|

市場調査レポート

商品コード

1850037

米国のガスセンサ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)United States Gas Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のガスセンサ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月22日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

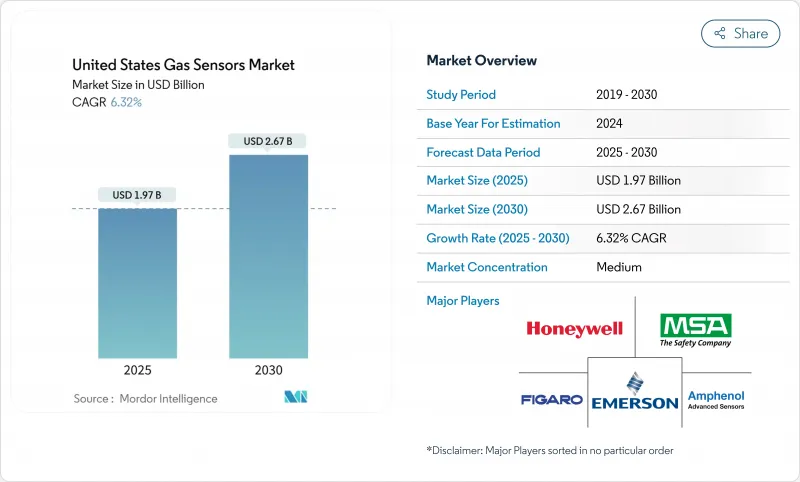

米国のガスセンサ市場規模は2025年に19億7,000万米ドルと推定され、2030年には26億7,000万米ドルに達し、CAGR 6.32%で成長すると予測されています。

需要は、工場や製油所に連続的な漏水検知システムの設置を促す連邦安全規則によって支えられており、ASHRAE換気基準の厳格化によって商業ビルでの採用が拡大しています。低電力ネットワークが設置コストを削減し、稼働時間を向上させる遠隔診断を可能にするため、無線およびIoT対応デバイスが急速に支持を集めています。エッジAI分析がセンサーノード上で直接実行されるようになり、生データをリアルタイムのアラートに変えて、コストのかかる事故の防止に役立っています。水素インフラの展開により超高感度検出器の注文が急増し、MEMSベースの設計によりサイズと電力要件が低下し、ウェアラブル機器や携帯型安全機器に新たな用途が広がっています。競合の激しさは中程度です。多角的なセーフティ・リーダーは依然としてクリティカル・プロセス・ニッチを支配しているが、半導体のスペシャリストはコンパクトでソフトウェア主導のプラットフォームでシェアを拡大しています。

米国のガスセンサ市場動向と洞察

OSHAとEPAの遵守が産業需要を牽引

メタンガスや有毒ガスの排出に関する規制の更新により、工場はより低いしきい値で漏れを確認する必要があり、1日あたり2万5,000米ドルに達する罰則が課されることもあります。そのため、施設は10億分の1濃度を検出するマルチガスアレイに投資し、コンプライアンスを超えたプロセス制御の価値を付加しています。エンジニアリング・チームは現在、危険レベルが発生したときにシャットダウンを自動化する安全計装システムと統合する検出器を指定しています。テキサス州、ルイジアナ州、ペンシルベニア州の石油・ガス・化学クラスターでは、コンプライアンスへの支出が最も多く、サプライヤーにとって確実な収益源となっています。大手バイヤーは、規制当局への報告を簡素化する校正プログラムやクラウドベースの監査証跡に支えられた製品ラインを好みます。

HVAC/IAQの採用拡大(ASHRAE 62.1)

2024年のASHRAE 62.1の更新により、CO2メーターの精度目標が厳しくなったため、ビル事業者は古いハードウェアを高度な光学式または電気化学式デバイスに交換するようになりました。オフィスタワー、病院、学校では、現在、ガス測定値を空気処理装置にリンクさせる稼働率ベースの換気制御を統合し、省エネと健康基準のバランスを取っています。ポートフォリオ・オーナーは、室内空気データをテナント維持をサポートするアメニティとみなし、ガスセンサーを裏方設備からウェルネス・ブランディングの目に見える部分へと昇華させています。最も導入が進んでいるのは北東部とカリフォルニア州で、州からの奨励金と持続可能性の義務化が組み合わされています。システム・インテグレーターは、センサーを分析ダッシュボードにバンドルし、故障警告と換気スコアカードを単一のビューで提供しています。

高い校正とメンテナンスコスト

四半期ごとの較正プロトコルは、特殊なテストガス、訓練を受けたスタッフ、そして機器の生涯所有コストを40%にまで押し上げるダウンタイムを必要とします。小規模なプラントでは、サービス間隔が遅れることが多く、安全への投資を損なう誤報や未検出の漏れのリスクがあります。メーカーは、自己較正セルや遠隔診断で対応しているが、資本価格は上昇し、購入者は、先行的な節約と経常的な労働とを比較検討することを余儀なくされます。農村部での技術不足は負担を増大させ、一部の事業者はセンサー、サービス、コンプライアンス文書作成をバンドルしたメンテナンス契約をアウトソーシングすることを余儀なくされています。

セグメント分析

2024年の米国のガスセンサ市場では、無停電電源とフェイルセーフ通信を必要とするプロセス産業に支えられ、有線カテゴリが54%のポジションを維持した。これらの設備は通常、分散型制御システムに直接接続し、危険区域でのコンプライアンスを確保します。しかし、ワイヤレスノードは、バッテリー寿命を5年以上に延ばす低消費電力広域技術に後押しされ、CAGR 11.5%で成長しています。施設管理者は、ターンアラウンド時や、ケーブル配線がコスト的に困難なレガシー・ビルでの一時的な配置を可能にするメッシュ・ネットワークを導入しています。ワイヤレスの柔軟性は、きめ細かなセンサー配置をサポートし、より良い換気の洞察を求める多層階の学校や病院でのカバレッジを向上させます。インテグレーターは、ワイヤレス・ガス・データを稼働率やエネルギー指標と組み合わせることで、安全性だけでなく運用効率にも価値を提供します。

ワイヤレス・オプションの台頭は、サービス・モデルの形も変えています。ベンダーは現在、ハードウェア、ネットワーク接続、分析ダッシュボードを1つの契約にまとめたサブスクリプション・パッケージを提供しています。このシフトにより、資本予算が削減され、新しいセンサーが登場した際には、常時アップグレードが可能になります。無線設備に関連する米国のガスセンサの市場規模が上昇するにつれて、調達チームは生涯価値とソフトウェア機能を重視したトータルコスト評価に軸足を移しています。危険度の高いエリアでは有線システムが標準であることに変わりはないが、クラスIディビジョン1のゾーンでは常設の有線検知器と、危険度の低いスペースでは無線デバイスを組み合わせ、費用を最適化するハイブリッド・アーキテクチャが出現しています。

電気化学セルは、CO、H2S、NO2に対する精度が実証されているため、2024年の米国のガスセンサ市場シェアの31.5%を占めました。触媒ビーズ設計は、クラスi環境における可燃性ガス用の有力な選択肢として存続し、NDIR光学系はHVAC制御におけるCO2用として人気を集めました。PIDは、危険物対応や産業衛生キャンペーンでVOCを監視するニッチな役割を果たしました。

MEMS MOSデバイスは、半導体生産がユニットあたりのコストを削減し、コインサイズのパッケージで複数のガスの識別を可能にするため、2025年から2030年にかけて13.2%のCAGR成長を遂げる見込みです。機械学習アルゴリズムが交差感度を補正し、単一のダイでメタン、水素、揮発性有機物を文脈に応じた精度で識別できるようにします。一人で作業する人の安全を確保するためのウェアラブル機器や民生用電子機器は、これらのチップを統合することで、危険な環境をリアルタイムでユーザーに警告することができます。また、MEMSへの移行は消費電力を低減し、ワイヤレスノードのバッテリー寿命を延ばし、頻繁なバッテリー交換を抑制する持続可能性の目標に合致します。

米国のガスセンサー市場は、タイプ別(有線、無線)、ガスタイプ別(酸素、一酸化炭素など)、技術別(電気化学、光イオン化検出器(PID)など)、用途別(医療・ヘルスケア、ビルディングオートメーションなど)に分類されます。市場予測は金額(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- OSHAとEPAのコンプライアンスが産業界の需要を牽引

- HVAC/IAQの採用拡大(ASHRAE 62.1)

- 自動車の車内空気質と排出ガスの監視

- エッジAIとIoTを活用した予知保全

- 水素燃料補給漏れ検知システムの展開

- IIJAパイプラインプログラムにおけるメタン漏洩規制

- 市場抑制要因

- 校正とメンテナンスのコストが高め

- センサー価格のコモディティ化

- 国内MEMS工場の生産能力のボトルネック

- クラウド接続センサーのサイバーセキュリティの懸念

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- パンデミックとマクロ経済への影響評価

第5章 市場規模と成長予測

- タイプ別

- 有線

- 無線

- ガスの種類別

- 酸素

- 一酸化炭素

- 二酸化炭素

- 窒素酸化物

- 炭化水素

- その他

- 技術別

- 電気化学

- 光イオン化検出器(PID)

- ソリッドステート/MOS

- 触媒ビーズ

- 赤外線(NDIR)

- 半導体

- 用途別

- 医療とヘルスケア

- ビルオートメーション

- 産業安全とプロセス

- 食品・飲料

- 自動車

- 運輸・物流

- その他の用途

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Honeywell International Inc.

- Sensirion AG

- Amphenol Advanced Sensors

- Figaro Engineering Inc.

- Emerson Electric Co.

- MSA Safety Inc.

- Robert Bosch GmbH

- City Technology Ltd

- Renesas Electronics Corp.

- AMS OSRAM AG

- Trolex Ltd

- Sensata Technologies

- Draeger Safety AG

- NevadaNano

- Aeroqual Ltd

- SPEC Sensors LLC

- AlphaSense Inc.

- Figaro USA Inc.

- Membrapor AG

- Cubic Sensor and Instrumentation