小売デスクトップ仮想化:市場シェア分析、業界動向、成長予測(2025~2030年)

Retail Desktop Virtualization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640500

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

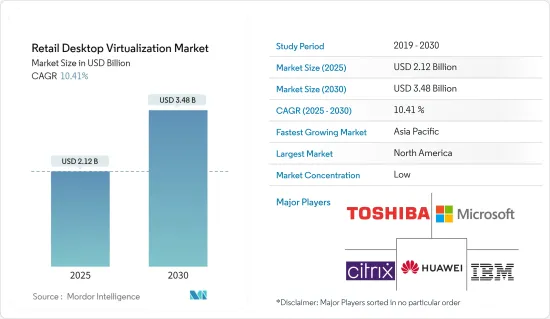

小売デスクトップ仮想化市場規模は、2025年に21億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは10.41%で、2030年には34億8,000万米ドルに達すると予測されます。

小売デスクトップ仮想化市場は、クラウドコンピューティングの急速な普及とさまざまなセグメントでの自動化の進展によって、大きな牽引力となっています。デスクトップ仮想化は、集中管理されたサーバー上でホストされる仮想マシン(VM)内でデスクトップOSを実行するもので、柔軟性、セキュリティ、コスト効率の向上を目指す企業にとって極めて重要なソリューションとなっています。仮想デスクトップ基盤(VDI)やDaaS(Desktop-as-a-Service)といったプラットフォームを通じて提供されることが多いこの技術は、リモートデスクトップソリューションやアプリケーションの仮想化を可能にし、シームレスな仮想ワークスペースを育みます。

産業分析によると、デスクトップ仮想化は、特にマルチクラウド環境の台頭とエンドユーザーコンピューティング(EUC)ソリューションに対する需要の高まりに伴い、最新のITインフラにとってますます不可欠なものとなっています。仮想マシン(VM)とSoftware-Defined Data Center(SDDC)もまた、この状況において極めて重要な役割を果たしており、企業は仮想デスクトップを効率的に展開できるようになっています。シトリックスシステムズ社、VMware、Microsoftなどの主要企業が市場をリードする中、ハイパーコンバージドインフラ(HCI)やシンクライアントで大きなイノベーションが起きており、競争は激しいです。

企業が引き続き柔軟性とリモートワーク機能を優先する中、仮想デスクトップ導入の需要は拡大すると予想されます。市場展望では、特にデータのセキュリティとアクセシビリティが最重要視される産業において、クラウドデスクトップの採用が着実に増加しています。この変化は市場のセグメンテーションにも反映されており、特に北米や欧州などの地域では、オンプレミスソリューションよりもクラウド展開モードへの傾向が顕著です。

デスクトップ仮想化を促進するクラウドコンピューティングの役割

主要ハイライト

- ITインフラの変革:クラウドコンピューティングは従来のITインフラを変革し、デスクトップ仮想化をあらゆる規模の企業にとって実現可能なソリューションにしました。クラウドベースのサービスを活用することで、企業は仮想デスクトップをより効率的に導入し、大規模な物理インフラの必要性を減らすことができます。このシフトは、仮想デスクトップインフラ(VDI)やDaaS(Desktop-as-a-Service)ソリューションのスケーラビリティを実現する上で大きな力となっています。クラウドデスクトップが提供する柔軟性により、企業はリソースを動的に管理することができ、ワークロードの分散と災害復旧が重要なマルチクラウド環境では特に有利です。

- アクセシビリティとコスト効率の向上:クラウドコンピューティングは、アクセシビリティとコスト効率の向上を促進し、企業は多額の先行投資を行うことなく、リモートデスクトップソリューションとアプリケーションの仮想化をサポートすることができます。仮想マシン(VM)の普及により、企業は場所を問わず、従業員に仮想ワークスペースへの安全かつ一貫したアクセスを提供できます。この機能は、モビリティとデータセキュリティが最優先事項である今日の「どこからでも仕事ができる」文化には不可欠です。さらに、クラウドデスクトップは、従来のデスクトップセットアップと比較して、より簡単な管理とアップデートを可能にし、総所有コスト(TCO)を削減します。

小売業における自動化が仮想化需要を後押し

主要ハイライト

- 小売業務の合理化:小売業における自動化の進展は、デスクトップ仮想化の需要に大きく貢献しています。小売業では、業務の合理化、顧客体験の向上、サプライチェーンの効率化を目的に、自動化技術の導入が進んでいます。デスクトップ仮想化は、複数の拠点にまたがるアプリケーション、在庫システム、顧客データを一元管理するプラットフォームを提供することで、こうした取り組みを支援します。小売企業は、リモートデスクトップソリューションを導入することで、業務の同期を確保し、ペースの速い環境では不可欠なリアルタイムのデータアクセスと処理機能を実現できます。

- オムニチャネル戦略のサポート:小売企業がオムニチャネル戦略を開発し続けるにつれ、物理的なプラットフォームとデジタルプラットフォームをシームレスに統合する必要性が顕著になっています。デスクトップ仮想化により、小売企業は、POS(販売時点情報管理)システムからCRM(顧客関係管理)ツールまで、さまざまな機能をサポートする統合ワークスペースを構築できます。この統合は、チャネル間で一貫した顧客体験を提供するために不可欠です。さらに、仮想デスクトップ導入の増加により、小売企業は、機密性の高い顧客情報を取り扱う上で不可欠な、堅牢なセキュリティプロトコルやデータ保護対策を維持することができます。

小売デスクトップ仮想化市場の動向

デスクトップ仮想化におけるクラウド導入の台頭

- クラウド導入の動向:クラウド導入は、デスクトップ仮想化市場において極めて重要な動向となっており、その背景には、コスト効率が高く、拡大性があり、管理が容易なソリューションに対するニーズがあります。仮想デスクトップインフラ(VDI)やDaaS(Desktop as a Service)を筆頭に、従来のオンプレミス型からクラウド型への移行が進んでいます。この移行により、企業は仮想デスクトップを迅速に導入できるようになると同時に、初期コストを削減し、柔軟性を高めることができます。マルチクラウド環境の採用は、この傾向をさらに加速させています。企業はベンダーロックインを回避し、運用の回復力を強化しようとしており、さまざまなクラウドプラットフォームで仮想マシン(VM)の普及を促進しています。

- クラウド導入を後押しする主要要因:クラウドコンピューティングの普及により、デスクトップ仮想化の状況は一変し、企業はリソースをより効率的に管理できるようになりました。ハイパーコンバージドインフラ(HCI)が提供するコンピューティング、ストレージ、ネットワークリソースのシームレスな統合が、クラウド導入への嗜好を高めています。さらに、Software-Defined Data Centers(SDDC)の台頭により、企業は仮想化ワークロードの管理が容易になり、運用効率が大幅に向上しています。その結果、ITリソースを最適化するためにクラウドデスクトップソリューションを採用する中小企業が増えており、市場の成長をさらに促進しています。

北米が大きなシェアを占める見込み

- 世界市場をリードする北米:北米は、先進的な技術インフラとデジタルトランスフォーメーション戦略の高い導入率に牽引され、デスクトップ仮想化市場を独占するとみられます。同地域は技術革新に力を入れており、新技術を迅速に統合できることから、市場成長の重要な拠点として位置づけられています。リモートワークや在宅勤務の増加に後押しされたリモートデスクトップソリューションに対する需要の高まりが、この優位性を支える重要な要因となっています。この地域の企業がVDI、DaaS、クラウドデスクトップソリューションを採用するにつれ、北米の市場シェアは大きく成長すると予想されます。

- 主要企業としての米国:北米最大のデスクトップ仮想化消費国である米国は、同地域の市場リーダーとして重要な役割を果たしています。米国には大手クラウドサービスプロバイダーが存在し、ホスティングサーバーの数が増加していることが、クラウドベースのデスクトップ仮想化の成長を促進しています。さらに、カナダに近く、新しいワークスペースでは環境に優しいプラクティスが重視されていることも、この地域での市場の拡大をさらに後押ししています。このような地域間の相互接続性は、デスクトップ仮想化ソリューションの幅広い採用をサポートし、北米のリーダーとしての地位を強化しています。

小売デスクトップ仮想化産業概要

細分化された市場:小売デスクトップ仮想化市場は非常に細分化されており、単一の企業が圧倒的な市場シェアを持つことはないです。この細分化は、世界の大企業と小規模な専門企業の両方が事業を展開する競合環境を示しています。基本的な仮想化から複雑なカスタマイズ導入まで、幅広いソリューションを提供しています。

多様なアプローチで市場をリードする企業デスクトップ仮想化市場の大手企業には、Citrix Systems Inc.、Toshiba Corporation、Red Hat Inc.、IBM Corporation、Huawei Technologies、Microsoft Corporationなどがあります。これらの企業は、強力な世界的プレゼンス、広範な製品ポートフォリオ、継続的なイノベーションによって際立っています。シトリックスとMicrosoftは包括的な仮想化プラットフォームで特に注目され、Red Hat(IBM傘下)とHuaweiはオープンソースとクラウドベースのソリューションの統合に注力しています。Toshiba Corporationのプレゼンスはよりニッチで、特定の産業のニーズに対応しています。

今後の成功戦略はイノベーションと統合が中心デスクトップ仮想化市場の主要動向としては、クラウドベースのソリューション、セキュリティ強化、既存のITインフラとのシームレスな統合に対する需要の高まりが挙げられます。市場参入企業が成功を収めるには、これらのセグメントに注力し、変化する企業ニーズに対応できる柔軟で安全なソリューションを提供する必要があります。継続的なイノベーション、戦略的パートナーシップ、サービス提供の拡大が、この細分化された市場で競合を維持するための重要な戦略となると考えられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要(COVID-19による影響を含む)

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- クラウドコンピューティングの導入拡大

- 小売業における自動化の成長

- 市場抑制要因

- インフラ導入の制約

第6章 市場セグメンテーション

- デスクトップ配信プラットフォーム別

- ホスト型仮想デスクトップ(HVD)

- ホスト型共有デスクトップ(HSD)

- 導入形態別

- オンプレミス

- クラウド

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Citrix Systems Inc.

- Toshiba Corporation

- Red Hat Inc.(IBM Corporation)

- Huawei Technologies Co. Ltd.

- Microsoft Corporation

- Parallels International GmbH

- Dell Inc.

- Ncomputing, Inc.

- Ericom Software Inc.

- Tems, Inc

- Vmware Inc.

第8章 投資分析

第9章 市場の将来

目次

The Retail Desktop Virtualization Market size is estimated at USD 2.12 billion in 2025, and is expected to reach USD 3.48 billion by 2030, at a CAGR of 10.41% during the forecast period (2025-2030).

The desktop virtualization market has gained significant traction, driven by the rapid adoption of cloud computing and increasing automation across various sectors. Desktop virtualization, which involves running a desktop operating system within a virtual machine (VM) hosted on a centralized server, has become a crucial solution for businesses aiming to enhance flexibility, security, and cost efficiency. This technology, often delivered through platforms like Virtual Desktop Infrastructure (VDI) or Desktop as a Service (DaaS), enables remote desktop solutions and application virtualization, fostering a seamless virtual workspace.

Industry analysis reveals that desktop virtualization is becoming increasingly integral to modern IT infrastructures, especially with the rise of multi-cloud environments and the growing demand for end-user computing (EUC) solutions. Virtual machines (VMs) and software-defined data centers (SDDCs) are also playing a pivotal role in this landscape, enabling organizations to deploy virtual desktops efficiently. With companies like Citrix Systems Inc., VMware Inc., and Microsoft Corporation leading the market, the competition is intense, with significant innovation occurring in hyper-converged infrastructure (HCI) and thin clients.

As businesses continue to prioritize flexibility and remote work capabilities, the demand for virtual desktop deployment is expected to grow. The market outlook suggests a steady rise in the adoption of cloud desktops, particularly in industries where data security and accessibility are paramount. This shift is reflected in the market's segmentation, with a noticeable trend towards cloud deployment modes over on-premise solutions, particularly in regions like North America and Europe.

Cloud Computing's Role in Driving Desktop Virtualization

Key Highlights

- Transformation of IT Infrastructure: Cloud computing has transformed traditional IT infrastructures, making desktop virtualization a feasible solution for businesses of all sizes. By leveraging cloud-based services, companies can deploy virtual desktops more efficiently, reducing the need for extensive physical infrastructure. This shift has been instrumental in enabling the scalability of virtual desktop infrastructure (VDI) and Desktop as a Service (DaaS) solutions. The flexibility offered by cloud desktops allows organizations to manage resources dynamically, which is particularly advantageous in multi-cloud environments where workload distribution and disaster recovery are critical.

- Enhanced Accessibility and Cost Efficiency: Cloud computing facilitates greater accessibility and cost efficiency, enabling organizations to support remote desktop solutions and application virtualization without significant upfront investment. With the proliferation of virtual machines (VMs), businesses can provide employees with secure and consistent access to virtual workspaces, regardless of location. This capability is essential in today's work-from-anywhere culture, where mobility and data security are top priorities. Moreover, cloud desktops allow for more straightforward management and updates, which reduces the total cost of ownership (TCO) compared to traditional desktop setups.

Automation in Retail Boosting Virtualization Demand

Key Highlights

- Streamlining Retail Operations: The growth in automation within the retail sector is significantly contributing to the demand for desktop virtualization. Retailers are increasingly adopting automation technologies to streamline operations, enhance customer experience, and improve supply chain efficiency. Desktop virtualization supports these efforts by providing a centralized platform for managing applications, inventory systems, and customer data across multiple locations. By implementing remote desktop solutions, retailers can ensure that their operations are synchronized, with real-time data access and processing capabilities that are critical in a fast-paced environment.

- Supporting Omnichannel Strategies: As retailers continue to develop omnichannel strategies, the need for seamless integration across physical and digital platforms becomes more pronounced. Desktop virtualization enables retailers to create a unified workspace that supports various functions, from point-of-sale (POS) systems to customer relationship management (CRM) tools. This integration is vital for delivering a consistent customer experience across channels. Additionally, with the rise of virtual desktop deployment, retailers can maintain robust security protocols and data protection measures, which are essential in handling sensitive customer information.

Retail Desktop Virtualization Market Trends

The Rise of Cloud Deployment in Desktop Virtualization

- Cloud Deployment Trends: Cloud deployment has become a pivotal trend in the desktop virtualization market, driven by the need for cost-effective, scalable, and easily managed solutions. Businesses are increasingly transitioning from traditional on-premise setups to cloud-based models, with Virtual Desktop Infrastructure (VDI) and Desktop as a Service (DaaS) leading the way. This shift allows companies to deploy virtual desktops swiftly while reducing upfront costs and enhancing flexibility. The adoption of multi-cloud environments is further accelerating this trend, as businesses seek to avoid vendor lock-in and enhance operational resilience, driving the proliferation of virtual machines (VMs) across various cloud platforms.

- Key Factors Boosting Cloud Deployment: The widespread adoption of cloud computing is transforming the desktop virtualization landscape, offering organizations the ability to manage resources more efficiently. The growing preference for cloud deployment is due to the seamless integration of computing, storage, and networking resources provided by hyper-converged infrastructure (HCI). Additionally, the rise of Software-Defined Data Centers (SDDCs) is making it easier for enterprises to manage virtualized workloads, significantly improving operational efficiency. As a result, small to medium-sized enterprises (SMEs) are increasingly embracing cloud desktop solutions to optimize their IT resources, further driving market growth.

North America is Expected to Hold Major Share

- North America Leading the Global Market: North America is set to dominate the desktop virtualization market, driven by its advanced technological infrastructure and high adoption rates of digital transformation strategies. The region's strong focus on innovation and its ability to rapidly integrate new technologies have positioned it as a critical hub for market growth. The increasing demand for remote desktop solutions, fueled by the rise in remote work and telecommuting, is a key factor supporting this dominance. As businesses across the region adopt VDI, DaaS, and cloud desktop solutions, North America's market share is expected to grow significantly.

- United States as a Key Player: The United States, as the largest consumer of desktop virtualization in North America, plays a crucial role in the region's market leadership. The presence of major cloud service providers and an increasing number of hosted servers in the U.S. are driving the growth of cloud-based desktop virtualization. Additionally, the proximity to Canada and the emphasis on eco-friendly practices in new workspaces are further bolstering the market's expansion across the region. This regional interconnectivity supports the broader adoption of desktop virtualization solutions, reinforcing North America's leadership position.

Retail Desktop Virtualization Industry Overview

Highly Fragmented Market: The desktop virtualization market is highly fragmented, with no single company holding a dominant market share. This fragmentation indicates a competitive environment where both large global corporations and smaller specialized companies operate. The market's nature reflects the diversity of end-user needs, with players offering a wide range of solutions from basic virtualization to complex, customized deployments.

Market Leaders with Diverse Approaches: The leading players in the desktop virtualization market include Citrix Systems Inc., Toshiba Corporation, Red Hat Inc. (IBM Corporation), Huawei Technologies Co. Ltd., and Microsoft Corporation. These companies are distinguished by their strong global presence, extensive product portfolios, and continuous innovation. Citrix and Microsoft are particularly noted for their comprehensive virtualization platforms, while Red Hat (under IBM) and Huawei focus on integrating open-source and cloud-based solutions. Toshiba's presence is more niche, catering to specific industry needs.

Future Success Strategies Revolve Around Innovation and Integration: Key trends in the desktop virtualization market include the growing demand for cloud-based solutions, security enhancements, and seamless integration with existing IT infrastructures. For market players to succeed, they must focus on these areas, providing flexible and secure solutions that can adapt to the changing needs of businesses. Continuous innovation, strategic partnerships, and expanding service offerings will be crucial strategies for staying competitive in this fragmented market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview ( Includes the Impact due to COVID-19)

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Cloud Computing

- 5.1.2 Growth in Automation in Retail

- 5.2 Market Restraints

- 5.2.1 Infrastructure Deployment Constraints

6 MARKET SEGMENTATION

- 6.1 By Desktop delivery platform

- 6.1.1 Hosted Virtual Desktop (HVD)

- 6.1.2 Hosted Shared Desktop (HSD)

- 6.2 By Deployment Mode

- 6.2.1 On-premise

- 6.2.2 Cloud

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Citrix Systems Inc.

- 7.1.2 Toshiba Corporation

- 7.1.3 Red Hat Inc. (IBM Corporation )

- 7.1.4 Huawei Technologies Co. Ltd.

- 7.1.5 Microsoft Corporation

- 7.1.6 Parallels International GmbH

- 7.1.7 Dell Inc.

- 7.1.8 Ncomputing, Inc.

- 7.1.9 Ericom Software Inc.

- 7.1.10 Tems, Inc

- 7.1.11 Vmware Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日