|

市場調査レポート

商品コード

1640443

難燃ファブリック:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Fire-resistant Fabrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 難燃ファブリック:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

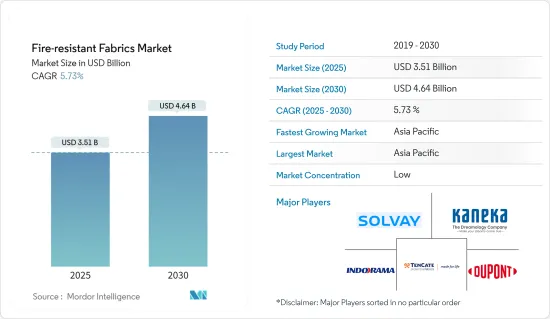

難燃ファブリック市場規模は2025年に35億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.73%で、2030年には46億4,000万米ドルに達すると予測されます。

市場はCOVID-19の大流行によりマイナスの影響を受けました。このパンデミックのために、ウイルスの蔓延を抑えるために世界のいくつかの国が封鎖状態に入った。これにより需給チェーンが完全に混乱し、市場に悪影響を及ぼしました。COVID-19パンデミックから市場は回復し、著しい成長を遂げています。

主なハイライト

- 短期的には、生地に対する厳しい工業規格、家庭用および商業用家具における難燃ファブリックの需要増加、南米の鉱業からの需要増加が市場の成長を牽引しています。

- その反面、難燃ファブリックの製造に使用される原材料の価格が高く、安全規格が整備されていないことが市場成長の妨げになると予想されます。

- とはいえ、BRICS諸国(ブラジル、ロシア、インド、中国、南アフリカ)における急速な工業化は、予測期間中に好機となることが予想されます。

- アジア太平洋地域は、中国やインドなどの国々からの消費の増加により、予測期間中に最大のシェアを占めると予想されます。

難燃ファブリック市場動向

輸送セグメントが市場を独占する

- 耐火性繊維は、鉄道、自動車、航空機、海洋建設などの輸送産業で使用されています。世界の輸送部門は、より良い鉄道、地下鉄、鉄道網を建設するための外国投資に対応して健全に成長することが期待されています。

- OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、世界の自動車産業は自動車と商用車の生産台数の増加を目の当たりにし、2022年には8,484万台、2023年には9,355万台に達します。このため、2022年と2023年には、この分野からの難燃ファブリックの需要が増加しました。

- 世界の主要市場である米国、ブラジル、インド、中国における2022年の自動車販売台数は、前年比でそれぞれ10%、5%、24%、3%増加しました。

- しかし、さまざまな環境問題への懸念から化石燃料からの脱却を推進する政府プログラムにより、特に欧州と中国では電気自動車の開発が今後も勢いを増すと予想され、あらゆる自動車分野の設計者が新たな可能性を見出しています。

- 自動車分野では、インドのようなアジア太平洋諸国での電気自動車需要の高まりも市場の成長を後押ししています。

- IEA(国際エネルギー協会)によると、2030年の世界の電気自動車販売台数は、新政策シナリオ(二輪車/三輪車を除く)で1億2,500万台に達すると予想されています。EV30@30シナリオでは、2030年、中国では自動車販売の約70%がEVになると予想されています。欧州では販売台数の半分がEVで、日本は37%、インドは29%、カナダと米国は30%です。

- 世界の鉄道建設の拡大が難燃ファブリックの需要を牽引すると予想されます。インド政府は、インドの30以上の都市で地下鉄鉄道プロジェクトの開発を計画しています。

- 航空業界もまた、顕著な成長を遂げている人気の交通手段です。航空機は、遠方への最速の通勤手段として知られています。航空機の製造において、適切な生地素材を選択することは、他の部品と同様に重要です。航空機事故による死者のかなりの割合は、火災や煙の吸引、火災時に放出される有毒ガスによる窒息が原因です。

- 旅客数の増加と航空機の退役の増加により、今後20年間は新型ジェット機のニーズが高まると予想されます。ボーイング商用機市場見通し2023-2042によると、2023-2042年の間に42,000機の航空機が新たに納入される見込みです。

- ボーイングによると、民間航空機の市場規模は2028年までに3兆1,000億米ドルに達すると予想されています。新興市場および既存市場における航空旅行の着実な増加に対応するため、運航会社は古いジェット機をより燃費の良いモデルに置き換え、保有機を拡大すると予想されているからです。したがって、新しいジェット機の生産に伴い、航空宇宙産業からの耐火性ファブリックの需要も予測期間中に増加すると予想されます。

- 上記のすべての要因が、予測期間中に難燃ファブリック市場を牽引すると予想されます。

アジア太平洋市場を独占する中国

- 中国における難燃ファブリックの需要を牽引しているのは、主に航空宇宙産業における製造活動の拡大です。

- この成長は主に、消費者の消費力の高さと航空便の利便性向上による旅客輸送量の増加に依存しています。旅客輸送量の増加は、さらに航空機の旺盛な需要を生み出しています。

- 中国の航空宇宙政策は、航空宇宙開発と生産のトップレベルに入るための最も包括的な試みのひとつです。中国は、今後20年間で、民間航空機販売において世界最大の単一国市場になると予想されています。メイド・イン・チャイナ2025」計画のもと、中国は2025年までに国産民間航空機の10%以上を国内市場に供給すると予想されています。これにより、予測期間中、航空宇宙分野の難燃ファブリック市場にビジネスチャンスがもたらされると予想されます。

- 自動車産業は難燃ファブリックの主要消費者のひとつです。中国は自動車の主要生産国であり、2022年の総生産台数は2,700万台を超え、前年比約3%の成長率を記録するため、難燃ファブリックの市場需要にプラスの影響を与えます。

- さらに、政府が電気自動車の生産に力を入れていることも、予測期間中の難燃ファブリック市場の需要を促進すると予想されます。

- 中国政府は、2025年までに少なくとも5,000台、2030年までに100万台の燃料電池電気自動車を導入する計画です。政府による電気自動車、ハイブリッド車、燃料電池車の普及促進は、予測期間中の市場調査を促進すると予想されます。

- 上記のすべての要因が、予測期間中に同国における難燃ファブリックの需要を促進すると予想されます。

難燃ファブリック産業の概要

難燃ファブリック市場は細分化されています。主要企業(順不同)には、デュポン、インドラマ・コーポレーション、ソルベイ、カネカコーポレーション、テンケート・プロテクティブ・ファブリックスなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- ファブリックに対する厳しい工業規格

- 家庭用および商業用家具における耐火性ファブリックの需要増加

- 南米における鉱業需要の増加

- 抑制要因

- 難燃ファブリックの原料価格の高騰

- 安全コンプライアンスの欠如

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ別

- アパレル

- 非アパレル

- 用途別

- 産業用防護服・鉱業用防護服

- 輸送

- 鉄道

- 航空機

- 自動車(道路)

- 海洋

- 防衛・消防

- その他の用途

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- マレーシア

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ロシア

- ノルディック

- トルコ

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- アラブ首長国連邦

- エジプト

- ナイジェリア

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- DuPont

- Glen Raven Inc.

- Indorama Corporation

- KANEKA CORPORATION

- LENZING AG

- Newtex Industries Inc.

- PBI Fibers International

- Solvay

- Teijin Carbon Europe GmbH

- TenCate Protective Fabrics

- W. L. Gore & Associates Inc.

- Westex:A Milliken Brand

第7章 市場機会と今後の動向

- BRICS諸国における急速な工業化

- その他の機会

The Fire-resistant Fabrics Market size is estimated at USD 3.51 billion in 2025, and is expected to reach USD 4.64 billion by 2030, at a CAGR of 5.73% during the forecast period (2025-2030).

The market was negatively impacted due to the COVID-19 pandemic. Owing to the pandemic, several countries worldwide went into lockdown to curb the spread of the virus. This completely disrupted the supply and demand chain, negatively affecting the market. The market has recovered from the COVID-19 pandemic and has grown at a significant rate.

Key Highlights

- Over the short term, stringent industrial standards for fabrics, the increasing demand for fire-resistant fabrics in home and commercial furnishing, and growing demand from the mining industry in South America are driving the market's growth.

- On the flip side, the high price of raw materials that are used to make fire-resistant fabric and the lack of safety compliances are expected to hinder the market's growth.

- Nevertheless, rapid industrialization in BRICS countries (Brazil, Russia, India, China, and South Africa) is expected to be an opportunity during the forecast period.

- Asia-Pacific is expected to account for the largest share during the forecast period, owing to increasing consumption from countries such as China and India.

Fire-resistant Fabrics Market Trends

Transport Segment to Dominate the Market

- Fire-resistant fabrics are used in the transport industry during railways, automotive, aircraft, and marine construction. The global transport sector is expected to grow healthy in response to foreign investments in constructing better railways, metro, and rail networks.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), the global automobile industry witnessed an increase in the production of cars and commercial vehicles, reaching 84.84 million units in 2022 and 93.55 million units in 2023. This, in turn, increased the demand for fire-resistant fabrics from this sector in 2022 and 2023.

- The car sales for 2022 in major global markets of the United States, Brazil, India, and China were up by 10%, 5%, 24%, and 3%, respectively, compared to the previous year.

- However, the development of electric vehicles is expected to continue to gain momentum in the future, especially in Europe and China, owing to government programs promoting the shift away from fossil fuels due to various environmental concerns, where designers in all the automotive segments are discovering new possibilities.

- In the automotive sector, the growing demand for electric vehicles in Asia-Pacific countries, like India, has also fueled the market's growth.

- According to the IEA (International Energy Association), in 2030, global electric vehicle sales are expected to reach 125 million as per the New Policies Scenario (excluding two/three-wheelers). In the EV30@30 Scenario, in 2030, in China, around 70% of vehicle sales are expected to be EVs. Half of the vehicles sold in Europe are EVs, with 37% in Japan, 29% in India, and 30% in Canada and the United States.

- Growing railway construction worldwide is expected to drive the demand for fire-resistant fabrics. The Indian government plans to develop metro rail projects in more than 30 Indian cities.

- The aviation industry is another popular mode of transportation that has been growing notably. It is known to be the fastest means of commuting to distant places. Selecting the right fabric material in aircraft production is as important as any other component. A substantial percentage of aircraft accident deaths are caused by fire and smoke inhalation and asphyxiation from toxic gases released during a fire.

- The growing passenger volumes and increasing aircraft retirements are expected to drive the need for new jets over the next two decades. According to Boeing Commercial Market Outlook 2023-2042, 42,000 new aircraft are expected to be delivered during 2023-2042.

- According to Boeing, the market value for commercial aircraft is expected to reach USD 3.1 trillion by 2028, as operators are expected to replace older jets with more fuel-efficient models and expand their fleets to cater to the steady rise in air travel in emerging and established markets. Hence, with the production of new jets, the demand for fire-resistant fabrics from the aerospace industry is also expected to increase during the forecast period.

- All the factors above are expected to drive the fire-resistant fabrics market during the forecast period.

China to Dominate the Asia-Pacific Market

- The growing manufacturing activities of the aerospace industry in the country mainly drive the demand for fire-resistant fabrics in China.

- This growth primarily depends on the rising passenger traffic due to the high consumer spending power and better air connectivity. The increasing passenger traffic is further creating a robust demand for aircraft.

- The Chinese aerospace policy represents one of the most comprehensive attempts to enter the top aerospace development and production levels. China is expected to be the world's largest single-country market for civil aircraft sales in the next 20 years. Under the plan 'Made in China 2025,' it is expected that China will supply over 10% of homemade commercial aircraft to the domestic market by 2025. This is expected to provide opportunities for the fire-resistant fabrics market in the aerospace sector during the forecast period.

- The automotive industry is one of the major consumers of fire-resistant fabrics. China is the leading producer of vehicles, with a total production volume of over 27 million vehicles in 2022, registering a growth rate of about 3% compared to the previous year, thus positively impacting the market demand for fire-resistant fabrics.

- Moreover, the government's focus on producing electric vehicles is expected to drive the demand for the fire-resistant fabrics market during the forecast period.

- The Chinese government plans to have at least 5,000 fuel-cell electric vehicles by 2025 and 1 million by 2030. The government's promotion of electric, hybrid, and fuel-cell electric vehicles is expected to drive the market studied during the forecast period.

- All the abovementioned factors are expected to drive the demand for fire-resistant fabrics in the country over the forecast period.

Fire-resistant Fabrics Industry Overview

The fire-resistant fabrics market is fragmented in nature. The major companies (not in any particular order) include DuPont, Indorama Corporation, Solvay, KANEKA CORPORATION, and TenCate Protective Fabrics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Stringent Industrial Standards for Fabrics

- 4.1.2 Increasing Demand for Fire-resistant Fabrics in Home and Commercial Furnishing

- 4.1.3 Growing Demand from the Mining Industry in South America

- 4.2 Restraints

- 4.2.1 High Price of Raw Materials Used to Make Fire-resistant Fabrics

- 4.2.2 Lack of Safety Compliance

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Type

- 5.1.1 Apparel

- 5.1.2 Non-apparel

- 5.2 By Application

- 5.2.1 Industrial Protective and Mining Clothing

- 5.2.2 Transport

- 5.2.2.1 Railway

- 5.2.2.2 Aircraft

- 5.2.2.3 Automotive (Roadway)

- 5.2.2.4 Marine

- 5.2.3 Defense and Firefighting Service

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Egypt

- 5.3.5.6 Nigeria

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 DuPont

- 6.4.2 Glen Raven Inc.

- 6.4.3 Indorama Corporation

- 6.4.4 KANEKA CORPORATION

- 6.4.5 LENZING AG

- 6.4.6 Newtex Industries Inc.

- 6.4.7 PBI Fibers International

- 6.4.8 Solvay

- 6.4.9 Teijin Carbon Europe GmbH

- 6.4.10 TenCate Protective Fabrics

- 6.4.11 W. L. Gore & Associates Inc.

- 6.4.12 Westex: A Milliken Brand

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Industrialization in BRICS Countries

- 7.2 Other Opportunities