|

市場調査レポート

商品コード

1639462

フィリピンのリテール業界:市場シェア分析、産業動向、成長予測(2025年~2030年)Philippines Retail Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フィリピンのリテール業界:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

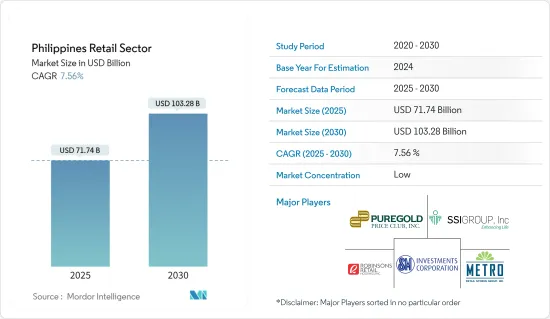

フィリピンのリテール市場規模は2025年に717億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは7.56%で、2030年には1,032億8,000万米ドルに達すると予測されます。

コンビニエンス食品の需要は、フィリピンのリテール市場の堅調な成長を支える重要な要因です。最小限の調理で済むこれらの製品は、特に多忙な個人や働く女性人口の増加に伴い、家庭料理よりも加工肉や鶏肉のような簡便食品を選ぶ人気の選択肢となっています。

フィリピンのリテール業界情勢は顕著な好転を見せており、業界各社は多様なリテールセグメントにおける好調な成長率に乗じています。特に高級品は、推定成長率30%で、東南アジアのトップランナーになる勢いです。さらに、フィリピンのリテールeコマースセクターは、東南アジアの他のセクターを凌ぐ勢いです。このリテールの急成長は、供給網と流通網が拡大し、消費者が様々な商品やサービスにアクセスしやすくなったことが主な要因です。

フィリピンのリテール市場の動向

フィリピンの飲食品セクター:国家経済の重要な柱

フィリピンの飲食品セクターは、GDPの半分近くを占めるなど、フィリピン経済の重要な原動力となっています。フィリピンの製造業の中では、この部門だけでGDPの約25%を占めています。フィリピンはアジアの主要な食料生産国の一つとして際立っています。この成長は、中流階級と上流階級の可処分所得の増加によって推進されています。特筆すべきは、25~34歳の年齢層が裁量的支出において依然として圧倒的な力を持っていることで、この傾向は今後10年間続くと予想されます。米国農務省は、業界の収益が6%増加し、今年は350億米ドルに達すると予測しています。

レストラン、ファーストフードチェーン、グラブハブ(Grubhub)やキャビア(Caviar)のようなフードデリバリーアプリの普及により、フィリピンの飲食品需要は大幅な成長を遂げようとしています。さらに、消費者は有機食品、自然食品、生鮮食品の健康上のメリットを認識するようになっており、この需要をさらに促進しています。

オンライン流通チャネルが市場で台頭

堅調なインターネットとスマートフォンの普及率の恩恵を受けて、フィリピンは東南アジアで最も急速に拡大しているeコマース市場の1つとして際立っています。COVID-19の流行は消費者行動に顕著な変化をもたらし、実店舗よりもオンライン・プラットフォームを好む傾向が顕著となった。フィリピンでは、Lazada、Shopee、Zalora、Ebay、Kimstoreなどがオンライン・マーケットプレースの主要企業です。特に、中国のeコマースの巨人アリババの支援を受けたラザダは、中国を拠点とするプラットフォーム、タオバオを通じてASEAN市場にも進出しています。同時に、Foodpandaとセブン-イレブンとの提携のような注目すべき提携により、ASEANではオンライン食料品ショッピングが急増しています。eコマースの展望が広がるにつれ、デジタル決済サービスの採用も進んでいます。買い物客のかなりの部分は店舗での購入に回帰しているが、飲食品のeコマース分野は、小規模とはいえ、製品輸入の有望な可能性を示しています。

フィリピンのリテール業界の概要

フィリピンのリテール業界は断片的です。リテール市場における大手企業は数社に過ぎないです。しかし、既存プレイヤーの拡大と新たなビジネスチャンスの出現により、このセクター自体は急速な成長を遂げています。特筆すべきは、リテール業の様相が変化していることで、小規模で構造化されていない店舗が、スーパーマーケットやハイパーマーケット、リテールチェーンといった大規模な業態に取って代わられています。この変革は、今後数年間も勢いを増すと予測されます。業界をリードするのは、以下のような大手企業です。 SM Investments Corp., SSI Group, Puregold Price Club Inc., Metro Retail Stores Group Inc., and Robinsons Retail Holdings Inc.

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の洞察と力学

- 市場概要

- 市場促進要因

- 包装食品と調理済み食品の需要増加が市場を牽引

- アパレル、化粧品、履物、時計、飲食品などのブランド商品カテゴリーに対する需要の増加

- 市場抑制要因/課題

- 消費者の購買行動の変化とブランド意識の高まり

- 市場機会

- インターネット普及率の上昇が市場の成長をもたらす

- バーチャルアシスタントとデジタル決済の台頭

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 消費者行動分析

- リテール業界の技術革新に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 製品別

- 飲食品

- パーソナルケアとハウスホールドケア

- アパレル

- フットウェア・アクセサリー

- 家具

- 玩具・ホビー

- 家電製品

- その他製品

- 流通チャネル別

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- 百貨店

- 専門店

- オンライン

- その他の流通チャネル

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- SM Investments Corp.(SM Retail Inc.)

- Puregold Price Club Inc.

- SSI Group Philippines

- Metro Retail Sores Group Inc.

- Robinsons Retail Holdings Inc.

- Rustan Supercenters Inc.

- Alfamart

- 7-Eleven

- Golden ABC Inc.

- Mercury Drug Corp.*

第7章 市場動向

第8章 免責事項と出版社について

The Philippines Retail Market size is estimated at USD 71.74 billion in 2025, and is expected to reach USD 103.28 billion by 2030, at a CAGR of 7.56% during the forecast period (2025-2030).

The demand for convenience food products is a key driver behind the robust growth of the retail market in the Philippines. These products, requiring minimal preparation, have become popular choices, especially among busy individuals and the rising working female population, who are opting for convenience foods like processed meats and poultry over home-cooked meals.

The retail landscape in the Philippines is witnessing a notable upswing, with industry players capitalizing on the buoyant growth rates across diverse retail segments. Luxury goods, in particular, are poised to be the frontrunners in Southeast Asia, with an estimated growth rate of 30%. Additionally, the retail e-commerce sector in the Philippines is set to outpace its counterparts in Southeast Asia. This retail surge is largely attributed to the expanding supply and distribution networks, facilitating enhanced accessibility to various goods and services for consumers.

Philippines Retail Market Trends

The Philippines' Food and Beverage Sector: A Key Pillar of the Nation's Economy

The food and beverage sector in the Philippines is a vital driver of the nation's economy, accounting for nearly half of its GDP. Within the country's manufacturing landscape, this sector alone contributes to about 25% of the GDP. The Philippines stands out as one of Asia's major food producers. This growth is propelled by the rising disposable incomes of the middle and upper classes. Notably, the 25-34 age group remains a dominant force in discretionary spending, a trend expected to persist for the coming decade. The US Department of Agriculture projects a 6% rise in the industry's revenue, reaching USD 35 billion this year, primarily attributed to an improved labor scenario.

With the proliferation of restaurants, fast food chains, and food delivery apps like Grubhub and Caviar, the demand for food and beverages in the Philippines is poised for significant growth. Moreover, consumers are increasingly recognizing the health benefits of organic, natural, and fresh foods, further fueling this demand.

The Online Distribution Channel is Emerging in the Market

Benefiting from robust internet and smartphone penetration rates, the Philippines stands out as one of Southeast Asia's most rapidly expanding e-commerce markets. The COVID-19 pandemic further catalyzed a pronounced shift in consumer behavior, with a notable preference for online platforms over brick-and-mortar stores. In the Philippines, key players in the online marketplace landscape include Lazada, Shopee, Zalora, Ebay, and Kimstore. Notably, Lazada, backed by Chinese e-commerce titan Alibaba, has been extending its footprint to ASEAN markets via its China-based platform, Taobao. Concurrently, the nation has been witnessing a surge in online grocery shopping, with notable collaborations like Foodpanda's partnership with 7-Eleven stores. As the e-commerce landscape expands, so does the adoption of digital payment services. While a significant portion of shoppers have reverted to in-store purchases, the e-commerce segment for food and beverages, albeit small, showcases a promising potential for product imports.

Philippines Retail Industry Overview

The retail industry in the Philippines is fragmented. There are only a few big players in the retail market. However, the sector itself is experiencing rapid growth, driven by the expansion of existing players and the emergence of new business opportunities. Notably, the retail landscape is shifting, with smaller, unstructured stores making way for larger formats like supermarkets, hypermarkets, and retail chains. This transformation is projected to continue gaining momentum in the coming years. Leading the pack are prominent players such as SM Investments Corp., SSI Group, Puregold Price Club Inc., Metro Retail Stores Group Inc., and Robinsons Retail Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 The Rising Demand for Packaged and Ready to Eat Food is Driving the Market

- 4.2.2 Increase in the Demand for Branded Goods Categories such as Apparel, Cosmetics, Footwear, Watches, Beverages, and Food

- 4.3 Market Restraints/Challenges

- 4.3.1 Changing Consumer Buying Behavior and Rising Brand Consciousness

- 4.4 Market Opportunities

- 4.4.1 Increase in Internet Penetration Leads to Growth in the Market

- 4.4.2 Virtual Sales Assistants and Rising Digital Payment Options

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.7 Consumer Behavior Analysis

- 4.8 Insights into Technological Innovations in the Retail Industry

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Products

- 5.1.1 Food and Beverage

- 5.1.2 Personal and Household Care

- 5.1.3 Apparel

- 5.1.4 Footwear and Accessories

- 5.1.5 Furniture

- 5.1.6 Toys and Hobbies

- 5.1.7 Electronic and Household Appliances

- 5.1.8 Other Products

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Department Stores

- 5.2.4 Specialty Stores

- 5.2.5 Online

- 5.2.6 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 SM Investments Corp. (SM Retail Inc.)

- 6.2.2 Puregold Price Club Inc.

- 6.2.3 SSI Group Philippines

- 6.2.4 Metro Retail Sores Group Inc.

- 6.2.5 Robinsons Retail Holdings Inc.

- 6.2.6 Rustan Supercenters Inc.

- 6.2.7 Alfamart

- 6.2.8 7-Eleven

- 6.2.9 Golden ABC Inc.

- 6.2.10 Mercury Drug Corp.*