|

市場調査レポート

商品コード

1851392

ワイン包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Wine Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ワイン包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月13日

発行: Mordor Intelligence

ページ情報: 英文 118 Pages

納期: 2~3営業日

|

概要

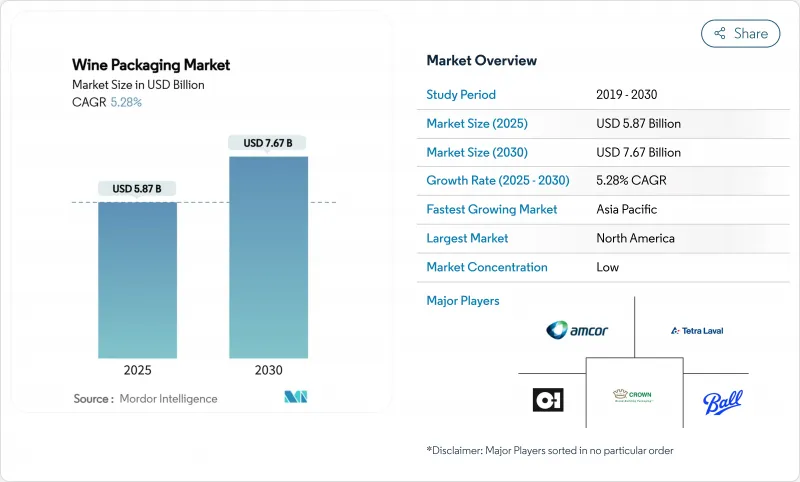

ワイン包装の市場規模は2025年に58億7,000万米ドルに達し、2030年には76億7,000万米ドルに達すると予測され、期間中のCAGRは5.28%で推移します。

旺盛なガラス瓶需要、軽量デザインへの関心の高まり、缶やバッグ・イン・ボックスなどの代替フォーマットの急速な採用が、この軌道の舵を切っています。中国におけるプレミアム化、欧州における軽量ガラスの展開、北米における消費者への直接販売(DtC)の加速は、ワイン包装市場全体の生産規模と物流経済性を再構築しています。EUの2030年までの100%リサイクル義務化からカリフォルニア州の償還価値拡大までの規制圧力は、ガラス価格の変動が続く中でも、サプライヤーを循環型材料とエネルギー効率の高い炉へと押しやり続けています。金属パッケージのリサイクル性は、若く移動の多い消費者にアピールし、バイオベースのクロージャーは、ブドウ園が持続可能性の実践を認証するにつれて支持を集めています。

世界のワイン包装市場の動向と洞察

中国におけるワインのプレミアム化がデザイナーズボトルの需要を高める

中国の若い都市部の消費者は、利便性と手頃な価格を重視しながらも、洗練されたデザインを品質と結び付けています。Huadong Wineryの樽ワインやFranziaのボックスワインなどのイノベーションは、ブランド・エクイティを薄めることなくカジュアルな集まりをサポートし、ワイン包装市場においてプレミアム・スタイルの選択肢を引き上げています。

CO2削減のための欧州ワイナリーによる軽量ガラス瓶の採用

Bourgogneのカーボンニュートラル・ロードマップは、ボトルの重量が重要な排出促進要因であることを明らかにしました。Veralliaの300gのBordeaux Airは、より軽いボトルで伝統を維持しながらCO2を最大40%削減できることを証明し、ワイン包装市場全体でより広範な採用を促進しました。

EUプラスチック包装税でPETソリューションのコストが上昇

PFASの使用禁止と再生材含有率の義務化により、PETのコンプライアンスコストが上昇し、ワイン包装市場のプレミアムラインでの競争力が低下しています。

セグメント分析

ガラスはその不活性な性質と高級感により、2024年のワイン包装市場の68.22%を占めました。軽量炉のアップグレードとカレット比率の向上は、排出量を削減しながらリーダーシップを維持するのに役立っています。金属のCAGR 8.43%は、アルミニウムのリサイクル性とチルスピードの優位性を反映しており、アウトドア志向の消費者を魅了し、ワイン包装市場全体の将来の嗜好を形成しています。Frugalpac社の紙ボトルとPETハイブリッドは、規制当局が100%リサイクル可能な目標を推進する中、素材分野の幅を広げています。

プラスチックと紙の進歩は、長年のヒエラルキーを試します。Frugalpac社のファイバーシェルは、ガラスよりもプラスチックの使用量が77%少なく、カーボンフットプリントも84%低いです。ガラスメーカーは、電気炉や超軽量設計を試験的に導入することで対抗しています。アルミボトルはリシーラブルトップを活用して鮮度を長持ちさせ、バイオベースのPETは最大30%のrPETを統合しているが、リサイクル原料の供給拡大を待っています。

従来のボトルは、2024年の売上の55.76%を占め、貯蔵と儀式用の軸となっています。それでも缶はCAGR 7.88%で成長しており、ワイン包装市場内のシングルサーブの利便性とスタジアムの規制を満たしています。バッグ・イン・ボックスのラインはスケールメリットを達成し、スウェーデンの数量の56%を占め、プレミアム・グレードの進化を物語っています。

PETボトルは、アルプラのバリア層により6ヶ月の賞味期限でニッチな役割を確保し、パウチはフェスティバルのシェアを獲得しています。EUのデジタル義務に対応したスマートラベルは、ボトルにも缶にも貼られ、トレーサビリティを充実させ、ワイン包装市場のオムニチャネル戦略を強化しています。

地域分析

北米が最大の売上貢献国であることに変わりはないです。カリフォルニア州では、DtC法とリサイクル拡大により、5セントと10セントのデポジットが統合され、ワイン包装市場をカーブサイド対応デザインへと誘導しています。欧州の政策は2030年までに100%のリサイクルを可能にすることを定めており、電気炉への投資と貨物排出量を削減するバッグ・イン・ボックスの革新に拍車をかけています。

アジア太平洋が2030年までの成長をリードします。中国のプレミアム化はデザイナーズ・ガラスと費用対効果の高い箱をミックスし、オーストラリアの補助金は軽量PETボトルと紙ボトルを支持し、ワイン包装市場の地域的な勢いを加速させる。電子食料品の利便性が環境マーケティングと絡み合って、若い消費者を転換させる。

中東・アフリカと南米が新たな道筋を提供。温暖な気候の地域では、より軽量で酸化バリア性の高い包装形態が好まれ、輸出業者はEUの規則を満たしながら運賃を最小限に抑える包装を採用しています。国内の生産者は、新たな飲用者を獲得するためにrPETや缶詰ラインを模索し、ワイン包装業界の革新が世界的に広がっていることを示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 中国におけるワインのプレミアム化がデザイナーズボトルの需要を高める

- 欧州ワイナリーの軽量ガラス瓶採用でCO2削減へ

- 北欧の電子食料品チャネルにおけるバッグ・イン・ボックスの急速な普及

- 米国における消費者直販(DtC)チャネルの台頭がオンプレミス包装を加速する

- オセアニアにおける屋外消費用缶入りワインとPETシングルサーブ・ワインの急増

- ブドウ園の持続可能性認証がバイオベースの栓の採用を促進

- 市場抑制要因

- EUプラスチック包装税がPETソリューションのコストを上昇させる

- 世界のリサイクル原料供給不足がrPETワインボトルの展開を制限

- プレミアムワインの普及を阻む代替栓の酸素透過リスクの高さ

- ソーダ灰の価格変動がガラス瓶コストを押し上げる

- サプライチェーン分析

- テクノロジーの展望

- 規制の見通し

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 素材タイプ別

- ガラス

- プラスチック

- 金属

- 紙

- 製品タイプ別

- ガラス瓶

- ペットボトル

- バッグインボックス

- 缶

- ポーチ

- クロージャタイプ別

- 天然コルク

- テクニカル/合成コルク

- スクリューキャップ

- クラウンキャップ

- その他(Tストッパー、ビノロック)

- ワインタイプ別

- スティルワイン

- スパークリングワイン

- 酒精強化ワインとデザートワイン

- 低アルコール・ノンアルコールワイン

- 容量別

- 375mL未満

- 375-750 mL

- 750-1,500 mL

- 1,500mL以上

- 流通チャネル別

- 直接販売

- 間接販売

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア、ニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Owens-Illinois Inc.(O-I)

- Verallia SA

- Ardagh Group SA

- Saverglass SAS

- Vetropack Holding AG

- BA Glass Group

- Consol Glass Pty Ltd

- Guala Closures Group

- Amorim Cork, S.A.

- Vinventions LLC(Nomacorc)

- Amcor plc

- Ball Corporation

- TricorBraun Inc.

- Tetra Laval International SA

- SIG Combibloc Group AG

- Scholle IPN(Sealed Air)

- Liqui-Box(Sealed Air)

- International Paper Company

- G3 Enterprises Inc.

- Maverick Enterprises Inc.

- Encore Glass Inc.

- Smurfit WestRock

- Crown Holdings, Inc.