|

市場調査レポート

商品コード

1629783

製造業におけるデスクトップ仮想化- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Desktop Virtualization In Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 製造業におけるデスクトップ仮想化- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

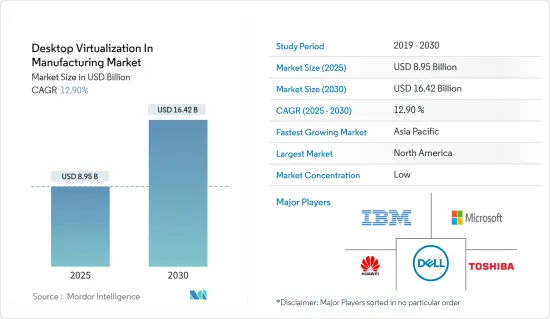

製造業におけるデスクトップ仮想化市場規模は、2025年に89億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは12.9%で、2030年には164億2,000万米ドルに達すると予測されます。

製造業におけるデスクトップ仮想化は、物理的なインフラ要件(スペース、消費電力、冷却など)やハードウェアの取得(新しいサーバーの購入)によって高いコストが発生することが多い大規模データセンターを持つ企業に対して、より効率的でコスト効率の高いソリューションを提供する成長市場です。

主要ハイライト

- クラウドコンピューティングの普及が市場を牽引。クラウドコンピューティングは企業のデジタルトランスフォーメーションを推進し、メーカーは情報技術(IT)予算をクラウドにシフトしています。クラウドコンピューティングは、産業部門における電力コストやリソース管理コストを削減し、デスクトップ仮想化の需要を促進しています。

- コスト削減が市場を牽引しているのは、情報技術(IT)の観点から、仮想デスクトップが新しいデスクトップを提供するのにかかる時間や、デスクトップや管理者の管理サポート費用を最小化するのに役立ち、異なる工場に投資しないためです。専門家によると、標準的なPCの総所有コスト(TCO)は、PCのハードウェアとソフトウェアの管理・保守に関連して50~70%だといいます。

- しかし、ネットワークインフラは、デスクトップ仮想化によって増加する帯域幅を管理しなければならないため、インフラの制約によって導入が制限されます。そうでなければ、更新が必要になります。広域ネットワーク(WAN)回線は、リモートDVコンシューマーを処理できなければならず、市場の重大な問題を防ぐことができます。

- COVID-19の大流行中、世界のデスクトップ仮想化市場は堅調に成長しました。これは、COVID-19が引き起こしたロックダウンや厳しい社会的距離施策により、デジタル普及率が劇的に高まったためで、デスクトップ仮想化ツールのようなリモート運用ツールの需要が高まった。Anunta Techの最新レポートによると、COVID-19の流行はデスクトップ仮想化産業に影響を与え、仮想デスクトップインフラ(VDI)の需要を70%以上増加させました。

- さらに、COVID-19のインスタンス数の増加により、多くの企業がリモートワーク技術を利用するようになりました。TechTargetのレポートによると、COVID-19の出現を受けて在宅勤務施策を導入した企業の67%以上が、パンデミック後も従業員がアクセス可能なリモートワークの選択肢を維持すると予想しています。この期間、このような要因が世界のデスクトップ仮想化ソリューション市場の拡大に拍車をかけた。

製造業におけるデスクトップ仮想化市場の動向

クラウド展開モードが大きなシェアを獲得

- 製造業における自動化/インテリジェント製造費用の削減と導入の迅速化におけるクラウドの重要性が、仮想デスクトップインフラ(VDI)の魅力となっています。製造業者は設計情報をデータセンターで管理し、リモートユーザーはノートパソコンやモバイルデバイスでこのデータをリアルタイムで見ることができます。

- クラウドソリューションにおける「リモート・デスクトップ仮想化」の利用は、フラッシュ・ストレージと加速された読み書きの機能により、製造業におけるユーザーエクスペリエンスを向上させ、従来のデスクトップ管理に比べて他の製造工場の管理コストを削減することができるため、増加していました。

- マイクロン技術社は、情報技術(IT)の仮想化を利用して、半導体メモリーの製造プロセスを管理しています。さらに、同社は製造工場で仮想化/ハイパーコンバージドインフラ(HCI)エコシステムの基本部分を開発、製造、保守しており、これが市場を効率的に押し上げています。

著しい成長を遂げる北米

- 北米は、産業部門が米国経済の大半を占め、同地域の経済生産高の82%を占めており、多数のクラウドサービスプロバイダーがデスクトップ仮想化の高い需要をもたらしています。

- この地域では、製造業における3Dプリンティングの導入が著しく、産業や学術機関が絶えず3Dプリンティングを導入しています。米国におけるNVIDIA仮想化プラットフォームは、NVIDIA GPUの可能性を広げ、3Dアプリケーションでネイティブなデスクトップ体験を記載しています。

- 米国は世界最大の医薬品市場であり、医薬品とバイオテクノロジー産業における研究開発費の半分以上を占めています。数多くの制御システムが存在するため、各システムにはネットワーク・トポロジー、サーバーインフラ、工場フロア上のワークステーションが必要であり、デスクトップ仮想化が普及しています。

- 自動化への急速な動向や、エコや省エネの実践による新技術への投資は、産業セグメントでの価値創造を後押ししており、今後の需要拡大が期待されます。

製造業におけるデスクトップ仮想化産業概要

製造業におけるデスクトップ仮想化市場は、参入企業が製造部門の生産性を向上させるために研究開発で新技術を革新し投資しているためセグメント化されており、参入企業間の競争は激しいです。主要参入企業は、IBM、Microsoft Corporation、Huawei Technologiesなどです。市場の最近の動向は以下の通り。

2022年2月、IBMはハイブリッド・マルチクラウドサービスの提供を拡大し、ハイブリッド・クラウドと人工知能(AI)戦略で発言力を持つため、Microsoft Azureのコンサルタント会社であるNeudesicを買収しました。

2022年5月、Citrixは、世界初のクラウドPCであるWindows365と、市場をリードする高解像度ユーザー体験(HDX)技術、堅牢なIT施策制御、エコシステムの柔軟性を組み合わせた次期製品について、Microsoftと協業したと発表しました。これにより、IT管理者はシトリックスのユーザーライセンシングに容易にアクセスできるようになり、従業員はMicrosoft Endpoint ManagerとWindows 365を通じてシトリックスクライアントにシームレスに移行できるようになりました。

2022年5月、Citrix DaaS for IBM Cloudは、Intel Xeonサーバーを搭載したIBM Cloud Virtual Private Cloud(VPC)で利用可能になりました。オートスケールにより、この機能はクラウドでのパートタイムワークロードの可能性を広げ、数分での迅速なマシンプロビジョニングを実現し、アプリやデスクトップコンピュータを動的に展開します。

さらに、オンプレミスで仮想デスクトップインフラ(VDI)を実行している既存のシトリックスクライアントは、VPCに移行またはバーストし、DaaS(Desktop-as-a-Service)の提供を開始することができます。管理者は、マシンカタログを使用して任意の仮想プライベートクラウド(VPC)インスタンスプロファイルを選択し、永続的または非永続的なデスクトップとアプリケーション体験を提供できます。

2022年11月、NComputingは、最新のRaspberry Pi 3(PIシリーズの開発ボード)をベースとした、クラウド対応、デュアルスクリーン、Wi-Fi対応のWindowsとLinux用シンクライアント「RX300」を発表しました。受賞歴のあるNComputingのデスクトップ仮想化ソフトウェアvSpace Pro 10が、RX300の対象プラットフォームです。NComputingのvCASTストリーミング技術のサポートを含むクラウド対応機能とともに、高性能PCのような体験を記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提条件と市場定義

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因の採用

- 市場促進要因

- クラウドコンピューティングの採用拡大

- デスクトップ/PCのコスト削減

- 市場抑制要因

- インフラの制約

- バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- デスクトップ提供プラットフォーム別

- ホスト型仮想デスクトップ(HVD)

- ホスト型共有デスクトップ(HSD)

- その他のデスクトップ提供プラットフォーム

- 導入形態別

- オンプレミス

- クラウド

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- IBM Corp.

- Microsoft Corporation

- Huawei Technologies Co. Ltd.

- Dell Inc.

- Toshiba Corporation

- Citrix Systems, Inc.

- Parallels International GmbH

- NComputing Co. LTD.

- Ericom Software

- VMware, Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Desktop Virtualization In Manufacturing Market size is estimated at USD 8.95 billion in 2025, and is expected to reach USD 16.42 billion by 2030, at a CAGR of 12.9% during the forecast period (2025-2030).

Desktop virtualization in manufacturing is a growing market that provides more efficient and cost-effective solutions for enterprises with large data centers, which often incur high costs due to physical infrastructure requirements (such as space, power consumption, and cooling) and hardware acquisition (purchase of new servers).

Key Highlights

- The increased popularity of cloud computing is driving the market. Cloud computing drives digital transformation in enterprises, and manufacturers are shifting their information technology (IT) budgets to the cloud. It lowers power and resource management costs in the industrial sector, driving demand for desktop virtualization.

- Cost savings are driving the market because, from an information technology (IT) standpoint, virtual desktops assist in minimizing the time it takes to provide new desktops, as well as desktop and admin administration and support expenses, by not investing in different plants. According to experts, the total cost of ownership (TCO) of a standard PC is between 50 and 70 percent related to managing and maintaining PC hardware and software.

- However, infrastructure restrictions limit the adoption since network infrastructure must manage the increased bandwidth that desktop virtualization will create. Otherwise, it will need to be updated. The Wide Area Network (WAN) lines must be able to handle remote DV consumers, preventing a significant market problem.

- During the COVID-19 pandemic, the global desktop virtualization market grew steadily, owing to dramatically increased digital penetration during COVID-19-induced lockdowns and stringent social distancing policies, which fueled demand for remote operational tools such as desktop virtualization tools. According to Anunta Tech's recent report, the COVID-19 pandemic affected the desktop virtualization industry, increasing demand for virtual desktop infrastructure (VDI) by more than 70%.

- Furthermore, the growing number of COVID-19 instances prompted many firms to use remote working technologies. According to a TechTarget report, more than 67% of firms who implemented work-from-home policies following the emergence of COVID-19 expected to maintain remote working alternatives accessible for their employees even after the pandemic. During this period, such factors fueled the expansion of the worldwide desktop virtualization solutions market.

Desktop Virtualization in Manufacturing Market Trends

Cloud Deployment Mode to Gain Significant Share

- The importance of the cloud in reducing automation/intelligent manufacturing expenses and speeding up adoption in the manufacturing industry has been a draw for Virtual desktop infrastructure (VDI). Manufacturers can maintain design information in the data center, and remote users can view this data in real-time on a laptop or mobile device.

- The use of remote desktop virtualization' in cloud solutions was growing as a result of their flash storage and accelerated reading and writing features, which improve the user experience in the manufacturing sector and lower the cost of managing other manufacturing plants when compared to traditional desktop administration.

- Micron Technology manages its semiconductor memory production processes using virtualization in information technology (IT). In addition, they develop, produce, and maintain fundamental pieces of the virtualization/hyper-converged infrastructure (HCI) ecosystem in their manufacturing plant, which efficiently pushes the market.

North America to Witness Significant Growth

- North America controls most of the market since the industrial sector dominates the United States economy, which accounts for 82% of the region's economic output, and a substantial number of cloud service providers, resulting in high demand for desktop virtualization.

- The region's adoption of 3D printing for manufacturing has been significant, with industry and academic institutions deploying 3D printing constantly. NVIDIA virtualization platform in the United States extends the potential of NVIDIA GPUs, delivering a native desktop experience in 3D applications.

- The United States is the world's largest drug market, accounting for over half of all R&D spending in the pharmaceutical and biotechnology industry. With numerous control systems, each system needs its network topology, server infrastructure, and workstations on the plant floor, where desktop virtualization is becoming more popular.

- The rapid trend toward automation and investments in new technologies through implementing eco-friendly and energy-saving practices are driving value creation in the industrial sector, which will enhance demand in the future.

Desktop Virtualization in Manufacturing Industry Overview

The desktop virtualization market in manufacturing is fragmented as the players are innovating and investing in new technologies in R&D to improve the manufacturing sector's productivity, which gives a high rivalry among the players. Key players are IBM, Microsoft Corporation, Huawei Technologies Co. Ltd, etc. Recent developments in the market are -

In February 2022, IBM purchased Neudesic, a Microsoft Azure consultancy, to expand its provision of hybrid multi-cloud services and have a say in its hybrid cloud and artificial intelligence (AI) strategies.

In May 2022, Citrix announced that it collaborated with Microsoft on an upcoming product combining Windows 365, the world's first cloud PC, with its market-leading high-definition user experience (HDX) technology, robust IT policy control, and ecosystem flexibility. This gave IT administrators easier access to Citrix user licensing and offered employees a seamless transition to Citrix clients through Microsoft Endpoint Manager and Windows 365.

In May 2022, Citrix DaaS for IBM Cloud was available on IBM Cloud Virtual Private Cloud (VPCs) powered by Intel Xeon servers. With autoscale, this feature opened up the potential for part-time workloads in the cloud, delivering quick machine provisioning in minutes and dynamically deploying apps and desktop computers.

Furthermore, existing Citrix clients who run virtual desktop infrastructure (VDI) on-premises can migrate or burst to VPC and start providing Desktop-as-a-Service (DaaS). Administrators can use a machine catalog to select any Virtual Private Cloud (VPC) instance profile to deliver persistent and non-persistent desktop and application experiences.

In November 2022, A cloud-ready, dual-screen, Wi-Fi-ready thin client for Windows and Linux called RX300 was launched by NComputing Co. LTD. and is based on the most recent Raspberry Pi 3 (development board in PI series). The award-winning vSpace Pro 10 desktop virtualization software from NComputing is the platform for which RX300 is intended. Along with cloud-ready features, including support for NComputing's vCAST streaming technology, it offers a high-performance PC-like experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions and Market Definition

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Growing Adoption of Cloud Computing

- 4.3.2 Cost Saving in Desktop/PC

- 4.4 Market Restraints

- 4.4.1 Infrastructural Constraints

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Desktop Delivery Platform

- 5.1.1 Hosted Virtual Desktop (HVD)

- 5.1.2 Hosted Shared Desktop (HSD)

- 5.1.3 Other Desktop Delivery Platforms

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corp.

- 6.1.2 Microsoft Corporation

- 6.1.3 Huawei Technologies Co. Ltd.

- 6.1.4 Dell Inc.

- 6.1.5 Toshiba Corporation

- 6.1.6 Citrix Systems, Inc.

- 6.1.7 Parallels International GmbH

- 6.1.8 NComputing Co. LTD.

- 6.1.9 Ericom Software

- 6.1.10 VMware, Inc.