欧州のエンタープライズファイアウォール:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Enterprise Firewall - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639511

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

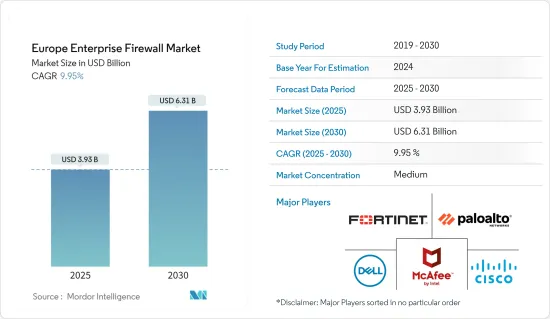

欧州のエンタープライズファイアウォールの市場規模は、2025年に39億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.95%で、2030年には63億1,000万米ドルに達すると予測されています。

サイバーセキュリティのスキル格差が続く中、企業は今後数年間、管理が容易で設定や監視に必要な専門知識が少ない最適なソリューションとしてファイアウォールを求める可能性があります。

主なハイライト

- エンタープライズファイアウォールは、ネットワーク・セキュリティに不可欠なユニットです。ファイアウォールは、企業ネットワーク内のインバウンドおよびアウトバウンドのデータパケットの流れを、事前に定義された値のセットと照らし合わせて検査し、ネットワーク内の悪意のある活動を検出します。

- さらに、欧州には一般データ保護規則(GDPR)など、世界で最も厳しいデータ保護規制があります。例えば、欧州データ保護委員会(EDPB)は、データ保護法が欧州連合全体で一貫して遵守されることを保証する責任を負う独立組織です。一般データ保護規則(GDPR)はEDPBを創設しました。この地域で事業を展開する企業は、これらの規制を確実に遵守し、ユーザーデータを保護するために、ファイアウォールを含む強固なセキュリティ対策を導入することを余儀なくされています。

- さらに、「信頼せず、常に検証する」という原則を強調するゼロ・トラスト・セキュリティ・モデルが支持されるようになった。ファイアウォールは、ユーザーID、デバイスの姿勢、その他のコンテキスト要因に基づくアクセス制御を実施する上で重要な役割を果たしました。Oktaのレポートによると、2021年、欧州の組織の82%がゼロトラスト支出を増加させたが、同地域で減少を報告した企業はありません。予算削減が浸透している中でのこの結果であり、セキュリティソリューションとしてのゼロトラストの重要性が浮き彫りになった。

- クラウド技術の出現により、ファイアウォールが導入されるようになり、どのようなデバイスでもファイアウォールを利用できるようにし、どのようなトラフィックワークロードにも対応し、組織全体で同様のポリシーを実施するバンドルソリューションが提供されています。

- ウェブ・アプリケーションの急速な利用、クラウド技術の急速な採用、サイバー攻撃のリスクを軽減するためのセキュリティ・サービスへの需要の高まりも、欧州のエンタープライズファイアウォール市場の成長を後押ししています。セキュリティ侵害やサイバー攻撃からデータと情報を保護するため、ネットワークセキュリティファイアウォールの導入がさまざまな最終用途の企業で拡大しています。その結果、ネットワークセキュリティファイアウォール市場全体の成長を牽引しています。

- しかし、この地域のレガシーシステムや時代遅れのネットワークアーキテクチャを持つ組織は、最新のファイアウォールソリューションを導入する際に互換性の問題で助けを必要とするかもしれないです。これは、高度なファイアウォールの採用を遅らせたり、妨げたりする可能性があります。

欧州のエンタープライズファイアウォール市場動向

企業におけるクラウドサービス採用の増加が市場成長を促進

- 組織のプロセスは、拡張性、柔軟性、リソースへのアクセス性を提供するクラウドサービスによって大きく変化しています。しかし、クラウドサービスを利用する個人が増えるにつれて、クラウドベースの環境で使用されるデータ、アプリ、インフラを保護するためのエンタープライズファイアウォールなどの強力なセキュリティ対策に対する需要が高まっています。

- 欧州中の企業が、生産性の向上、ワークフローの再編成、消費者ニーズの変化に対応したイノベーションを目指し、デジタルトランスフォーメーションに取り組んでいます。スケーラブルなインフラ、SaaS(Software as a Service)アプリケーション、PaaS(Platform as a Service)オプションを提供することで、クラウドサービスはこの変革のフレームワークとして機能します。しかし、この移行には、クラウドベースの資産を保護するための適切なセキュリティ・ソリューションが必要です。

- 例えば、Eurostatによると、クラウド・コンピューティング・サービスを購入したEU企業の大多数(94%)が、クラウドサービスとしてのセキュリティ・ソフトウェア・アプリケーションを含むクラウドSaaS(Software as a Service)を少なくとも1つ利用しています。さらに、すべての企業規模におけるクラウドSaaSの採用率は約94%と報告されており、これはセキュリティ・ソリューションを含むクラウドベースのアプリケーションが広く採用されていることを示しています。この高い採用率は、企業がサイバーセキュリティを含む業務を強化するためにクラウドベースのツールを採用していることを示しています。

- また、クラウドコンピューティングの成長に伴い、脅威の状況は複雑さを増しており、マルウェアやランサムウェアによる攻撃の急増を防御し、クラウドシステム全体で一貫したセキュリティを提供できる最新のセキュリティソリューションの必要性が浮き彫りになっています。SonicWall Cyber Threat Report 2022によると、欧州では、マルウェア攻撃とランサムウェアの取り組みが、それぞれ前年比29%増、63%増と大幅に増加しています。また、ランサムウェアの標的国上位11カ国のうち7カ国が欧州(英国、イタリア、ドイツ、オランダ、ノルウェー、ポーランド、ウクライナ)であり、この地域のサイバー脅威環境の変化を示しています。

英国が大きな市場シェアを占める見込み

- 英国は、さまざまなサイバーセキュリティ企業、研究機関、熟練した専門家を含む強固で成熟したサイバーセキュリティ・エコシステムを誇っています。このエコシステムは、エンタープライズファイアウォール技術を含む高度なサイバーセキュリティ・ソリューションの革新と開発を促進しています。

- 金融とビジネスの中心地である英国では、多くの国際企業、金融機関、技術系企業が事業を展開しています。これらの企業が機密データ、知的財産、消費者データを保護するために高度なサイバーセキュリティ・ソリューションを必要としている結果、エンタープライズ・ファイアウォールはかなりの需要があります。

- また、同国はさまざまな業界でデジタルトランスフォーメーションを積極的に推進しています。組織が業務を近代化し、クラウドサービスを採用し、IoTデバイスを受け入れるにつれて、これらのデジタルイニシアチブを保護するための高度なファイアウォール・ソリューションの必要性が極めて重要になっています。

- さらに、DSIT UKによると、2022年には、英国の登録サイバーセキュリティ企業のほとんどが、サイバーセキュリティに関連する指導、製品、ソリューションの提供など、専門的なサイバーサービスを提供していました。ネットワーク・セキュリティの登録率は約61%で、企業が最も頻繁に提供する重要なサービスの第2位と記録されています。このような重要なネットワーク・セキュリティ登録企業は、不正アクセス、データ侵害、マルウェア、その他のサイバー攻撃からネットワークを守る上で重要な役割を果たす、エンタープライズファイアウォールの機能と密接に連携しています。

- さらに、この国には、ファイアウォール・システムの構築、適用、管理に貢献する、知識の豊富なサイバーセキュリティ専門家が多数存在します。例えば、国家統計局(英国)の報告によると、英国のクリエイティブ産業におけるIT、ソフトウェア、コンピュータ・サービスのサブセクターの雇用者数は、2022年9月時点で100万人を超え、前年は94万人を記録しました。このうち約10万8000人は自営業者です。このような労働人口の大幅な増加率は、業界全体における高度なセキュリティ対策の展開を支えています。

欧州のエンタープライズファイアウォール産業概要

欧州のエンタープライズファイアウォール市場は、世界プレイヤーとローカルプレイヤーの存在により、半統合が予想されます。プレーヤーは、業界内の専門知識を組み合わせることにより、自社のソリューションを強化するために積極的にパートナーシップやコラボレーションに従事しています。エンタープライズファイアウォール市場の有力プレーヤーには、Cisco Systems、Dell Inc.、Palo Alto Networks、Fortinet Inc.などが含まれます。

2023年5月、パロアルトネットワークスは、フルマネージドAzureネイティブISVサービスとして、MLを搭載した次世代ファイアウォール(NGFW)をMicrosoft Azureに提供すると発表しました。Cloud NGFW for Azureは、Advanced Threat Prevention、Advanced URL Filtering、WildFire、DNS Securityなどの高度な機能を備えた完全なセキュリティ・ソリューションを提供します。さらに同社は、Cloud NGFW for Azureが西欧で利用可能になったことにも言及しています。

2023年2月、英国を拠点とするサイバーセキュリティ・サービス・プロバイダーであるソフォスは、エンタープライズグレードのXGSシリーズアプライアンス2機種を新たに投入し、次世代ファイアウォールのポートフォリオを拡充することを発表しました。新しいXGS 7500および8500モデルは、大企業やキャンパス内に最適なパフォーマンスと保護を提供し、サポートするチャネルパートナーの市場展望を拡大する可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 企業におけるクラウドサービス導入の増加

- サイバー脅威環境の開発

- データプライバシーとデータ漏えいの結果に対する意識の高まり

- 市場抑制要因

- ファイアウォールを既存のネットワーク・インフラに統合することの難しさ

- 専門家が限られていることによるファイアウォールの導入と管理の複雑さ

第6章 技術スナップショット

第7章 市場セグメンテーション

- 展開タイプ別

- オンプレミス

- クラウド

- ソリューション別

- ハードウェア

- ソフトウェア

- サービス別

- 組織規模別

- 中小企業

- 大規模組織

- エンドユーザー業界別

- ヘルスケア

- 製造業

- 政府機関

- 小売

- 教育

- 金融サービス

- その他業界別

- 国別

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

第8章 競合情勢

- 企業プロファイル

- Fortinet Inc.

- Palo Alto Networks

- McAfee(Intel Security Group)

- Dell Inc.

- Cisco Systems Inc.

- The Hewlett-Packard Company

- Juniper Networks

- Check Point Software Technologies

- Huawei Technologies Inc.

- Sophos Group PLC

- Netasq SA

- WatchGuard Technologies

- SonicWall Inc.

第9章 投資分析

第10章 市場の将来

目次

The Europe Enterprise Firewall Market size is estimated at USD 3.93 billion in 2025, and is expected to reach USD 6.31 billion by 2030, at a CAGR of 9.95% during the forecast period (2025-2030).

As the cybersecurity skills gap persists, enterprises in the coming years may seek firewalls as an optimal solution that is easier to manage and requires less specialized expertise for configuration and monitoring.

Key Highlights

- Enterprise firewalls are essential units of network security. They examine the flow of inbound and outbound data packets in an enterprise network against a set of predefined values to detect any malicious activity in the network.

- Moreover, Europe has some of the strictest data protection regulations worldwide, such as the General Data Protection Regulation (GDPR). For example, the European Data Protection Board (EDPB) is an independent organization responsible for ensuring that data protection laws are consistently followed across the entire European Union. The General Data Protection Regulation (GDPR) created the EDPB. Enterprises operating in the region are compelled to implement robust security measures, including firewalls, to ensure compliance with these regulations and protect user data.

- Moreover, the zero trust security model gained traction, emphasizing the principle of "never trust, always verify." Firewalls played a key role in enforcing access controls based on user identity, device posture, and other contextual factors. According to Okta's report, in 2021, 82% of European organizations boosted their Zero Trust expenditures, while no company in the region reported a drop. This occurs when budget cuts have been prevalent, highlighting the significance of Zero Trust as a security solution.

- With the emergence of cloud technology, firewalls are now being deployed, which offer a bundled solution that ensures the availability of a firewall on any device, addresses any traffic workload, and enforces similar policies across the organization.

- The rapid use of web applications, rapid adoption of cloud technologies, and the increasing demand for security services to mitigate the risk of cyberattacks are also driving the growth of the enterprise firewall market in Europe. In order to protect the data & information from security breaches and cyber-attacks, the implementation of network security firewalls is growing across various end-use enterprises. Consequently, driving the growth of the overall network security firewalls market.

- However, organizations with legacy systems or outdated network architectures in the region might need help with compatibility issues when implementing modern firewall solutions. This could delay or hinder the adoption of advanced firewalls.

Europe Enterprise Firewall Market Trends

Increasing adoption of Cloud Services among Enterprises to Drive the Market Growth

- Organizational processes have been significantly altered by cloud services, which offer scalability, flexibility, and accessibility to resources. However, as more individuals utilize cloud services, the demand for strong security measures, such as corporate firewalls, to safeguard the data, apps, and infrastructure used in cloud-based environments is rising.

- Businesses all around Europe are undertaking a digital transformation to increase productivity, reorganize workflows, and innovate in response to shifting consumer needs. By delivering scalable infrastructure, Software as a Service (SaaS) applications, and Platform as a Service (PaaS) options, cloud services serve as a framework for this transformation. However, this transition requires adequate security solutions to protect cloud-based assets.

- For instance, the majority (94%) of EU businesses who purchased cloud computing services also utilized at least one cloud Software as a Service (SaaS), which includes security software applications as a cloud service, according to Eurostat. Additionally, the adoption of cloud SaaS across all corporate sizes has been reported to be approximately 94%, which signifies the widespread adoption of cloud-based applications, including security solutions. This high adoption rate indicates businesses are embracing cloud-based tools to enhance their operations, including cybersecurity.

- Also, the complexities of the threat landscape increase with the growth of cloud computing, highlighting the need for modern security solutions that can defend against the upsurge in malware and ransomware assaults and offer consistent security across cloud systems. As per SonicWall Cyber Threat Report 2022, Malware assaults and ransomware efforts significantly increased in Europe by 29% and 63%, respectively, year over year. In addition, seven of the top 11 ransomware target nations in terms of volume were in Europe (United Kingdom, Italy, Germany, Netherlands, Norway, Poland, and Ukraine), indicating a change in the region's cyber threat environment.

United Kingdom is Expected to Hold a Significant Market Share

- The United Kingdom boasts a robust and mature cybersecurity ecosystem that includes various cybersecurity companies, research institutions, and skilled professionals. This ecosystem fosters innovation and the development of advanced cybersecurity solutions, including enterprise firewall technologies.

- Many international enterprises, financial institutions, and technological firms operate in the United Kingdom, a major financial and business center. Enterprise firewalls are in considerable demand as a result of these enterprises' necessity for advanced cybersecurity solutions to safeguard their confidential data, intellectual property, and consumer data.

- Also, the country is actively pursuing digital transformation across various industries. As organizations modernize their operations, adopt cloud services, and embrace IoT devices, the need for advanced firewall solutions to secure these digital initiatives becomes crucial.

- Moreover, in 2022, according to DSIT UK, most of the United Kingdom's registered cyber security companies provided professional cyber services, including offering guidance, products, or solutions associated with cyber security. Network security was recorded to be registering around 61%, the second most significant service that businesses offered the most frequently. Such significant network security registered firms in the country align closely with the functionalities of enterprise firewalls, which play a crucial role in safeguarding networks from unauthorized access, data breaches, malware, and other cyber attacks.

- Additionally, the nation is host to a pool of knowledgeable cybersecurity experts who contribute to the creation, application, and administration of firewall systems. For instance, the Office for National Statistics (UK) reported that the IT, software, and computer services sub-sector in the UK's creative industries employed more than one million individuals as of September 2022, compared with the previous year, recording 940,000. About 108,000 of these individuals were self-employed. Such a significant growth rate in the workforce supports the deployment of sophisticated security measures across industries.

Europe Enterprise Firewall Industry Overview

The Europe enterprise firewall market is expected to be Semi consolidated owing to the presence of global and local players. The players are actively engaging in partnerships and collaborations to enhance their solutions through combined expertise in the industry. Prominent players in the enterprise firewall market include Cisco Systems, Dell Inc., Palo Alto Networks, and Fortinet Inc.

In May 2023, Palo Alto Networks announced that as a fully managed Azure-native ISV service, the firm will deliver its ML-powered next-generation Firewall (NGFW) to Microsoft Azure. Cloud NGFW for Azure provides a complete security solution with advanced capabilities, including Advanced Threat Prevention, Advanced URL Filtering, WildFire, and DNS Security. Moreover, the firm mentioned that Cloud NGFW for Azure is made available in West Europe.

In February 2023, Sophos, a United Kingdom-based cybersecurity service provider, announced the expansion of its next-generation firewall portfolio with two new enterprise-grade XGS Series appliances. The new XGS 7500 and 8500 models may offer large enterprises and campus installations optimal performance and protection, expanding market prospects for the supporting channel partners.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness- Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing adoption of Cloud Services among Enterprises

- 5.1.2 Developing Cyber Threat Environment

- 5.1.3 Increasing Awareness of Data Privacy and Consequences of Data Breaches

- 5.2 Market Restraints

- 5.2.1 Difficulty in Integrating Firewalls with Existing Network Infrastructure

- 5.2.2 Complexity of Deploying and Managing Firewalls due to Limited Expertise

6 TECHNOLOGY SNAPSHOT

7 MARKET SEGMENTATION

- 7.1 By Type of Deployment

- 7.1.1 On-premises

- 7.1.2 Cloud

- 7.2 By Solution

- 7.2.1 Hardware

- 7.2.2 Software

- 7.2.3 Services

- 7.3 By Size of the Organization

- 7.3.1 Small to Medium Organizations

- 7.3.2 Large Organizations

- 7.4 By End-User Verticals

- 7.4.1 Healthcare

- 7.4.2 Manufacturing

- 7.4.3 Government

- 7.4.4 Retail

- 7.4.5 Education

- 7.4.6 Financial Services

- 7.4.7 Other End-User Verticals

- 7.5 By Country

- 7.5.1 Germany

- 7.5.2 United Kingdom

- 7.5.3 France

- 7.5.4 Russia

- 7.5.5 Spain

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Fortinet Inc.

- 8.1.2 Palo Alto Networks

- 8.1.3 McAfee (Intel Security Group)

- 8.1.4 Dell Inc.

- 8.1.5 Cisco Systems Inc.

- 8.1.6 The Hewlett-Packard Company

- 8.1.7 Juniper Networks

- 8.1.8 Check Point Software Technologies

- 8.1.9 Huawei Technologies Inc.

- 8.1.10 Sophos Group PLC

- 8.1.11 Netasq SA

- 8.1.12 WatchGuard Technologies

- 8.1.13 SonicWall Inc.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日