|

|

市場調査レポート

商品コード

1907327

船舶用コーティング:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Marine Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 船舶用コーティング:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

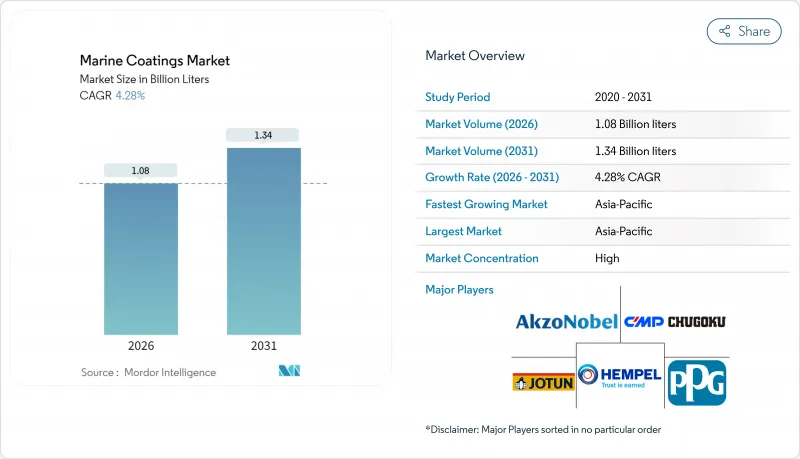

2026年の船舶用コーティング市場規模は10億8,000万リットルと推定され、2025年の10億4,000万リットルから成長し、2031年には13億4,000万リットルに達すると予測されています。

2026年から2031年にかけての年間平均成長率(CAGR)は4.28%となる見込みです。

国際海事機関(IMO)による性能要求の厳しい規制、特にエネルギー効率既存船舶指数(EEXI)および炭素強度指標(CII)により、塗料は維持管理コストから、燃料費と炭素排出量を削減する最前線の解決策へと格上げされました。アジア太平洋地域は世界市場の圧倒的シェアを占め、2024年には全船舶用コーティングの72.11%を供給しています。これは中国が新造船受注の69%という圧倒的なシェアを握っていることに加え、韓国が20%未満のシェアを維持しているためです。カーニバル・コーポレーションが2024年に記録した250億米ドルの収益と、2025年に予定される16隻の新造遠洋クルーズ船の納入スケジュールは、構造的な回復を示しており、これはプレミアム塗料の需要増加につながっています。あらゆる意思決定ポイント、樹脂、技術、用途において、市場は測定可能な燃料節約、低炭素強度スコア、およびより長いサービス間隔を約束するソリューションへと転換しており、価値はもはやチケット価格ではなくライフサイクル経済性にあるという中心的なテーマを裏付けています。

世界の船舶用コーティング市場の動向と洞察

レジャーボート及びクルーズ船の生産増加

レジャークルーズは確実に成長軌道に戻っており、クルーズライン国際協会(CLIA)は2027年までに乗客数が4,000万人に達すると予測しています(2024年の3,170万人から増加)。より大規模な航路と長期航海により、運航会社は優れた光沢保持性と長いドック間隔を実現するプレミアムシリコーンまたはハイブリッドトップコートを指定する傾向にあります。中国がクルーズ船建造国として台頭(国内2隻目の船体現在組立中)したことで、新たな生産能力が加わる一方、高級外装塗料の潜在需要も拡大しています。2025年就航予定の16隻のクルーズ船のうち8隻がLNG推進を採用するため、バンカー作業時の-163℃に耐える極低温対応タンクコーティング及び燃料ラインバリアが求められます。レクリエーションボート分野では、持続的な世帯所得と柔軟なリモートワークモデルが、プレミアムマリンフィニッシュの長期的な需要を支えています。これらの動向が相まって、商業貨物セグメントと比較して平均販売価格と利益率が上昇し、船舶用コーティング市場におけるCAGRを1.2ポイント押し上げる好影響を強化しています。

船舶修理・ドック入り量の増加

紅海危機によるメンテナンスの延期がアジアの造船所を混雑させ、定期用船事業者は最大1年先まで予約を埋める状況です。このバックログは現在、船体洗浄・再塗装需要の上昇サイクルへと転換しており、特にCIIスコアリングの厳格化に直面するパナマックス・スエズマックス級船舶で顕著です。ダメン・シップリペア・ロッテルダム社の代表プロジェクトはこの変化を如実に示しており、船主は従来の剥離型防汚塗料と比較して5~6%の燃料節約効果を約束するシリコン系低摩擦コーティングへの改修を進めています。学術的モデリングによれば、最適な洗浄サイクルにより船舶1隻あたりの年間燃料費を10,402~2万6,685米ドル削減可能であり、投資回収の合理性を裏付けています。需要が最も強いのは世界最古の商用船隊が集中するアジア太平洋地域ですが、EU排出量取引制度(EU-ETS)の課金開始を控え、欧州・北米でも同様の需要急増が見られます。結果として、修理需要に牽引された消費が全体の成長率を0.9ポイント押し上げています。

厳格なVOC及び殺生物剤規制

2023年1月発効の国際海事機関(IMO)によるシブトリン禁止措置は、主要防汚防汚剤を一夜にして排除し、調合メーカーに設計変更サイクルの加速を迫りました。欧州が2024年から中国産二酸化チタンに課す反ダンピング関税は顔料コストを二桁上昇させ、地域塗料連盟やヘッジ規模に乏しい中小塗料メーカーの反発を招いています。ワシントン州の銅使用禁止延期は、環境目標と技術的実現可能性の狭間で進む規制の綱渡りを示していますが、2029年までの継続的な調査は、より厳しい規制上限が延期されただけで撤回されたわけではないことを示唆しています。業界の動向は水性塗料やシリコーン系システムへの移行に向かっていますが、これらは原材料費と検証コストが高くなります。世界の研究開発センターを持たない中小メーカーは、必要な毒性学基準の資金調達に苦慮しており、船舶用コーティング市場の予測成長率を0.8ポイント押し下げています。

セグメント分析

防汚システムは2025年の需要の46.75%を占め、船舶用コーティング市場規模を牽引しました。これは船体の平滑性、燃料消費量、CIIスコアへの直接的な影響を証明するものです。防汚リリース系化学品は、銅不使用の義務化と環境認証を優先するチャーター契約条項の増加を背景に、2031年までCAGR4.52%で拡大が見込まれます。

規模の大きさにもかかわらず、自己研磨型防汚塗料は殺生物剤流出に対する規制監視により成長の限界に直面しています。一方、シリコーンおよびフッ素樹脂系防汚リリース塗料は、初期コストは高いもの、ライフタイム排出量が少なくメンテナンス間隔が長いため、船舶用コーティング市場内での着実な移行経路を強化しています。自己修復添加剤に関する産学共同研究の継続は、次なるイノベーションの波を示唆しております。マイクロカプセルが腐食防止剤を放出したり、傷を埋めるために重合したりすることで、ドッキング間隔をさらに延長することが可能となります。

2025年の出荷量においてアルキド系塗料は54.10%を占め、コスト、噴霧性、世界の入手可能性に関する数十年にわたる最適化を反映しています。しかしながら、この優位性は現在ポリウレタンによって課題を受けており、規制がLNGや水素タンクに適した高強度・低膜厚ライニングを支持する中、2031年までCAGRCAGR4.33%で拡大すると予測されています。

ポリウレタンの台頭は、光沢や耐摩耗性を損なうことなくVOC規制上限値を遵守する水性二液型システムの進歩によって後押しされており、クルーズ船の上部構造物や上部構造区域での仕様採用に貢献しています。並行して進められている動的ジスルフィド交換反応の調査により、常温で微細なひび割れを修復する自己修復層が実現されつつあります。この特性は海軍艦艇のメンテナンス時間を削減する可能性があります。こうした進展により、アルキド樹脂は船舶用コーティング市場においてコスト重視の作業船向けニッチ市場を維持しつつも、シェアを徐々に譲り渡すことになるでしょう。

本海洋塗料市場レポートは、タイプ別(防食塗料、防汚塗料、汚損防止塗料、湿気硬化型)、樹脂別(エポキシ、ポリウレタン、アクリル、アルキド、その他)、技術別(水性、溶剤系、UV硬化型、粉体)、用途別(船舶OEM、船舶アフターマーケット)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分類されています。市場予測は数量(リットル)単位で提供されます。

地域別分析

アジア太平洋地域の71.60%というシェアは、同地域が世界の造船業の中心地としての役割を担っていることを示しています。中国単独で未納船舶受注の69%を占めており、この規模は運賃サイクルがどう変化しても、最低限の塗料使用量を保証するものです。2031年までの地域CAGR4.58%は、クルーズ船建造の拡大、沿岸貿易の増加、日本・韓国・台湾沖での初期段階の洋上風力発電プロジェクトによって牽引されます。日本の国内造船所向け69億米ドルの支援策(米国海軍艦艇向けサービスに充てられる)は、高度なプライマーおよび船体システム向けの新たな高付加価値市場を創出します。

欧州は規制厳格化の指標であり、高級ヨット、フェリー、海洋インフラ分野でのシェアが、塗料需要の多様性と技術集約性を維持しています。EUが2025年1月より5,000総トン以上の船舶を排出量取引制度に組み入れる決定は、船主に対し、炭素排出コスト削減が可能な低抵抗・低溶剤代替品の選択を促します。浮体式洋上風力発電の世界目標264GWのうち、スコットランド、ノルウェー、イベリア半島沖に相当数が設置される見込みであり、25年保証付きのスプラッシュゾーン用コーティングパッケージが求められます。これはトップクラスのサプライヤーのみが提供可能なものです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- レジャーボートおよびクルーズ船の生産増加

- 船舶修理およびドック入り量の増加

- より厳格な国際海事機関(IMO)のEEXIおよびCII燃料効率規制

- 重負荷塗料を必要とする洋上再生可能エネルギー設備の急増

- 銅フリー防汚剤配合への移行

- 市場抑制要因

- 厳格なVOCおよび殺生物剤規制

- エポキシ樹脂および酸化チタンの価格変動性

- 高い塗布・維持管理コスト

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- 防食

- 防汚塗料

- ファウルリリース

- 湿気硬化

- 樹脂別

- エポキシ樹脂

- ポリウレタン

- アクリル

- アルキド樹脂

- その他(フッ素樹脂、ポリエステル等)

- 技術別

- 水性塗料

- 溶剤系

- UV硬化

- 粉末

- 用途別

- 船舶OEM

- 船舶アフターマーケット

- 地域別

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- マレーシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- ナイジェリア

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- AkzoNobel N.V.

- Arkema S.A.(Bostik Yacht Coatings)

- Axalta Coating Systems

- BASF SE

- BOERO BARTOLOMEO S.p.A.

- Carboline Company

- Chugoku Marine Paints Ltd.

- Engineered Marine Coatings LLC

- Hempel A/S

- Jotun

- Kansai Paint Marine Co., Ltd.

- KCC Corporation

- MCU Coating International

- Nippon Paint Marine Coatings Co. Ltd.

- Pettit Marine Paints

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company