧州の燃料電池市場では、ドイツが大きな役割を果たすと予想されます。ドイツは燃料電池技術を推進する先進国であり、その採用を支援するために様々な施策やイニシアチブを実施しています。

欧州の燃料電池市場動向

輸送産業が市場を独占すると予想

- 燃料電池は、バス、トラック、列車などの大型輸送用途に特に適しています。これらの車両は通常、エネルギー需要が高く、運転距離が長いため、純粋なバッテリー電気ソリューションでは困難です。燃料電池は、ゼロ・エミッション運転を実現しながら、必要なパワーと航続距離を提供することができます。

- 運輸産業は温室効果ガス排出の大きな要因であり、脱炭素化への取り組みが世界的に高まっています。燃料電池は、内燃エンジンに代わるゼロ・エミッションを提供し、輸送による炭素排出を削減するための魅力的なソリューションとなっています。

- 欧州における燃料電池電気自動車(FCEV)の増加は、ゼロ・エミッション輸送への広範な移行の一環として、徐々に勢いを増してきました。国際エネルギー機関(IEA)によると、2023年の燃料電池電気自動車の総台数は、2013年の42台に対し820台となります。この10年間で販売台数は大幅に増加しており、輸送産業における市場の成長機会を示しています。

- さらに、燃料電池には既存のインフラを活用できるという利点があります。水素給油ステーションは既存のガソリンスタンドに組み込むことができるため、電気充電インフラが普及するのに比べ、給油インフラの展開が比較的早いです。

- さらに2023年2月、欧州は2035年からガソリン車とディーゼル車の新車販売を禁止することを正式に決定しました。世界第2位の自動車市場であるこの決定は、欧州議会が自動車メーカーに対し、新たに生産されるすべての自動車からCO2排出を完全にゼロにすることを義務付ける法律を可決したことを受けたものです。これにより、予測期間中に燃料電池電気自動車の販売が増加すると予想されます。

- したがって、こうした新興国市場の開拓を考慮すると、予測期間中は運輸産業が市場を独占すると予想されます。

市場を独占すると予想されるドイツ

- 欧州の燃料電池市場では、ドイツが大きな役割を果たすと予想されます。ドイツは、燃料電池技術の推進における先進国であり、その導入を支援するために様々な施策やイニシアチブを実施してきました。ドイツ政府は、水素と燃料電池の普及に意欲的な目標を設定し、燃料電池技術の研究開発と商業化に多額の資金を割り当てています。

- ドイツは産業基盤が発達しており、製造能力も高いため、燃料電池システムの生産と展開を支援することができます。ドイツには著名な燃料電池メーカー、研究機関、産業団体がいくつかあり、技術の進歩と市場の成長に貢献しています。

- さらに、ドイツの再生可能エネルギーと脱炭素化への取り組みは、クリーンでサステイナブルエネルギーソリューションとしての燃料電池の可能性と一致しています。再生可能エネルギー、特に風力と太陽光への移行は、効率的なエネルギー変換と貯蔵のために燃料電池を統合することで補完することができます。

- さらにドイツは、水素製造施設や燃料補給ステーションを含む包括的な水素インフラを開発する野心的な計画を持っています。このインフラは、燃料電池自動車やその他の水素ベースのアプリケーションの普及に不可欠です。水素インフラ開発への取り組みにより、ドイツは燃料電池普及のリーダーとしての地位を確立しています。

- H2ステーション組織によると、ドイツでは近年、水素充填ステーションの数が大幅に増加しています。2023年には、同国の水素補給ステーションの総数は、2018年の52カ所に対し91カ所となります。

- 2023年1月には、H2 MOBILITY Germanyが運営するベルリンのTempelhofer Weg 102の水素充填ステーションが正式にオープンしました。このステーションは、燃料電池トラック、廃棄物収集車、自動車、小型商用車など、水素で動く車の燃料補給ニーズに応えることが期待されています。特筆すべきは、Tempelhofer Wegの水素ステーションが850kg以上の水素貯蔵能力を誇り、欧州で最も効率的な水素ステーションのひとつであることです。この水素ステーションの成功は、首都における水素モビリティの発展・拡大にとって極めて重要です。

- したがって、こうした点から、予測期間中、ドイツが市場を独占すると予想されます。

欧州の燃料電池産業概要

欧州の燃料電池市場は適度にセグメント化されています。この市場の主要企業(順不同)には、Ballard Power System Inc.、Toshiba Corp.、Fuelcell Energy Inc.、Plug Power Inc.、Nuvera Fuel Cell LLCなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 政府の支援施策とインセンティブ

- 再生可能エネルギーの統合

- 抑制要因

- 初期コストの高さ

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 用途

- ポータブル

- 据置型

- 輸送用

- 燃料電池技術

- 固体高分子形燃料電池(PEMFC)

- 固体酸化物形燃料電池(SOFC)

- その他の燃料電池技術

- 地域

- ドイツ

- フランス

- イタリア

- 英国

- ロシア

- ノルディック

- スペイン

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Ballard Power System Inc.

- Toshiba Corp.

- Fuelcell Energy Inc.

- Nuvera Fuel Cells LLC

- Plug Power Inc.

- AFC Energy

- Topsoe

- Ceres Power

- SFC Energy

- Cummins Inc.

- 市場ランキング分析

第7章 市場機会と今後の動向

- 水素製造とインフラ開発

目次

Product Code: 56719

The Europe Fuel Cell Market size is estimated at USD 2.01 billion in 2025, and is expected to reach USD 2.72 billion by 2030, at a CAGR of 6.25% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adaption of renewable energy sources and supportive government policies are expected to drive the market during the forecasted period.

- On the other hand, the high upfront cost is expected to hinder the market's growth during the forecast period.

- Nevertheless, the increasing focus on hydrogen production and infrastructure development is expected to create huge opportunities for the European fuel cell market.

- Germany is expected to play a major role in the fuel cell market in Europe. Germany has been a leading country in promoting fuel cell technology and has implemented various policies and initiatives to support its adoption.

Europe Fuel Cell Market Trends

Transportation Industry Expected to Dominate the Market

- Fuel cells are particularly suitable for heavy-duty transportation applications such as buses, trucks, and trains. These vehicles typically have higher energy demands and longer operating ranges, making them challenging for purely battery-electric solutions. Fuel cells can provide the required power and range while offering zero-emission operation.

- The transportation industry is a significant contributor to greenhouse gas emissions, and there is a growing global commitment to decarbonizing it. Fuel cells offer a zero-emission alternative to internal combustion engines, making them an attractive solution for reducing carbon emissions from transportation.

- The growth in the number of fuel cell electric vehicles (FCEVs) in Europe has gradually gained momentum as part of the broader transition to zero-emission transportation. According to the International Energy Agency, in 2023, the total number of fuel cell electric vehicles accounted for 820 units compared to 42 units in 2013. Over a decade, the sales number has increased significantly, signifying the growth opportunity for the market in the transportation industry.

- Moreover, fuel cells have the advantage of utilizing existing infrastructure. Hydrogen fueling stations can be integrated into existing gas stations, allowing for a relatively faster rollout of refueling infrastructure compared to widespread electric charging infrastructure.

- Additionally, in February 2023, Europe officially confirmed the prohibition on selling new petrol and diesel cars starting in 2035. As the world's second-largest car market, this decision follows the passing of a law by the European Parliament mandating car manufacturers to achieve complete elimination of CO2 emissions from all newly produced vehicles. This is expected to increase the sales of fuel-cell electric vehicles during the forecasted period.

- Therefore, considering such developments, the transportation industry is expected to dominate the market during the forecast period.

Germany Expected to Dominate the Market

- Germany is expected to play a major role in the European fuel cell market. Germany has been a leading country in promoting fuel cell technology and has implemented various policies and initiatives to support its adoption. The German government has set ambitious targets for hydrogen and fuel cell deployment and has allocated significant funding for research, development, and commercialization of fuel cell technologies.

- Germany has a well-developed industrial base and strong manufacturing capabilities, which can support the production and deployment of fuel cell systems. The country is home to several prominent fuel cell manufacturers, research institutions, and industry associations that contribute to technological advancements and market growth.

- Furthermore, Germany's commitment to renewable energy and decarbonization efforts aligns with the potential of fuel cells as a clean and sustainable energy solution. The country's transition to renewable energy sources, particularly wind and solar, can be complemented by integrating fuel cells for efficient energy conversion and storage.

- Additionally, Germany has ambitious plans to develop a comprehensive hydrogen infrastructure, including hydrogen production facilities and refueling stations. This infrastructure is vital for the widespread adoption of fuel-cell vehicles and other hydrogen-based applications. Germany's commitment to hydrogen infrastructure development positions it as a leader in fuel cell deployment.

- According to the H2 stations organization, the number of hydrogen refueling stations has increased significantly in Germany in recent years. In 2023, the country's total number of hydrogen refueling stations was 91 compared to 52 in 2018.

- In January 2023, the hydrogen refueling station at Tempelhofer Weg 102 in Berlin, operated by H2 MOBILITY Germany, officially opened. This station is expected to cater to the refueling needs of hydrogen-powered vehicles, including fuel cell trucks, waste collectors, cars, and light commercial vehicles. Notably, the Tempelhofer Weg station boasts over 850 kg of hydrogen storage capacity, making it one of Europe's most efficient hydrogen stations. This station's successful operation is crucial for advancing and expanding hydrogen-powered mobility in the capital city.

- Therefore, owing to such points, Germany is expected to dominate the market during the forecast period.

Europe Fuel Cell Industry Overview

The European fuel cell market is moderately fragmented. Some key players in this market (not in particular order) include Ballard Power System Inc., Toshiba Corp., Fuelcell Energy Inc., Plug Power Inc., and Nuvera Fuel Cell LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Supportive Policies and Incentives

- 4.5.1.2 Renewable Energy Integration

- 4.5.2 Restraints

- 4.5.2.1 High Initial Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Portable

- 5.1.2 Stationary

- 5.1.3 Transportation

- 5.2 Fuel Cell Technology

- 5.2.1 Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 5.2.2 Solid Oxide Fuel Cell (SOFC)

- 5.2.3 Other Fuel Cell Technologies

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 Italy

- 5.3.4 United Kingdom

- 5.3.5 Russia

- 5.3.6 NORDIC

- 5.3.7 Spain

- 5.3.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Ballard Power System Inc.

- 6.3.2 Toshiba Corp.

- 6.3.3 Fuelcell Energy Inc.

- 6.3.4 Nuvera Fuel Cells LLC

- 6.3.5 Plug Power Inc.

- 6.3.6 AFC Energy

- 6.3.7 Topsoe

- 6.3.8 Ceres Power

- 6.3.9 SFC Energy

- 6.3.10 Cummins Inc.

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Hydrogen Production and Infrastructure Development