|

市場調査レポート

商品コード

1639509

バイオ有機酸-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Bio-Organic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バイオ有機酸-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

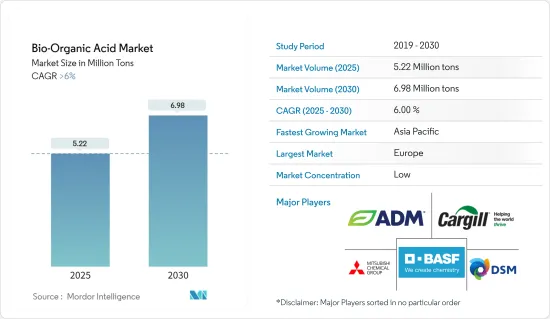

バイオ有機酸の市場規模は2025年に522万トンと推定され、予測期間(2025~2030年)のCAGRは6%を超え、2030年には698万トンに達すると予測されます。

COVID-19パンデミックは、全国的な封鎖、厳しい社会的遠ざけ対策、サプライチェーンの混乱により市場に悪影響を与えました。これらの要因は飲食品、繊維、塗料市場に悪影響を及ぼし、バイオ有機酸市場に影響を与えました。しかし、規制解除後、市場は順調に回復しました。飲食品、繊維、コーティングのエンドユーザー産業におけるバイオ有機酸の消費増加により、市場は大幅に回復しました。

従来の有機酸に対する厳しい規制と、医療用途でのバイオベースポリマー需要の増加が、バイオ有機酸市場を牽引すると予想されます。

バイオベースの化学品の製造コストが高いことが、市場の成長を妨げると予想されます。

環境に優しい製品へのシフトは、予測期間中に市場に機会を創出すると予想されます。

アジア太平洋が市場を独占すると予想されます。また、医薬品、繊維製品、コーティング剤、食品用途でのバイオ有機酸の需要増加により、予測期間中に最も高いCAGRで推移すると予想されます。

バイオ有機酸市場の動向

市場を独占する飲食品産業

- 予測期間中、飲食品エンドユーザー産業がバイオ有機酸市場を独占すると予想されます。バイオ有機酸とその誘導体は、飲料、食品、飼料の生産で頻繁に使用されます。酸性添加物は、酸度を調整する緩衝剤、酸化防止剤、保存料、風味増強剤、封鎖剤として機能することがあります。

- 北米と欧州は世界最大の飲食品市場です。米国国勢調査局によると、米国の小売と食品サービスによる月間小売売上高は、9月の7,049億米ドルに対し、2023年11月には約7,057億米ドルとなりました。このように、飲食品市場の拡大が同国のバイオ有機酸市場を牽引することになります。

- さらに、米国農務省によると、メキシコは米国、ブラジルに次いで南北アメリカ第3位の食品加工産業です。農業市場諮問グループ(GCMA)のデータによると、同国の食品生産量は2022年の2億8,700万トンから2023年には2億9,000万トンに達すると予想されています。

- 飲食品部門は欧州最大の製造業のひとつです。FoodDrinkEuropeによると、飲食品産業の売上高は2022年第4四半期に前期比2.3%増、2021年第4四半期比では前年同期比19.2%増となりました。従って、飲食品市場の売上高の伸びは、同地域のバイオ有機酸市場を牽引すると予想されます。

- ドイツは欧州最大の飲食品市場です。食品産業は同国で4番目に大きな産業部門です。ドイツ飲食品産業連盟(BVE)のデータによると、2022年、同国の飲食品加工総収入は207億米ドルに達し、前年比成長率は17.9%でした。従って、飲食品部門の成長がこの地域のバイオ有機酸市場を牽引すると予想されます。

- したがって、飲食品エンドユーザー産業は、予測期間中にバイオ有機酸の市場を独占すると予想されます。

市場成長を支配するアジア太平洋

- アジア太平洋は、同地域の医薬品、繊維、コーティング、飲食品エンドユーザー産業からの需要増加により、バイオ有機酸市場を独占すると予想されます。

- 中国とインドは同地域最大の飲食品市場です。中国国家軽工業委員会によると、年間売上高280万米ドル以上の主要食品製造企業は、2022年に1兆5,300億米ドル以上の収益を計上しました。2021年と比較すると、総収入は前年比5.6%増を記録し、食品産業の力強い成長を示しています。

- 同様にインドでも、飲食品部門は大幅な成長率を記録すると予想されます。IBEFによると、インドの食品加工市場規模は2022年に307兆2,000億米ドルに達し、2028年には547兆3,000億米ドルに達すると予想されています。したがって、食品加工市場の成長により、同国ではバイオベースの有機酸の使用量が増加すると考えられます。

- バイオ有機酸の需要は医薬品セクターで増加しています。インドは世界の医薬品ハブであり、200カ国以上に医薬品を輸出しています。2022~2023年上半期、製薬産業への海外直接投資流入額は25%増加しました。IBEFによると、製薬産業の収益は2024年までに650億米ドルに達すると予想されています。したがって、医薬品市場の拡大が現在の研究市場を牽引することになります。

- さらに中国では、繊維産業が大幅な市場成長を記録しました。中国国家統計局によると、中国の繊維生産量は前年同期の235億メートルに対し、2022年には382億メートルに達しました。12月には、約34億7,000万メートルの衣料用生地が中国で生産されました。毎月の繊維生産量は常に30億メートルを上回っています。

- 上記の要因から、アジア太平洋のバイオ有機酸市場は予測期間中に大きく成長すると予測されます。

バイオ有機酸産業概要

バイオ有機酸市場は細分化されています。同市場の主要企業(順不同)には、BASF SE、DSM、Mitsubishi Chemical Corporation、Cargill, Incorporated、ADMなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 従来の有機酸に対する厳しい規制

- 医療用途におけるバイオベースポリマーの需要拡大

- その他の促進要因

- 抑制要因

- バイオベース化学品の製造コストの上昇

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- 原料

- バイオマス

- トウモロコシ

- トウモロコシ

- 砂糖

- その他の原料

- 製品タイプ

- バイオ乳酸

- バイオ酢酸

- バイオアジピン酸

- バイオアクリル酸

- バイオコハク酸

- その他の製品タイプ(バイオクエン酸、バイオフマル酸など)

- 用途セグメント

- ポリマー

- 医薬品

- 繊維製品

- コーティング

- 飲食品

- その他の用途(パーソナルケア、化学など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ADM

- Abengoa

- BASF SE

- BioAmber Inc

- Braskem

- Cargill, Incorporated

- Corbion

- Cosun

- DSM

- Genomatica

- Gfbio

- Mitsubishi Chemical Corporation

- NatureWorks LLC

- Novozymes

- PTT Global Chemical Public Company Limited

第7章 市場機会と今後の動向

- 環境に優しい製品へのシフト

- その他の機会

The Bio-Organic Acid Market size is estimated at 5.22 million tons in 2025, and is expected to reach 6.98 million tons by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market due to nationwide lockdowns, strict social distancing measures, and disruption in supply chains. These factors negatively affected the food and beverage, textile, and coating markets, thereby affecting the market for bio-organic acids. However, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of bio-organic acids in food and beverage, textile, and coating end-user industries.

The stringent regulations over conventional organic acids and the growing demand for bio-based polymers in healthcare applications are expected to drive the market for bio-organic acids.

The higher production cost of bio-based chemicals is expected to hinder the growth of the market.

The shifting focus towards eco-friendly products is expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for bio-organic acids in pharmaceuticals, textiles, coatings, and food products applications.

Bio-Organic Acid Market Trends

Food and Beverage Industry to Dominate The Market

- The food and Beverage end-user industry is expected to dominate the market for bio-organic acid during the forecast period. Bio-organic acids and their derivatives are frequently used in beverage, food, and feed production. Acidic additives may act as buffers to regulate acidity, antioxidants, preservatives, flavor enhancers, and sequestrants.

- North America and Europe are the largest markets for food and beverages across the globe. According to the U.S. Census Bureau, monthly retail sales from U.S. retail and food services were valued at around USD 705.7 billion in November 2023, as compared to USD 704.9 billion in September. Thus, the increasing market for food and beverage products will drive the market for bio-organic acids in the country.

- Furthermore, according to the USDA, Mexico is the third-largest food processing industry in the Americas, after the United States and Brazil. According to data from the Agricultural Markets Advisory Group (GCMA), the country's food production is anticipated to reach 290 million tons in 2023, growing from 287 million tons in 2022.

- The food and beverage sector is one of the largest manufacturing industries in Europe. According to FoodDrinkEurope, the food and beverage industry turnover increased by 2.3% in Q4 2022, compared to the previous quarter, and increased by 19.2% Y-o-Y compared to Q4 2021. Thus, the growth in food and beverage market turnover is expected to drive the market for bio-organic acid in the region.

- Germany is the largest market for food and beverage products in Europe. The food industry represents the fourth-largest industrial sector in the country. According to data from the Federation of German Food and Drink Industries (BVE), in 2022, the total revenue of food and beverage processing in the country reached USD 20.7 billion, at a growth rate of 17.9% as compared to the previous year. Thus, the growth in the food and beverage sector is expected to drive the market for bio-organic acids in the region.

- Thus, the food and beverage end-user industry is expected to dominate the market for bio-organic acid during the forecast period.

Asia-Pacific Region to Dominate the Market Growth

- The Asia-Pacific region is expected to dominate the market for bio-organic acid due to rising demand from pharmaceuticals, textiles, coatings, food and beverage end-user industries in the region.

- China and India are the largest food and beverage markets in the region. According to the China National Light Industry Council, major food manufacturing companies with an annual turnover of over USD 2.8 million reported revenues of over USD 1.53 trillion in 2022. Compared to 2021, the total revenue registered a year-on-year growth of 5.6%, indicating strong growth in the food industry.

- Similarly, in India, the food and beverage sector is expected to register a significant growth rate. According to IBEF, Indian food processing market size reached USD 307.2 trillion in 2022 and is expected to reach USD 547.3 trillion by 2028. Thus, the growth in food processing markets will increase the usage of bio-based organic acids in the country.

- The demand for bio-organic acids is increasing in the pharmaceutical sector. India is a global pharmaceutical hub, exporting pharmaceuticals to over 200 countries. In the first half of 2022-2023, foreign direct investment inflows into the pharmaceutical industry increased by 25%. According to IBEF, the pharmaceutical industry revenue is expected to reach USD 65 billion by 2024. Thus, the increasing market for pharmaceuticals will drive the current studied market.

- Furthermore, in China, the textile industry registered significant market growth. According to the National Bureau of Statistics of China, China's textile production volume accounted for 38.2 billion meters in 2022, compared to 23.5 billion meters during the same period in the previous year. In December, approximately 3.47 billion meters of clothing fabric were produced in China. Monthly textile production volume was consistently above three billion meters.

- Owing to the above-mentioned factors, the market for bio-organic acid in the Asia-Pacific region is projected to grow significantly during the forecast period.

Bio-Organic Acid Industry Overview

The bio-organic acid market is fragmented in nature. Some of the major players in the market (not in any particular order) include BASF SE, DSM, Mitsubishi Chemical Corporation, Cargill, Incorporated, and ADM, amongst others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Stringent Regulations Over Conventional Organic Acids

- 4.1.2 Growing Demand for Bio-based Polymer in Healthcare Applications

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Higher Production Cost of Bio-based Chemicals

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Raw Material

- 5.1.1 Biomass

- 5.1.2 Corn

- 5.1.3 Maize

- 5.1.4 Sugar

- 5.1.5 Other Raw Materials

- 5.2 Product Type

- 5.2.1 Bio Lactic Acid

- 5.2.2 Bio Acetic Acid

- 5.2.3 Bio Adipic Acid

- 5.2.4 Bio Acrylic Acid

- 5.2.5 Bio Succinic Acid

- 5.2.6 Other Product Types (Bio Citric Acid, Bio Fumaric Acid, etc.)

- 5.3 Application

- 5.3.1 Polymers

- 5.3.2 Pharmaceuticals

- 5.3.3 Textile

- 5.3.4 Coatings

- 5.3.5 Food and Beverage

- 5.3.6 Other Applications (Personal Care, Chemicals, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Abengoa

- 6.4.3 BASF SE

- 6.4.4 BioAmber Inc

- 6.4.5 Braskem

- 6.4.6 Cargill, Incorporated

- 6.4.7 Corbion

- 6.4.8 Cosun

- 6.4.9 DSM

- 6.4.10 Genomatica

- 6.4.11 Gfbio

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 NatureWorks LLC

- 6.4.14 Novozymes

- 6.4.15 PTT Global Chemical Public Company Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Focus Towards Eco-Friendly Products

- 7.2 Other Opportunities