|

市場調査レポート

商品コード

1851469

相変化材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Phase Change Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 相変化材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月01日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

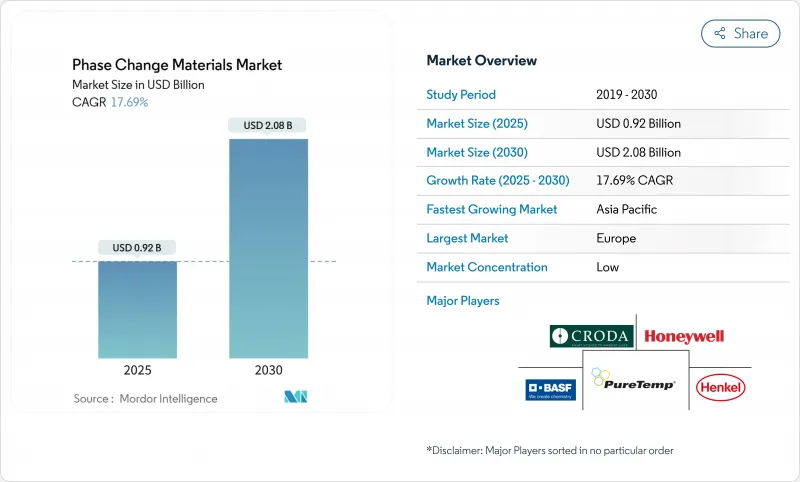

相変化材料市場規模は2025年に9億2,000万米ドルと推定・予測され、2030年には20億8,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは17.69%です。

長期化する熱波、ネットゼロ建設目標、輸送の急速な電化により、潜熱蓄熱は現在、商業エネルギー戦略の中心に位置づけられています。また、コールドチェーン・ロジスティクスや電気自動車用バッテリーパックは、輸送、製薬、データセンター冷却など、この技術の応用範囲を広げています。長らく相分離と過冷却の問題で制約を受けてきたソルトハイドレートは、最近の導電性のブレークスルーを受けて牽引力を増しています。同時に、農業残渣由来のバイオベースPCMは、熱容量を犠牲にすることなく火災安全性と持続可能性の懸念に対処し、実験室での好奇心からスケーラブルな商業製品へと移行しています。アジア太平洋地域では、メーカーが高純度塩水和物に関連するサプライチェーンリスクをヘッジするために現地生産ラインを増設しており、生産能力増強の支点へと進化しています。

世界の相変化材料市場の動向と洞察

PCM統合を加速する建築エネルギー基準の義務化

性能に基づく適合基準により、建築家は硬質断熱材を潜熱蓄熱層で代用できるようになり、軽量壁内のピーク冷房負荷を35~45%削減できるようになりました。ミネソタ州での実測結果では、室内ピーク温度が5.49℃低下し、負荷が77.8%オフピーク時間帯にシフトしたことが報告されており、規制当局にHVAC節約の現実的な証拠を提供しています。2027年のEU改修目標に向けた適合基準値の上昇により、PCM入り石膏ボードとコンクリートブロックがさらに重視されるようになり、相変化材料市場全体の調達量が増加すると予想されます。

コールドチェーン物流インフラの急速な展開

ワクチン、高度な生物製剤、精密食肉は、+-0.5℃の偏差を3日未満許容する温度帯を必要とすることが多いです。PCMは、外部電源なしでこの持ちこたえを72時間に延長し、空港や税関での遅延時のディーゼル発電機への依存を削減します。グリセリンー水-NaCl混合物は、アクティブ冷却と比較して二酸化炭素排出量を30~40%削減し、医薬品の保存期間を15~25%延ばし、相変化材料市場全体で2桁の需要をもたらしています。

相変化材料の危険な性質

パラフィンワックスはおよそ170 °Cで発火し、臭素系難燃剤を必要とするためコストがかさみ、健康表示規制の引き金となる可能性があります。LiNO3のような無機難燃剤は毒性リスクがあります。最近のin-situ重合固体ー固体PCMは漏れをなくし、ハロゲンなしでUL94 V-0の燃焼性をクリアしています。より広範な採用は、こうしたカプセル化の進歩を拡大し、世界的な化学安全基準を調和させることにかかっています。

セグメント分析

有機パラフィンワックスは相変化材料市場の収益の柱であり続け、2024年の世界売上高の44.19%を占める。その優位性は、成熟したサプライチェーン、幅広い温度範囲、建築パネルに使用されるマクロカプセル化スラブとの互換性を反映しています。しかし、利害関係者がライフサイクル排出量の削減を追い求める中、相変化材料市場はバイオ由来の油、獣脂、脂肪酸混合物へと急旋回しています。この新興サブセグメントは、2030年までのCAGRが19.21%と他を上回ると予測され、LEEDクレジットや、生物由来材料を明確に推奨する自治体のグリーン調達義務に後押しされています。

パラフィンベースの配合物は、安定した結晶化と0~90℃の範囲での融点の調整が容易なため、2024年の相変化材料市場の収益の41.49%を占めました。それでも、塩水和物はこのヒエラルキーを崩壊させる勢いであり、2030年までのCAGRは18.04%で拡大します。高い体積熱容量(最大350kJ/L)と炭素添加剤による熱伝導率の改善により、塩水和物は部品のサイズと重量の縮小を可能にしています。その結果得られる密度の優位性は、利用可能な設置面積に制約のある電気自動車のバッテリースリーブやコンパクトなデータセンター・ラックにとって特に魅力的です。

地域分析

2024年の世界売上高の32.86%は欧州が占める。これはEUの建築物エネルギー性能指令に支えられたもので、同指令は新築と大規模改修の両方に準ネットゼロ目標の達成を義務付けています。ドイツと北欧では、PCMを外壁断熱システムに組み込んだ後、HVACエネルギーが20~35%節約されたことを、早期採用企業が示しています。炭素取引とグリーンボンド適格性に関する規制の明確化により、PCMを多用する建築材料への資金が引き寄せられ続け、相変化材料市場における欧州の主導的地位が固まりつつあります。

アジア太平洋は最も急成長している地域で、2030年まで毎年18.98%の拡大が見込まれています。中国の積極的なヒートポンプ導入は、「ヒートポンプの未来」ロードマップの下で奨励されている相乗効果により、ピーク電力需要を節約することでPCM蓄熱を補完します。

北米では、厳しいエネルギー規制の更新と、爆発的に成長する電気自動車部門が組み合わさっています。米国のデータセンター事業者は、オンサイトエネルギー貯蔵に対する税額控除を目当てに、PCMベースのサーマルバッファを試験的に導入し、サーバーの熱スパイクを吸収して冷凍機の起動を延期しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- PCM統合を加速させる欧米の建築エネルギー基準の義務化

- コールドチェーン物流インフラの急速な展開

- 自動車の電動化には塩水和物PCMを用いた高度な熱電池パックが必要である

- バイオベースPCMの採用を促進するネット・ゼロ・ビルディングのための政府奨励金

- 省エネと持続可能な発展を目指す世界の動向の拡大

- 市場抑制要因

- 相変化材料の危険性

- 高純度水和塩のサプライチェーン変動性

- 限られた認識と理解

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 原材料分析

- 特許分析

第5章 市場規模と成長予測

- 製品タイプ別

- オーガニック

- 無機

- バイオベース

- 化学成分別

- パラフィン

- ノンパラフィン炭化水素

- ソルトハイドレート

- 共晶

- カプセル化技術別

- マクロカプセル化

- マイクロカプセル化

- 分子カプセル化

- エンドユーザー業界別

- 建築・建設

- パッケージ

- テキスタイル

- エレクトロニクス

- 交通機関

- その他の産業(ヘルスケア、防衛)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的な動き(M&A、JV、提携、資金調達)

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- BASF

- Appvion, LLC.

- Climator

- Croda International Plc

- Cryopak

- DuPont

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Laird Technologies, Inc.

- Microtek

- National Gypsum Services Company

- Outlast Technologies GmbH

- Parker Hannifin Corp

- Phase Change Solutions

- Pluss Advanced Technologies

- PureTemp LLC

- Rubitherm Technologies GmbH

- Shenzhen Aochuan Technology Co.,Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Sonoco Products Company