|

市場調査レポート

商品コード

1640663

オフショア支援船-市場シェア分析、産業動向・統計、成長予測(2025~2030年)Offshore Support Vessels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オフショア支援船-市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 237 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

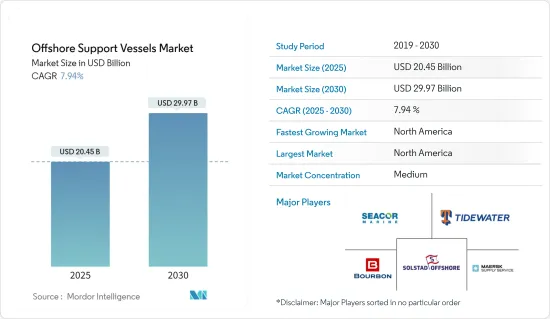

オフショア支援船市場規模は2025年に204億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.94%で、2030年には299億7,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、投資の拡大、石油・ガスの海洋探査・生産活動、洋上風力発電設備の増加が市場需要を牽引すると予想されます。

- その一方で、採掘される商品の価格変動が市場の成長を抑制すると予想されます。

- 海洋船舶の環境問題への対処を支援する新技術は、市場に多くの機会をもたらします。例えば、Maersk Supply Serviceは、非移動船からの排出を排除することで、海運産業における二酸化炭素排出量を削減するために、スティルストレム海洋船舶充電事業を開始しました。長期的には、化石燃料船を着実に廃止していくと考えられます。

- 北米は、この地域で最近起こった大規模な海洋石油・ガスの発見により、予測期間中に市場を独占すると予測されています。

オフショア支援船市場動向

PSV(プラットフォーム供給船)が市場を独占する見込み

- PSV(Platform Supply Vessels)は、海洋掘削リグや生産プラットフォームに機器、消耗品、掘削消耗品を供給するために不可欠です。これらの消耗品には、セメント、重晶石、ベントナイトなどの乾燥粉末、ドリル水、油または水ベースの液体泥水、メタノール、特殊化学品などが含まれます。

- PSVは、陸上基地での積み込みから作業を開始します。二重底タンクで液体貨物を、専用の空気圧タンクでドライバルク貨物を輸送し、船尾のオープンデッキで機器やドリルパイプを運ぶ。リグやプラットフォームに到着すると、リグクレーンが甲板貨物を管理する間に、液体貨物や粉末貨物が空気圧で圧送または移送されます。

- 多くの国々における世界レベルでの石油・ガス需要の増加により、生産者は深海での石油・ガス開発など、より多くの石油資源の探査を行うようになりました。米国では、メキシコ湾(GoM)連邦海洋地域からの原油生産量が、2023年には日量約186万5,000バレルに達します。このような動向は、オフショア石油生産と関連サービスの需要を示しています。

- プラットフォーム補給船(PSV)は、石油・ガス・再生可能エネルギーセグメントでのオフショアロジスティクスサポートの需要増加に牽引され、世界的に大きな成長を遂げています。PSVは、掘削装置、燃料、水などの物資を海上プラットフォームに輸送するために設計された特殊船です。これらの船舶は、海洋施設の継続的な操業を確保し、持続可能で効率的なサプライチェーンへのニーズの高まりをサポートする上で極めて重要です。

- 企業は排出量の削減と運航効率の最適化を目指しており、市場は世界的に環境に優しいソリューションへと移行しています。その顕著な例が、2024年1月にKongsberg Maritimeから先進的なエネルギー貯蔵システム4基の買収を発表したSEACOR Marine Holdings Inc.です。この取り組みは、ハイブリッド電力ソリューションを4隻のSEACOR PSV(SEACORオハイオ、SEACORアルプス、SEACORアンデス、SEACORアトラス)に統合するもので、設置は2024年12月に開始し、2025年半ばまでに完了する予定です。これらのアップグレードは、排出を最小限に抑え、船内のエネルギー効率を高めるという産業の目標に沿ったものです。

- さらに、フリート容量の拡大は、いくつかの企業にとって戦略的な焦点となっています。2023年3月、米国を拠点とするTidewaterは、Solstad Offshoreから37隻のPSVを5億7,700万米ドルで買収し、同社のフリートを228隻(PSV199隻とアンカーハンドリングタグサプライ(AHTS)船を含む)に大幅に増強しました。Tidewaterのフリートは、平均船齢11.3年と、世界的に最も若いフリートのひとつとされており、このセクターの増大する運用ニーズと持続可能性基準に対応するための位置づけとなっています。

- 全体として、プラットフォーム供給船の需要は、予測期間中に大幅な成長が見込まれます。

北米が市場を独占する見込み

- 米国はオフショア支援船(OSV)市場において傑出した参入企業であり、その主要理由は、確立された石油・ガス産業と成長するオフショア再生可能エネルギープロジェクトです。

- メキシコ湾を中心としたオフショア活動が盛んな米国のOSV市場は、伝統的化石燃料探査と新興のクリーンエネルギー源を支えるために不可欠な存在であり続けています。この多様な市場は、サステイナブル代替エネルギーに徐々に移行しつつ、エネルギー安全保障を維持するという米国のコミットメントを反映しています。

- メキシコ湾は、依然として重要な海洋石油・ガスのハブです。例えば、2024年9月、タロス・エナジー社は、米国メキシコ湾の鉱区で商業用石油・天然ガスを大量に発見したと発表しました。

- これらの活動には、探査、掘削、生産をサポートするOSVの継続的な需要が必要です。OSVは、物資の輸送、リグの安定化、海底検査の支援に不可欠であり、継続的な石油・ガス操業に欠かせない存在となっています。

- 国内の複数の企業が、オフショア活動のためのOSVの継続的な需要を支えています。例えば、2024年8月、DOFは米国メキシコ湾での海底契約を獲得しました。この契約は、注水フローライン、船体配管、関連する海底インフラのエンジニアリング、調達、建設、洋上設置を含みます。

- 洋上風力発電容量の拡大を推進する政府の動きは、建設、乗組員の移動、メンテナンスのためのサービスオペレーション船(SOV)やその他のOSVのような特殊船舶の需要を煽っています。

- 例えば、Hornbeck Offshore Servicesは2024年7月、イースタン造船グループと契約し、280フィートのオフショア・サプライ船(OSV)をサービスオペレーション船(SOV)に改造し、米国洋上風力発電市場での急増する需要に対応しました。

- 同国では、沿岸に多数の風力発電所が設置され、洋上風力発電の容量が拡大しています。例えば、2024年9月、イベルドローラの米国子会社であるAvangridが、米国で791MWのニューイングランド・ウインド1洋上風力発電所の開発契約を獲得しました。海岸沿いで新しい風力発電所が開発されるにつれて、OSVはこれらの再生可能エネルギープロジェクトをサポートするためにますます必要とされています。

- 例えば、デンマークのMaersk Supply Serviceは2024年9月、ポーランドのCRISTにDP3クラスのバッテリーハイブリッド推進多目的オフショア支援船(OSV)を発注しました。ABSクラス基準で建造される110メートルのOSVは、ホワイトローズ油田向けのプロジェクト「シードラゴン」の下、MMC Ship Design & Marine Consultingが995L SBC船型設計図を基に設計しました。マースクはこの船を、カナダ東部ニューファンドランド・ラブラドール沖に位置するホワイトローズ油田に長期配備する計画で、油田オペレーターのCenovus Energyに供給します。

- 以上のことから、予測期間中、北アフリカがオフショア支援船市場を独占すると予想されます。

オフショア支援船産業概要

オフショア支援船市場は細分化されています。同市場の主要企業(順不同)には、Tidewater Inc.、Bourbon Corporation SA、Seacor Marine Holdings Inc.、Maersk Supply Service A/S、Solstad Offshore ASAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 洋上風力発電設備の増加

- 石油・ガス開発への投資拡大

- 抑制要因

- 原油価格の高い変動性

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 投資分析

第5章 市場セグメンテーション

- 船種

- アンカーハンドリングタグ/アンカーハンドリング曳船供給船(AHT/AHTSs)

- プラットフォーム供給船(PSV)

- その他

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- 英国

- フランス

- ロシア

- ノルウェー

- イタリア

- ドイツ

- その他の欧州

- アジア太平洋

- 中国

- インド

- 韓国

- ASEAN諸国

- その他のアジア太平洋

- 南米諸国

- ブラジル

- アルゼンチン

- その他の南米諸国

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Bourbon Corporation SA

- Maersk Supply Service AS

- Seacor Marine Holdings Inc.

- Edison Chouest Offshore LLC

- Swire Pacific Limited

- Tidewater Inc.

- Harvey Gulf International Marine LLC

- Solstad Offshore ASA

- Hornbeck Offshore Services Inc.

- PACC Offshore Services Holdings Ltd.

第7章 市場機会と今後の動向

- オフショア船舶の環境問題対応を支援する新技術

目次

Product Code: 56465

The Offshore Support Vessels Market size is estimated at USD 20.45 billion in 2025, and is expected to reach USD 29.97 billion by 2030, at a CAGR of 7.94% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, growing investments, offshore oil and gas exploration and production activities, and rising offshore wind energy installations are expected to drive the market demand.

- On the other hand, the volatility in the prices of extracted commodities is expected to restrain the market growth.

- Nevertheless, new technologies that help offshore vessels deal with environmental problems open up many opportunities for the market. For example, Maersk Supply Service has started its Stillstrom offshore vessel-charging business to reduce carbon emissions in the shipping industry by eliminating emissions from non-moving ships. In the long run, it will steadily phase out fossil-fuel-based vessels.

- North America is predicted to dominate the market during the forecast period due to major offshore oil and gas discoveries that happened in the region recently.

Offshore Support Vessels Market Trends

Platform Supply Vessels (PSVs) Expected to Dominate the Market

- PSVs (Platform Supply Vessels) are essential for delivering equipment, supplies, and drilling consumables to offshore drilling rigs and production platforms. These consumables include dry powders like cement, baryte, and bentonite, drill water, oil or water-based liquid mud, methanol, and specialized chemicals.

- PSVs begin their operations by loading at a shore base. They transport liquid cargo in double-bottom tanks, dry bulk cargoes in specialized pneumatic pressure tanks, and carry equipment and drill pipes on the open deck aft. Upon reaching the rig or platform, liquid and powder cargoes are pumped or transferred pneumatically while the rig crane manages the deck cargo.

- The increase in oil and gas demand at the global level in many countries has prompted producers to explore more petroleum sources, such as deepwater oil and gas exploitation. In the United States, crude oil production from the Gulf of Mexico (GoM) Federal Offshore region reached around 1865 thousand barrels per day in 2023. Such growing trends indicate the demand for offshore petroleum production and related services.

- Platform Supply Vessels (PSV) has witnessed a significant growth globally, driven by the increasing demand for offshore logistics support in the oil, gas, and renewable energy sectors. PSVs are specialized vessels designed to transport supplies like drilling equipment, fuel, water, and other materials to offshore platforms. These vessels are critical in ensuring continuous operations for offshore installations and supporting the growing need for sustainable and efficient supply chains.

- The market globally is moving towards greener solutions as companies aim to reduce emissions and optimize operational efficiency. A notable example is SEACOR Marine Holdings Inc. which, in January 2024, announced the acquisition of four advanced energy storage systems from Kongsberg Maritime. This initiative will integrate hybrid power solutions into four SEACOR PSVs-SEACOR Ohio, SEACOR Alps, SEACOR Andes, and SEACOR Atlas-with installation expected to start in December 2024 and complete by mid-2025. These upgrades align with industry goals to minimize emissions and enhance energy efficiency on board.

- Additionally, expanding fleet capacities has been a strategic focus for some companies. In March 2023, US-based Tidewater acquired 37 PSVs from Solstad Offshore in a USD 577 million deal, significantly boosting its fleet to 228 vessels, which includes 199 PSVs and anchor handling tug supply (AHTS) vessels. Tidewater's fleet is considered one of the youngest globally, with an average age of 11.3 years, positioning it to meet the sector's growing operational needs and sustainability standards.

- Overall, the demand for platform supply vessels is expected to witness significant growth during the forecast period.

North America Expected to Dominate the Market

- The United States is a prominent player in the Offshore Support Vessels (OSVs) market, largely due to its well-established oil and gas industry and growing offshore renewable energy projects.

- With significant offshore activities, particularly in the Gulf of Mexico, the United States OSV market remains essential for supporting traditional fossil fuel exploration and emerging clean energy sources. This diverse market reflects the United States' commitment to maintaining energy security while gradually shifting towards sustainable alternatives.

- The Gulf of Mexico remains a significant offshore oil and gas hub. For instance, in September 2024, Talos Energy announced a significant discovery of commercial oil and natural gas quantities in a block in the United States Gulf of Mexico.

- These activities require a continuous demand for OSVs to support exploration, drilling, and production. OSVs are critical in transporting supplies, stabilizing rigs, and assisting with subsea inspections, making them essential for ongoing oil and gas operations.

- Several companies in the country supported the continuous demand for OSVs for offshore activities. For instance, in August 2024, DOF secured a subsea contract in the US Gulf of Mexico. The contract encompasses engineering, procurement, construction, and offshore installation of a water injection flowline, hull piping, and related subsea infrastructure.

- The government's push to expand offshore wind capacity has fueled demand for specialized vessels like Service Operation Vessels (SOVs) and other OSVs for construction, crew transfers, and maintenance.

- For instance, in July 2024, Hornbeck Offshore Services contracted Eastern Shipbuilding Group to transform a 280-foot offshore supply vessel (OSV) into a service operation vessel (SOV), addressing the surging demand in the United States offshore wind market.

- The country is expanding its offshore wind capacity with numerous wind farms established along its coasts. For instance, in September 2024, Iberdrola's US subsidiary, Avangrid, secured a contract to develop the 791 MW New England Wind 1 offshore wind farm in the United States. As new wind farms are developed along the coasts, OSVs are increasingly needed to support these renewable energy projects.

- For instance, in September 2024, Maersk Supply Service from Denmark ordered a DP3-class, battery-hybrid propulsion multipurpose offshore support vessel (OSV) with Poland's CRIST. The 110-meter OSV, set to be built to ABS class standards, is designed on the 995L SBC hull blueprint by MMC Ship Design & Marine Consulting under the project Sea Dragon for the White Rose oilfield. Maersk plans to deploy this vessel for long-term service at the White Rose oilfield, located offshore Newfoundland and Labrador in eastern Canada, catering to field operator Cenovus Energy.

- Thus, owing to above points, North Amrica is expected to dominate the offshore support vessels market during the forecast period.

Offshore Support Vessels Industry Overview

The offshore support vessel market is semi-fragmented. Some of the major players in the market (in no particular order) include Tidewater Inc., Bourbon Corporation SA, Seacor Marine Holdings Inc., Maersk Supply Service A/S, and Solstad Offshore ASA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Offshore Wind Energy Installations

- 4.5.1.2 Growing Investments In Offshore Oil & Gas Exploration And Production

- 4.5.2 Restraints

- 4.5.2.1 High Volatility Of Crude Oil Prices

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Anchor Handling Tug/Anchor Handling Towing Supply Vessels (AHT/AHTSs)

- 5.1.2 Platform Supply Vessels (PSVs)

- 5.1.3 Other Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Russia

- 5.2.2.4 Norway

- 5.2.2.5 Italy

- 5.2.2.6 Germany

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 South Korea

- 5.2.3.4 ASEAN Countries

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South-America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 Qatar

- 5.2.5.3 United Arab Emirates

- 5.2.5.4 Nigeria

- 5.2.5.5 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Bourbon Corporation SA

- 6.3.2 Maersk Supply Service AS

- 6.3.3 Seacor Marine Holdings Inc.

- 6.3.4 Edison Chouest Offshore LLC

- 6.3.5 Swire Pacific Limited

- 6.3.6 Tidewater Inc.

- 6.3.7 Harvey Gulf International Marine LLC

- 6.3.8 Solstad Offshore ASA

- 6.3.9 Hornbeck Offshore Services Inc.

- 6.3.10 PACC Offshore Services Holdings Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Technologies that Help Offshore Vessels Deal with Environmental Problems