|

市場調査レポート

商品コード

1851289

ガスセンサー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Gas Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ガスセンサー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月10日

発行: Mordor Intelligence

ページ情報: 英文 155 Pages

納期: 2~3営業日

|

概要

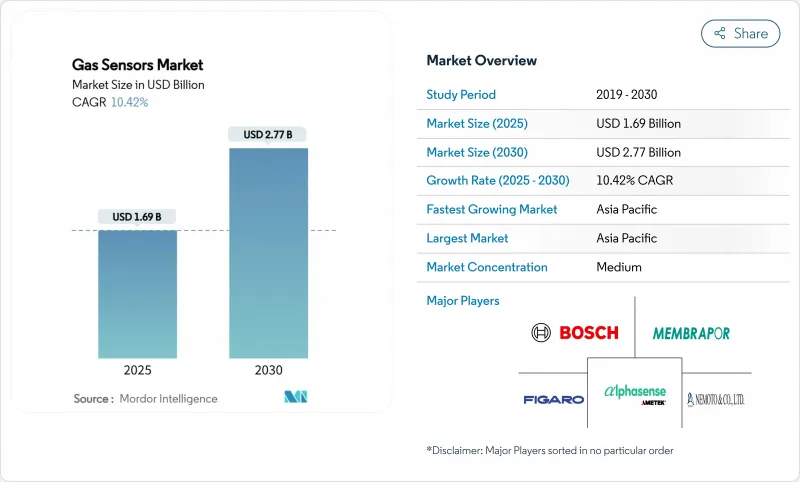

ガスセンサー市場は2025年に16億9,000万米ドル、2030年には27億7,000万米ドルに達し、CAGR 10.42%で成長すると予測されます。

Euro 7車載診断の急速な採用、職場の安全規則の厳格化、スマートシティの大気質への取り組みがセンサーの出荷を加速しています。平均販売価格を押し上げ、人工知能ベースの選択性を可能にする、電気化学から小型化されたMEMS半導体光学プラットフォームへの移行が勢いを強めています。アジア太平洋地域は、自動車とエレクトロニクス製造基盤のおかげで最大の地位を占めており、炭化水素と揮発性有機化合物デバイスは、メタン漏れ規制を背景に最も急速に拡大しているガスタイプです。しかし、10ppm以下の交差感度やウエハー価格の変動といった技術的なハードルが、コストに敏感なニッチ分野での採用を抑制する可能性があります。

世界のガスセンサー市場動向と洞察

自動車オンボード診断の厳格化がセンサーの統合を促進

Euro 7およびEPA Tier 3規制では、自動車のライフサイクル全体にわたって窒素酸化物、粒子状物質、炭化水素を継続的に追跡することが自動車メーカーに義務付けられており、-40℃~70℃の動作に耐える堅牢なマルチガスアレイの需要が高まっています。ボッシュのレーダー対応センシングモジュールとハネウェルのバッテリー安全電解質検出器は、コンプライアンス要件が内燃機関と電気プラットフォームを同様に包含していることを示しています。15年という長期耐久性が義務付けられたことで、短寿命の電気化学セルではなく、ソリッドステートとNDIRソリューションが推進されています。

作業現場での安全義務化が産業界への導入に拍車をかける

ISO 45001、OSHAの閉鎖空間基準、REACH物質上限規制の世界的な採用により、工場は連続固定検出器、個人バッジ、携帯型スニッファーの導入を余儀なくされています。化学プロセス、バッテリー製造ライン、半導体クリーンルームでは、自己較正し、クラウドダッシュボードにデータを記録するMEMSアレイにアップグレードしています。工場全体のデジタルツインプラットフォームとの統合は、ダウンタイムと保険料を削減する予測的介入をサポートします。

交差感度の課題が精密アプリケーションを制限

研究所のテストでは、低コストのホルムアルデヒド・セルがオゾンと二酸化窒素による偽陽性を登録し、屋外ステーションとしては不適格であることが示されています。農業用アンモニアモニターも同様の干渉に直面し、選択的なスズドープ酸化インジウム膜は狭い分析対象物窓でしか機能しないです。有機金属フレームワーク・フィルターや機械学習分類器は識別能力を向上させるが、材料費がかさむため、大衆市場向けウェアラブル製品への採用は抑制されます。

セグメント分析

一酸化炭素検知器は、家庭用警報器、炉の監視、車室内の安全性により2024年の販売量を独占し、ガスセンサー市場シェアの26.40%を確保しました。しかし、炭化水素・VOC検知器は、OGMP 2.0メタン規則がエネルギー企業に逃散排出の追跡を義務付けるため、CAGR 12.30%で同業他社を凌駕すると予測されます。このシフトにより、ガスセンサー市場はメタン、エタン、ベンゼンを同時に定量化し、石油・ガス事業者の総所有コストを削減するマルチスペシャルアレイへとリバランスします。300nWの消費電力で1~1,000ppmの水素を測定するナノトランジスタベースの検出器が登場し、バッテリーモジュール、ドローン、家庭用燃料電池システムにモニタリングの幅を広げています。

炭化水素ブームは、都市全体の漏出マッピングプログラムを構築する環境モニタリング請負業者にとって、対応可能なガスセンサー市場規模を拡大します。メタン専用チップのOEM需要も、成熟した一酸化炭素と酸素のカテゴリーにおける価格下落を部分的に相殺し、ユニット当たりの平均収益を押し上げます。一方、安定した酸素欠乏症用製品は冶金とパルプ工場で関連性を保ち、二酸化炭素NDIRセルは室内空気質に関する法規制の波に乗っています。特殊な二酸化硫黄と硫化水素の測定器は、製油所の煙突や採掘トンネルに限定されているが、ハイスペックサプライヤーのニッチな収益性を支えています。

電気化学素子は、実証済みの現場での信頼性と初期コストの低さにより、2024年に32.10%のシェアを維持し、産業用安全計装システムのエコシステムの中心であり続ける。MEMS-半導体光スタックは、固有の選択性、ドリフト耐性、機械学習ベースのパターンライブラリとの互換性により、2030年まで16.00%のCAGRで推移すると予測されており、状況は急速に変化しています。キャリブレーション不要のライフサイクルを要求する自動車、HVAC、消費者向けIoTエンドポイントに関連するガスセンサー市場規模は、この急増によって上昇します。

ハイブリッド・デバイスは、光学、電気化学、金属酸化物の原理を1つのパッケージに統合したもので、複数のディスクリート基板を置き換え、調達を合理化します。ボッシュ・センサーテックのBME688「エレクトロニック・ノーズ」は、食品の腐敗や森林火災の前兆を検知するAI対応のシグネチャーを展示。パルス駆動MEMSヒーターとディープ・ニューラル・ネットワークの組み合わせにより、水素、一酸化炭素、アンモニアの識別精度が100%に達しました。ソフトウェアの比重が高まるにつれて、ファームウェアの無線アップデートが決定的な差別化要因となり、ハードウェア中心のライバルが分析ベンダーと提携するよう促しています。

ガスセンサーガスタイプ(酸素、一酸化炭素、その他)、技術(電気化学、光イオン化、その他)、フォームファクター(固定/現場モジュール、携帯/ハンドヘルドデバイス、その他)、接続性(有線、無線)、最終用途産業(産業安全&プロセス、自動車パワートレイン&HVAC、その他)、地域別に市場を細分化。市場予測は金額(米ドル)で提供されます。

地域分析

アジア太平洋地域は、2024年の収益シェア43.30%でガスセンサー市場を牽引し、2030年までのCAGRは14.04%となる見込み。中国のスマートシティの青写真は、何万もの低コストのノードを必要とするブロックレベルの汚染グリッドを義務付けています。一方、ISO 45001への準拠を推進するインドは、自動車、セメント、特殊化学品セクターの工場フロアの改修を促進しています。日本では水素社会への野心がサブppmの安全モニターの受注を加速させ、韓国では半導体の拡張が国内MEMSサプライチェーンの種をまいています。ウィンセンエレクトロニクスやフィガロエンジニアリングのような地元のチャンピオンは、部品の集積と労働力の裁定を活用して輸出市場と国内市場の両方に対応し、ガスセンサー市場における持続的なリーダーシップを支えています。

北米は、成熟しつつもイノベーション主導の場です。EPAの第3次排気ガス規制、スーパーエミッタープログラム、カナダの75%メタン削減目標が、忠実度の高い漏れ検知ネットワークへの需要を育んでいます。テキサス州とアルバータ州の石油採掘事業者は、衛星フィードにネットワーク接続された光学式メタン・カメラを配備し、米国中西部のバッテリー・ギガ工場の拡張工事では、作業員保護のためにマルチガス電気化学ラックが指定されています。センサーOEMメーカーとソフトウェア企業の合弁事業では、データ量を圧縮しIPを保護するエッジ分析モジュールが開発され、サービスへの価値移行が強化されています。

欧州は引き続き規制中心です。ユーロ7は、小型車と大型車のNOx後処理プローブを推進し、2024年に採択されたEU全体のメタン規制は、フレアとコンプレッサーを継続的に監視するよう上流エネルギー企業に求めています。ドイツのグリーン・スティール・パイロット・ラインは、クローズド・ループ・バーナーに酸素と水素のゲージを統合し、スカンジナビアの都市は、5Gで接続された自転車道の大気質標識にNO2とO3セルを追加しています。データ主権に関する法令は、オンプレミスのサーバーと暗号化された無線プロトコルを奨励し、国境を越えたセンサー・フリートの調達仕様を形成しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 車載診断の厳格化(Euro 7、EPA Tier 3)

- 職場の安全義務化(OSHA、REACH、ISO 45001)

- IoT対応大気質モニタリングの展開(スマートシティ)

- 水素製造と燃料電池バリューチェーン(グリーン水素)の需要急増

- 石油・ガスにおける新たなメタン漏れ検知ルール(OGMP2.0)

- 小型化したMEMSベースのマルチガスアレイ(3mm以下)がASPの上昇を牽引

- 市場抑制要因

- 混合ガスマトリックスにおける10ppm以下の交差感受性の課題

- シリコン供給の不安定さがウエハー価格を押し上げる

- 世界の校正標準の欠如が互換性を妨げる

- 中国の低価格電化製品サプライヤーからのコスト圧力(価格競争)

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- ガスタイプ別

- 酸素

- 一酸化炭素(CO)

- 二酸化炭素(CO2)

- 窒素酸化物(NOx)

- 炭化水素(VOC/CH4)

- その他のガス(SO2、H2Sなど)

- 技術別

- 電気化学

- 光イオン化(PID)

- ソリッドステート/MOS

- 触媒ビーズ

- 非分散赤外線(NDIR)

- MEMS半導体オプティカル

- フォームファクター別

- 固定/設置型モジュール

- ポータブル/ハンドヘルドデバイス

- ウェアラブルバッジ/パッチ

- 接続性別

- 有線(4-20 mA、CAN、RS-485)

- ワイヤレス(BLE、NB-IoT、LoRaWAN)

- 最終用途産業別

- 産業安全とプロセス(石油・ガス、化学製品)

- 自動車パワートレインとHVAC

- ビルディングオートメーション/スマートホーム

- 医療・ライフサイエンス機器

- 飲食品とコールドチェーン物流

- 環境モニタリングとスマートシティノード

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Robert Bosch GmbH

- Honeywell International Inc.-City Technology

- Dragerwerk AG & Co. KGaA

- Figaro Engineering Inc.

- Sensirion Holding AG

- AlphaSense Inc.

- Amphenol SGX Sensortech Ltd.

- Membrapor AG

- Nemoto and Co., Ltd.

- Niterra Co., Ltd.(NGK-NTK)

- Delphi Technologies(BorgWarner Inc.)

- Senseair AB(Asahi Kasei Microdevices)

- Dynament Ltd.

- Siemens AG-BT Sensors

- ABB Ltd.-Ability(TM)Gas Analytics

- Yokogawa Electric Corporation

- Emerson Electric Co.-Rosemount

- Teledyne FLIR LLC

- General Electric Company-Panametrics

- Zhengzhou Winsen Electronics Technology Co., Ltd.