|

市場調査レポート

商品コード

1907312

パラキシレン(PX):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Paraxylene (PX) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| パラキシレン(PX):市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

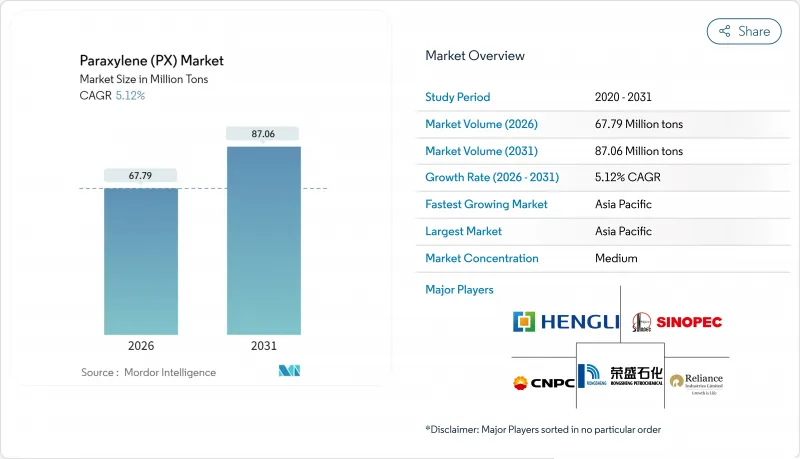

パラキシレン(PX)市場は、2025年の6,448万トンから2026年には6,779万トンへ成長し、2026年から2031年にかけてCAGR5.12%で推移し、2031年までに8,706万トンに達すると予測されています。

パラキシレンの安定供給は、精製テレフタル酸(PTA)が包装材や繊維用のポリエチレンテレフタレート(PET)に直接変換されるため、世界のポリエステル産業を支える基盤となっております。中国における石油化学統合コンプレックスは、原油を直接芳香族化合物に加工する手法によりコスト優位性を有しており、このアプローチにより2024年から2025年にかけて1,000万トン以上の新たなパラキシレン生産能力が追加されました。原料経済性は依然として重要であり、ナフサ価格が前年比16.5%減のトン当たり554.79米ドルとなったことで、供給過剰がスポット価格を圧迫する中でも2025年初頭にマージンが回復しました。需要の回復力は、飲料・パーソナルケア包装、テクニカルテキスタイル、アジア太平洋地域全体での可処分所得の増加に支えられています。一方、バイオベースルートと化学的リサイクルは、既存生産者にとってリスクと機会の両方をもたらします。したがって、競合上の優位性は、規模、統合性、エネルギー効率、そしてブランドの調達戦略に影響を与える持続可能性の要請に対応する能力にかかっています。

世界のパラキシレン(PX)市場の動向と展望

PET包装材の需要急増

飲料、家庭用液体製品、パーソナルケア製品を包装するブランドオーナーは、より重い素材からPETへの代替を進めており、ボトル樹脂重量の約70%を占めるPTA需要を牽引しています。リライアンス・インダストリーズ社は、2024会計年度における世界のPET引き取り量が13%増加したと報告しており、これは小売業者の輸送効率と陳列効果への要求を満たす軽量かつ完全リサイクル可能なボトル形態が促進要因です。オンライン食料品販売や消費者直販チャネルでは、長い流通経路でも破損しにくいPETの特性から、この需要がさらに拡大しています。政府規制では全面禁止ではなく最低再生材含有率の指定が増加しており、これによりバージンパラキシレンは包装需要の伸びに追随しつつ、回収インフラの整備を促進しています。結果として、芳香族化合物とPTAの統合設備を有する製油所は、予測可能なベースロード需要を確保でき、輸送用燃料が周期的な低迷期にあっても収益を安定させることが可能です。

アジアにおけるポリエステル繊維の拡大

アジア太平洋地域は依然として世界の繊維生産拠点であり、パラキシレン価格の変動にもかかわらず、ポリエステルが綿花に対して持つコスト優位性が繊維需要を支えています。中国では2024年に400万トン以上の新規ポリエステル短繊維生産能力が稼働を開始し、インドでは国内衣料品輸出を促進するため、化学繊維を対象とした業績連動型奨励制度が承認されました。自動車用エアバッグ、コンベアベルト、ジオテキスタイル向けテクニカルテキスタイルの需要は、安定した高マージン供給を必要とするため、PTAの継続的な供給に依存しています。ジャムナガルと大連の統合複合施設では、パラキシレン、PTA、繊維紡績を同一拠点に集約することで輸送コストを削減し、地域競争力を強化しています。ファストファッションブランドは発注サイクルを加速させており、工場側はジャストインタイムのPTA納入を保証できるサプライヤーを優先します。この能力は、中国東部沿岸省の大型統合クラスター内で最も実現可能です。

使い捨てプラスチック規制の強化

欧州連合(EU)の使い捨てプラスチック指令は特定テイクアウト用品を禁止し、拡大生産者責任制度による費用を課すことで、バージンPETを使用するコンバーター企業のコンプライアンスコストを増加させます。カリフォルニア州の類似提案では、2028年までに飲料ボトルの再生材含有率25%を義務付け、ブランドオーナーはニッチSKU向けにアルミや紙ベースのソリューションへの多様化を迫られています。操業面では、パラキシレン需要はファストフード包装分野で停滞する可能性がありますが、無菌ジュースや乳製品などの高バリア性PET用途は性能要件により保護された状態が続きます。この結果、成熟市場の成長は鈍化する一方、樹脂の流れは単純な使用量制限ではなく、現実的なリサイクル目標を設定する地域へと再配分される見込みです。

セグメント分析

精製テレフタル酸は2025年に世界生産量の94.35%を占め、パラキシレン市場の主要な販路としての地位を確固たるものにしております。江蘇省、浙江省、グジャラート州で進行中のPTA拡張規模は、セグメント全体のアロマティック供給を上回る成長を示し、2031年までにCAGR5.32%を達成する見込みです。製油所から化学品への統合が進むことで稼働率の柔軟性が高まり、パラキシレンとPTAユニット間の物流移送が最小化され、原料供給の安定性が確保されます。その結果、単一サイトにおけるメガプロジェクトのPTA生産能力は年間300万トンを超え、スポット市場におけるパラキシレンプレミアムの価格変動を緩和する規模経済を実現しています。デジタルツインモデルによる熱統合ネットワークの最適化により、エネルギーコストを10~12%削減し、排出量を低減。欧州の輸出顧客がスコープ1炭素排出制限の遵守を求められる状況下で、この優位性が発揮されます。

テレフタル酸ジメチル(DMT)のニッチ市場は縮小傾向にあります。これは、ライセンス取得企業が転エステル化ラインの廃止を進めており、直接PTAルートと比較して変動費が15~20%高いことを理由としているためです。特殊溶剤、可塑剤、除草剤中間体は、パラキシレン消費量の残りの1~2%を占めており、中程度の単一桁成長を示していますが、総需要を左右するには不十分です。しかしながら、改質芳香族プール内の異性体比率調整において重要性を維持しており、単一分子ではなく製油所全体の価値を最大化する生産計画を可能にしております。代替となるバイオ芳香族は有望視されるもの、商業生産量は依然としてごく僅かで、見通し期間中は従来型PTAがパラキシレン市場を主導し続けることを示唆しております。

パラキシレン(PX)市場レポートは、用途別(精製テレフタル酸、テレフタル酸ジメチル、その他用途)、エンドユーザー産業別(プラスチック、繊維、その他エンドユーザー産業)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分類されています。市場予測は数量(トン)単位で提供されます。

地域別分析

アジア太平洋地域は2025年に82.10%のシェアでパラキシレン市場を独占し、中国、インド、東南アジアが下流のポリエステルエコシステムを強化する中、2031年まで5.48%のCAGRを維持すると予測されています。中国の石油化学集中化戦略により、2024年から2025年にかけて5つの新複合施設が稼働を開始し、それぞれパラキシレン、PTA、ポリマーの統合ユニットを備えています。大宇山(Dayushan)単独でも年間1,180万トンの芳香族化合物を生産しています。インドではジャムナガルの140万トン級パラキシレンプラントと、同国が拡大するテクニカルテキスタイル輸出優遇策を活用し、地域の自給率向上とアパレル製造クラスターへの外資誘致を推進しています。日本と韓国は引き続き高規格パラキシレンを供給していますが、国内需要が頭打ちとなる中、生産能力の合理化が迫られています。

北米は規模こそ小さいもの、戦略的に重要な世界シェアを維持しています。混合キシレン原料はガソリン混合時に高いオクタン価を発揮するため、燃料需要がピークとなる季節には単独PXの利益率がアジアを下回ります。しかしながら、高度なCCR設備の改修と豊富なシェールコンデンセートの供給により、原料の多様性は維持されています。北米のパラキシレン市場規模は2031年までに447万トンに拡大する可能性があります。この増加分は、物流チェーンの短縮を重視する消費財ブランドに近い立地で進められる特殊PETおよびバイオPXパイロットプラントに起因します。化学的リサイクル素材への政策支援により調達源はさらに多様化しますが、予測期間内における新規PXの絶対的な代替効果は限定的です。

欧州ではエネルギーコストと規制コストの上昇が課題となり、中東・アジアからの輸入が増加しています。天然ガスの高値が継続することで蒸気クラッカーのユーティリティ費用が上昇し、現地PXの競争力が低下しています。しかしながら、使い捨てプラスチック規制により需要は完全リサイクル可能なPETへシフトしており、クローズドループリサイクル方式を採用するPTAプラントのベースロード需要は維持される見込みです。中東地域は、余剰ナフサと改質油を芳香族製品へ転換し、アジアのポリエステル大手企業との輸出契約に注力することで、世界の供給バランスを逼迫させています。南米の需要はブラジルの飲料セクターが中心であり、構造的なPX貿易赤字が生じていますが、米国メキシコ湾岸およびアラビア湾岸の輸出業者との長期供給契約によって対応されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- PET包装材の需要急増

- アジアにおけるポリエステル繊維の拡大

- 軽量でリサイクル可能な飲料ボトルがPX需要を牽引

- 高収率CCRおよびPRT芳香族ユニットの商業化

- バイオベースパラキシレンの商業規模パイロットプラント(非化石)

- 市場抑制要因

- 使い捨てプラスチック規制の強化

- 原油主導の原料価格変動性

- 新興化学リサイクルによるバージンPXの代替

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- 精製テレフタル酸(PTA)

- テレフタル酸ジメチル(DMT)

- その他の用途

- エンドユーザー産業別

- プラスチック

- テキスタイル

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- タイ

- インドネシア

- マレーシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- ナイジェリア

- エジプト

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- China Petrochemical Corporation

- CNPC

- Eneos Corporation

- Exxon Mobil Corporation

- FCFC

- GS Caltex Corporation

- Hengli Petrochemical Co., Ltd.

- Idemitsu Kosan Co.,Ltd.

- Ineos

- LOTTE CHEMICAL CORPORATION

- PTT Global Chemical Public Company Limited

- Reliance Industries Limited

- Rongsheng Petrochemical Co., Ltd.

- S-oil Corporation

- TotalEnergies