|

市場調査レポート

商品コード

1907326

欧州の3Dプリンティング市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe 3D Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の3Dプリンティング市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

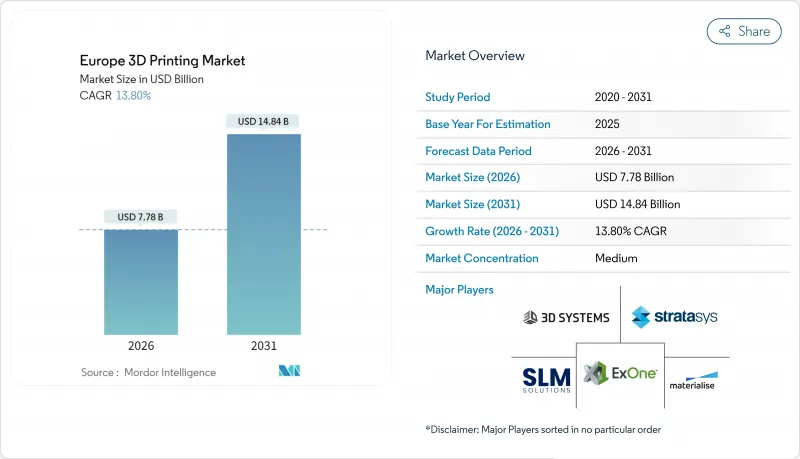

欧州の3Dプリンティング市場は、2025年の68億4,000万米ドルから2026年には77億8,000万米ドルへ成長し、2026年から2031年にかけてCAGR13.8%で推移し、2031年までに148億4,000万米ドルに達すると予測されております。

この拡大は、地域全体の製造業者が分散型生産戦略を加速させていることに起因します。これにより、リードタイムの短縮、サプライチェーンの混乱への備え、そして現地生産を奨励する炭素国境調整措置の要件を満たすことが可能となります。迅速なイノベーションサイクル、金属3Dプリンターのコスト低下、人工知能によるプロセス制御の統合が、自動車、医療、海事産業における生産グレードの使用事例拡大を支えています。ハードウェア販売が依然として収益の大部分を占める一方、サービス志向の「製造サービス(MaaS)」モデルが急速に拡大しており、大規模な資本支出を伴わない柔軟な生産能力を求めるユーザーの意向を反映しています。国別の動向にはばらつきが見られます。ドイツは特許の深さと自動化の専門知識を活用して主導的立場を守り、オランダは世界クラスの物流と海事クラスターを展開して最高の成長ペースを記録しています。既存企業が垂直統合を進め、新規参入者が新素材を推進し、欧州連合が技術基準を調和させて国境を越えた事業運営を容易にする中、競合の激化が進んでいます。

欧州3Dプリンティング市場の動向と洞察

インダストリー4.0およびAM産業への政府主導の取り組みと資金提供

欧州各国政府は、積層造形技術の普及促進に向け多額の資金を投入しております。フランスの540億ユーロ規模の「フランス2030」計画では、先進製造プラットフォーム向けに資金を割り当てております。また「ホライズン・欧州」は、国境を越えた設備をクラウド管理型生産ラインに統合する「サービスとしての製造」パイロット事業をさらに支援しております。ドイツでは、積層造形企業が売上高の30.6%を調査に投資しており、国およびEUの助成金によってさらに強化され、金属システム分野におけるリーダーシップを確固たるものにしています。この共同資金モデルは、研究所から現場への技術移転を促進し、共通の技術基準に沿ったサプライヤーの基盤を構築します。その結果、欧州の3Dプリンティング市場は規模の経済を確保し、中堅企業にとっての参入障壁を低減しています。

自動車メーカーにおける軽量プロトタイピング・金型製造の需要

自動車メーカーは初期プロトタイピングを超えた積層造形を追求しています。EU資金によるMulti-FUNプロジェクトでは、配線やセンサーを軽量構造体に組み込む複合材料造形が明らかになりました。ドイツのサプライヤーは少量生産用工具を造形し、高コストな在庫保管なしで車種固有部品を管理しています。溶接やボルトを削減する単体造形アセンブリを活用することで、企業は軽量化と生産サイクル短縮を実現し、欧州自動車産業の主要地域における3Dプリンティング市場の勢いを維持しています。

高額な設備投資と維持コスト

産業用プリンターは6桁の価格帯であり、ユーザーは粉末処理装置、後処理装置、品質保証装置を追加導入する必要があります。ハードウェア価格が下落しているにもかかわらず、中小企業は購入を先送りするケースが少なくありません。EU医療機器規則への準拠には厳格な文書化と市販後調査が求められ、医療分野の導入企業にとって間接費を押し上げています。鉄道、航空宇宙、エネルギー分野における認証制度の分断は試験予算を増大させ、レンタルやサービスモデルがリスクを相殺するまでは、欧州3Dプリンティング市場の潜在顧客基盤を狭めています。

セグメント分析

サービスプロバイダーは、企業が柔軟性を優先する中で収益シェアを拡大しています。2025年時点で欧州3Dプリンティング市場の67.62%をハードウェアが占めていますが、設計最適化・造形準備・後処理を外部委託する企業が増加する中、サービス指向モデルはCAGR15.97%で拡大しています。K3DやFKMなどの受託製造企業は複数プリンターを運用するファームを展開し、顧客が設備に資本を固定することなくジャストインタイムで部品を入手できるようにしています。この移行により実験コストが低減され、多様な顧客パイプラインにリスクが分散されます。

並行して、ハードウェアベンダーはソフトウェア・保守・トレーニングのサブスクリプションをバンドル化し、機器販売と継続的サービスの境界を曖昧にしています。クラウドダッシュボードは全フリートデータを統合し、予知保全と消耗品補充を可能にします。こうした統合型提供は導入を促進し、欧州3Dプリンティング市場を成果ベースの調達規範へと導いています。

FDMは成熟した材料、低い運用コスト、幅広いユーザー認知度により、2025年においても29.12%と最大のシェアを維持しました。一方DLPは、歯科矯正装置、補聴器、組織足場研究に適した50ミクロン未満の微細加工能力を背景に、14.42%という目覚ましいCAGRを記録しています。植物由来フォトポリマーの進歩は、持続可能性の信頼性を強化すると同時に生体適合性の幅を広げています。SLAおよびSLSは航空宇宙・自動車分野の耐熱部品要求に対応する一方、電子ビーム溶融法は整形外科インプラント用チタン格子構造の主要技術であり続けています。

技術の差別化は現在、自動化と閉ループ制御に依存しています。AI駆動のボクセルレベル補正はサポート材の質量を削減し、脱粉体化を容易にすることで、欧州3Dプリンティング市場全体での稼働率を向上させています。粉末床システムにおけるマルチレーザー協調は生産性と表面仕上げのバランスを実現し、製造業者が部品を量産認定する自信を与えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- インダストリー4.0およびAMに対する政府主導の施策と資金支援

- 自動車OEMにおける軽量プロトタイピングおよび金型製作への需要

- 患者特化型医療機器における医療分野での導入状況

- 金属3Dプリンターおよび材料のコスト低下

- EUの炭素国境調整措置が地域生産を促進

- 鉄道・海運分野におけるオンデマンド部品需要

- 市場抑制要因

- 高い資本投資と維持管理コスト

- 設計段階からのAM対応人材の不足

- EUにおける認証・規格の分断された状況

- 金属粉末の供給変動性とリサイクルの障壁

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- コンポーネント別

- ハードウェア

- サービス

- 技術別

- ステレオリソグラフィー(SLA)

- 溶融積層法(FDM)

- 選択的レーザー焼結(SLS)

- 電子ビーム溶解(EBM)

- デジタル・ライト・プロセッシング(DLP)

- その他の技術

- 素材別

- ポリマー

- 金属および合金

- セラミックス

- 複合材料およびその他

- エンドユーザー業界別

- 自動車

- 航空宇宙・防衛産業

- ヘルスケア

- 建設・建築

- エネルギー・公益事業

- 食品・飲料

- その他産業

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Stratasys Ltd.

- 3D Systems Corporation

- EOS GmbH

- General Electric Company(GE Additive)

- Hoganas AB(Digital Metal(R))

- Sisma S.p.A.

- ExOne Company

- SLM Solutions Group AG

- HP Inc.

- Ultimaker B.V.

- Materialise N.V.

- voxeljet AG

- Renishaw plc

- Prodways Group SA

- Arcam AB

- Carbon, Inc.

- Markforged Holding Corp.

- XJet Ltd.

- Photocentric Ltd.

- Desktop Metal, Inc.

- BEAMIT S.p.A.

- DWS Systems S.r.l.

- Farsoon Technologies Europe GmbH

- B9Creations, LLC