|

市場調査レポート

商品コード

1640499

アジア太平洋の油田用化学品-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Asia-Pacific Oilfield Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の油田用化学品-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

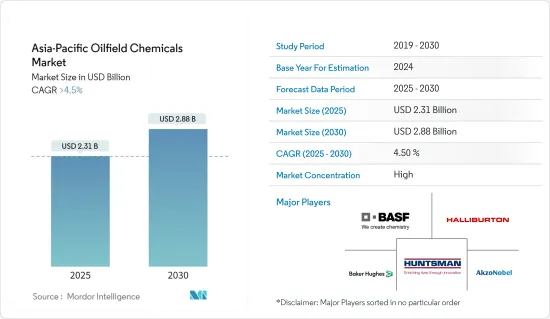

アジア太平洋の油田用化学品市場規模は、2025年に23億1,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは4.5%を超え、2030年には28億8,000万米ドルに達すると予測されます。

COVID-19の大流行は石油・ガス産業に悪影響を及ぼし、アジア太平洋の油田用化学品市場にも影響を与えました。しかし、COVID-19以後は、石油・ガス産業からの需要が増加しており、同地域の油田用化学品市場は復活すると予想されます。

主要ハイライト

- 市場の成長を促す主要要因のひとつは、アジア太平洋におけるガス探査・生産のシェア拡大です。輸送産業における石油系燃料の需要増が、予測期間中の市場需要を牽引するとみられます。

- バイオ燃料産業の台頭は、市場成長の妨げになる可能性が高いです。持続可能性と環境問題への関心の高まりに伴い、油田用化学品産業は規制の圧力や投資家の関心の低下にも直面する可能性があります。

- シェールオイル・ガスのような深海資源や非在来型資源への注目の高まりは、掘削油剤、潤滑油、コンプリーション油剤の新市場を切り開きます。このような厳しい環境に対応する高性能で環境に優しい化学品の開発は、大きなビジネス機会です。

- アジア太平洋全体では中国が市場を独占しており、同地域での油田用化学品の消費が最も大きいです。

アジア太平洋の油田用化学品の市場動向

腐食・スケール抑制剤セグメントが市場を独占

- 腐食防止剤は油井の金属パイプの腐食を抑えるために使用されます。炭素鋼パイプや容器には、腐食抑制が好ましい治療法です。阻害剤の利点は、プロセスが継続している場合でもほとんどのケースで使用できることです。

- 腐食は、酸素が金属部分と反応して酸化物を形成することで発生します。腐食防止剤は、露出した部品の上に薄いバリア層を形成することで作用します。油田では、数種類の腐食防止剤が使用されています。

- デハ-ジエチルヒドロキシルアミン、ポリアミン、モルホリン、シクロヘキシルアミン、二酸化炭素腐食防止剤などです。フィルミングアミンの混合物は、復水ライン腐食防止剤の調製に使用されます。これは、高蒸気と低蒸気の両方の液体が存在するため、すべての段階を保護することができます。

- スケールは、温度が上昇するにつれて不溶性になる可溶性固体が析出する結果、油田設備の表面に形成される残留物です。これが金属腐食を引き起こし、機器の機能とメンテナンスに影響を与えます。この析出は腐食速度を高め、生産損失を引き起こし、流れを制限します。

- したがって、油田設備を保護し、その効率を維持するためには、スケール防止剤として機能する科学的に設計された化学品を添加して、正確な状態を維持する必要があります。有機リン酸塩、無機リン酸塩、ポリマー(ポリアクリル酸塩)、ホスホン酸塩、有機キレート剤であるエチレンジアミン四酢酸(EDTA)などの化学品が、スケール防止剤の一部です。腐食防止剤は、油井の金属パイプの腐食を抑えるために使用されます。炭素鋼のパイプや容器では、腐食抑制が望ましい治療法です。

- Rystadによると、オフショアプロジェクトがグリーンフィールド投資の回復を促進し、石油・ガス産業における海底インフラと掘削サービスの需要が大きくなるといいます。

- 例えば、Petronasのカサワリはマレーシア初の炭素回収・貯留(CCS)の投資承認を発表し、これに続いてタイのPTT Exploration and Productions(PTTEP)のLang Lebahがマレーシアで2023年のFIDを目指しています。

- エネルギー産業協議会によると、シェルは最近、グムスット・カカプ・ゲロン・ジャグス・イースト(GKGJE)深海プロジェクト(2024年稼働予定の海底タイバック開発)への投資を承認しました。

- S&P Global Inc.によると、ニュージーランドのRefining NZは、2022年前半にマースデン・ポイント製油所を輸入ターミナルに転換できるよう、10月中に顧客とのターミナルサービス契約をまとめる予定だといいます。

- S&P世界社によると、オーストラリアのViva Energyは、連邦政府による燃料安全保障包装の発表を歓迎し、その一環として、2027年6月までジーロングでの精製操業を維持し、さらに3年間のオプションで2030年6月まで延長することを6年間約束するとしています。

- タイのシラチャ製油所では、40億米ドルのクリーン燃料プロジェクトが進められています。このアップグレードは2023年に完了する予定で、製油所の生産能力を27万5,000b/dから40万b/dに増強し、よりクリーンな製品の生産性を高めています。

- さらに、アジア太平洋におけるメンテナンスの新規契約は、予測期間中に腐食・スケール防止剤への投資の増加を示しています。

市場を独占する中国

- 石油・ガス産業は中国経済の主要な貢献者のひとつです。石油・ガス産業は高温環境で操業しています。

- 油田用化学品は、掘削、生産、刺激、増進回収活動で使用されます。シェール層からの石油・ガス埋蔵量の開発には、水圧掘削などの活動が必要であり、油田用化学品の使用を奨励しています。中国は、シェールガス探査の能力と掘削技術において多くのマイルストーンを達成してきました。そのため、世界でもトップクラスのシェールガス供給国となっています。

- BP Statistical Review 2023によると、2022年の同国全体の石油生産量は2億470万トンに達し、2021年の生産量1億9,890万トンと比べて2.9%の成長率でした。

- 同様に、同国の石油消費量全体も過去10年間で増加傾向にあります。例えば、2022年の同国の石油消費量(1,000バレル/日)は1,429万5,000バレル/日であったのに対し、2021年には1,489万3,000バレル/日でした。また、2012年から22年までの10年間で、消費量の伸び率は年率3.6%でした。

- さらに、同じ情報源は、同国が天然ガス生産でプラス成長を確認したことを挙げています。例えば、2021年の天然ガス生産量は2,092億立方メートルであったが、2022年には2,218億立方メートルに増加し、これは約6.0%の成長です。また、この10年間で、生産量は年平均7.1%増加しています。

- 同国における石油・ガスの生産能力の増加は、同国の油田用化学品市場を牽引すると考えられます。

アジア太平洋の油田用化学品産業概要

アジア太平洋の油田用化学品市場は、その性質上、部分的に統合されています。主要企業(順不同)には、AkzoNobel N.V.、Haliburton、Huntsman International LLC、Baker Hughes Company、BASF SEなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 運輸産業における石油系燃料の需要増加

- アジア太平洋におけるシェールガス探査・生産の増加

- その他の促進要因

- 抑制要因

- バイオ燃料産業の台頭

- クリーンエネルギーへの取り組み

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 化学タイプ

- 殺生物剤

- 腐食・スケール防止剤

- 乳化剤

- ポリマー

- 界面活性剤

- その他の化学品(有機酸、フラクチャリング液など)

- 用途

- 掘削とセメンテーション

- 石油増進回収

- 生産

- 坑井刺激

- ワーカオーバーとコンプリーション

- 地域

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- フィリピン

- オーストラリア・ニュージーランド

- その他のアジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AkzoNobel N.V.

- Albemarle Corporation

- Ashland

- Baker Hughes Company

- BASF SE

- CLARIANT

- Chevron Phillips Chemical Company LLC

- Dow

- Ecolab

- Elementis PLC

- Haliburton

- Huntsman International LLC

- Innospec

- Kemira

- Newpark Resources Inc.

- SLB

- Solvay

第7章 市場機会と今後の動向

- 深海掘削事業が切り開く新たな地平

- 新興諸国がもたらす生産機会

The Asia-Pacific Oilfield Chemicals Market size is estimated at USD 2.31 billion in 2025, and is expected to reach USD 2.88 billion by 2030, at a CAGR of greater than 4.5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the oil and gas industry, which in turn affected the oilfield chemicals market in the Asia-Pacific region. However, post-COVID-19, the rising demand from the oil and gas industry is expected to revive the market for oilfield chemicals in the region.

Key Highlights

- One of the major factors driving the market's growth is the increased share of gas exploration and production in the Asia-Pacific region. Rising demand for petroleum-based fuel from the transportation industry is expected to drive the market demand during the forecast period.

- The rising biofuel industry is likely to hinder the market growth. With the increasing focus on sustainability and environmental concerns, the oilfield chemicals industry may face regulatory pressures and a decline in investor interest as well.

- The increasing focus on deepwater and unconventional resources like shale oil and gas opens up new markets for drilling fluids, lubricants, and completion fluids. Developing high-performance, environmentally friendly chemicals for these challenging environments is a lucrative opportunity.

- China dominated the market across the Asia-Pacific Region, with the most significant consumption of oilfield chemicals in this region.

Asia-Pacific Oilfield Chemicals Market Trends

Corrosion and Scale Inhibitors segment to dominate the market

- Corrosion inhibitors are used to reduce corrosion in the metallic pipes of the oil well. Inhibition is the preferred treatment for carbon steel pipes and vessels. The advantage of inhibition is that it can be used in most cases even when the process is continuing.

- Corrosion occurs due to the reaction of oxygen with metallic parts to form oxides. Corrosion inhibitors act by forming a thin barrier layer over the exposed parts. Several types of corrosion inhibitors are used in oilfields.

- These include Deha - Diethyl Hydroxyl Amine, Polyamine, Morpholine, Cyclohexylamine, and Carbon Dioxide Corrosion Inhibitors. A mixture of filming amines is used to prepare condensate line corrosion inhibitors. This can protect every stage due to the presence of both high and low vapor/liquids.

- Scale is a residue that forms on the surface of oilfield equipment as a result of the precipitation of soluble solids that become insoluble as temperature increases. This, in turn, causes metallic corrosion that affects the functioning and maintenance of equipment. This deposition increases corrosion rates, causes loss of production, and restricts flow.

- Hence, to safeguard oilfield equipment and to maintain their efficiency, it is necessary to maintain accurate conditions by adding scientifically designed chemicals that act as scale inhibitors. Chemicals, such as organic phosphates, inorganic phosphates, polymers (polyacrylates), phosphonates, and ethylenediaminetetraacetic acid (EDTA), an organic chelating agent, are some of the scaling inhibitors. Corrosion inhibitors are used to reduce corrosion in metallic pipes of oil wells. Inhibition is the preferred treatment for carbon steel pipes and vessels.

- As per Rystad, offshore projects will drive the recovery in greenfield investment, with significant demand for subsea infrastructure and drilling services in the oil and gas industry.

- For example, Petronas's Kasawari announced investment approval for the first carbon capture and storage (CCS) in Malaysia, which was followed by Thai company PTT Exploration and Productions's (PTTEP's) Lang Lebah, targeting FID in 2023 in Malaysia.

- Shell's recent investment approval for the Gumusut-Kakap-Geronggong-Jagus East (GKGJE) deep-water project - a subsea tieback development planned to start up in 2024, according to the Energy Industries Council.

- As per S&P Global Inc., New Zealand's Refining NZ said it was working to finalize terminal services agreements with customers in October to enable the conversion of its Marsden Point refinery into an import terminal in the first half of 2022.

- As per S&P Global Inc, Australia's Viva Energy welcomed the federal government's announcement of a fuel security package and, as part of this, would make a six-year commitment to maintain refining operations at Geelong through to June 2027 with a further three-year option to extend until June 2030.

- A USD 4 billion clean fuel project is being undertaken at Thailand's Sriracha refinery. The upgrade is slated to be completed in 2023 and will increase the refinery's capacity from 275,000 b/d to 400,000 b/d, boosting the yield of cleaner products. as per S&P Global Inc.

- Furthermore, new contracts for maintenance in Asia-Pacific exhibit increased investment in corrosion and scale inhibitors during the forecast period.

China to Dominate the Market

- The oil and gas industry is one of the key contributors to the Chinese economy. The oil and gas industry operates in high-temperature environments.

- Oilfield chemicals are used in drilling, production, stimulation, and enhanced oil recovery activities. Developing oil and gas reserves from shale formations requires activities such as hydraulic drilling, which encourages the use of oilfield chemicals. China has achieved many milestones in capacity and drilling techniques in shale gas exploration. This makes it one of the top shale gas suppliers around the globe.

- According to BP Statistical Review 2023, the overall oil production in the country reached 204.7 million metric tons in 2022 at a growth rate of 2.9% compared to 198.9 million metric tons produced in 2021.

- Similarly, the country's overall oil consumption has been on the rise over the past decade. For instance, in 2022, the country's oil consumption in thousands of barrels per day was 14,295 thousand barrels per day, whereas in 2021, the consumption stood at 14,893 thousand barrels per day. In addition, the consumption growth rate has been 3.6% yearly over the decade between 2012 and 22.

- Moreover, the same source cited that the country witnessed positive growth in natural gas production. For instance, in 2021, the natural gas produced was 209.2 billion cubic meters, whereas in 2022, the production increased to 221.8 billion cubic meters, which is around 6.0% growth. In addition, over the decade, production has been growing by an average of 7.1% yearly.

- The increase in the production capacities of oil and gas in the country is likely to drive the market for oilfield chemicals in the country.

Asia-Pacific Oilfield Chemicals Industry Overview

The Asia-Pacific oilfield chemicals market is partially consolidated in nature. The major players (not in a particular order) include AkzoNobel N.V., Haliburton, Huntsman International LLC, Baker Hughes Company, and BASF SE, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for Petroleum-based Fuel from the Transportation Industry

- 4.1.2 Increased Shale Gas Exploration and Production in Asia-Pacific

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Rising Biofuel Industry

- 4.2.2 Clean Energy Initiatives

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Chemical Type

- 5.1.1 Biocide

- 5.1.2 Corrosion and Scale Inhibitor

- 5.1.3 Demulsifier

- 5.1.4 Polymer

- 5.1.5 Surfactant

- 5.1.6 Other Chemical Types (Organic Acids, Fracturing Fluids, etc.)

- 5.2 Application

- 5.2.1 Drilling and Cementing

- 5.2.2 Enhanced Oil Recovery

- 5.2.3 Production

- 5.2.4 Well Stimulation

- 5.2.5 Workover and Completion

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Malaysia

- 5.3.6 Thailand

- 5.3.7 Indonesia

- 5.3.8 Vietnam

- 5.3.9 Philippines

- 5.3.10 Australia & New Zealand

- 5.3.11 Rest of Asia-pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Albemarle Corporation

- 6.4.3 Ashland

- 6.4.4 Baker Hughes Company

- 6.4.5 BASF SE

- 6.4.6 CLARIANT

- 6.4.7 Chevron Phillips Chemical Company LLC

- 6.4.8 Dow

- 6.4.9 Ecolab

- 6.4.10 Elementis PLC

- 6.4.11 Haliburton

- 6.4.12 Huntsman International LLC

- 6.4.13 Innospec

- 6.4.14 Kemira

- 6.4.15 Newpark Resources Inc.

- 6.4.16 SLB

- 6.4.17 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Horizons Opened Up due to Deep-water Drilling Operations

- 7.2 Production Opportunities Provided by Developing Countries