|

市場調査レポート

商品コード

1906942

液体包装用カートン:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Liquid Packaging Cartons - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 液体包装用カートン:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

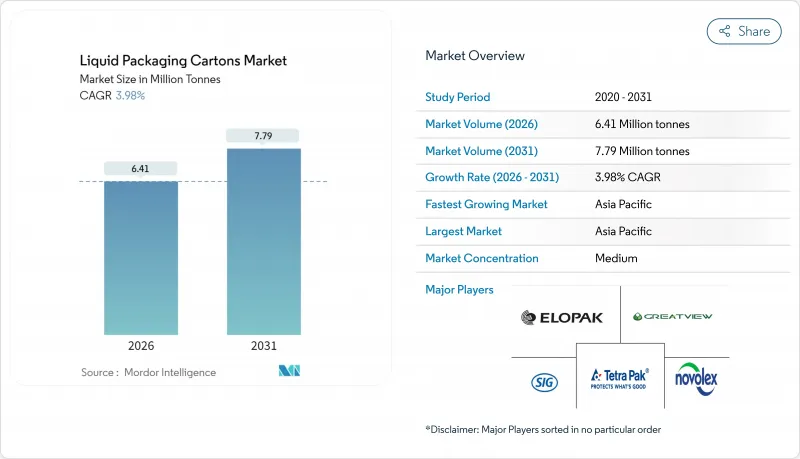

液体包装用カートン市場は、2025年に616万トンと評価され、予測期間(2026-2031年)においてCAGR 3.98%で成長し、2026年の641万トンから2031年までに779万トンに達すると推定されています。

繊維系素材を推奨する規制の勢い、保存期間を延長するバリア技術の革新、食料品小売業の急速なデジタル化が、成熟経済圏と新興経済圏の両方で液体包装用カートン市場の拡大を促進しています。アジア太平洋地域では、公的栄養プログラムや食品接触規制の進化により常温保存可能な包装への需要が高まり、最も強い成長が見込まれます。同時に、乳製品や植物性飲料におけるプレミアム化の動向が、付加価値型カートン形式の採用を促進しています。また、持続可能性に連動した資金調達チャネルが、繊維素材の革新に向けた資本を導いています。既存企業は脱炭素化やリサイクル能力への大規模投資によりシェア防衛を図る一方、地域専門企業が現地のコスト優位性と機敏な市場参入戦略を活用しているため、競合は激化しています。

世界の液体包装用カートン市場の動向と洞察

新興アジアにおけるUHT乳製品の需要

インドネシアの無料栄養食プログラムにより、同国の乳製品消費量は2024年の420万トンから2025年には530万トンへ増加し、冷蔵不要で熱帯地域の物流に耐える無菌カートンの持続的な需要創出につながっています。中国のGB 4,806食品接触規制は適合プレミアムを高め、認証を受けたカートン供給業者に液体包装カートン市場における価格決定力を付与しています。これらの要因が相まって、同地域は価値と数量の成長において主導的立場を強化し、多国籍企業による現地生産の促進や国内加工業者との長期供給契約締結を後押ししています。中産階級の所得増加は、常温保存可能な乳製品の家庭普及をさらに加速させています。これらの要素が総合的に作用し、アジア太平洋地域の世界液体包装用カートン市場への貢献度は、過去平均を大きく上回る水準に達しています。

電子商取引による食料品市場の成長が常温保存形態を推進

オンライン食料品市場は2025年までに世界の小売市場の61%を占めると予測されており、コールドチェーンの複雑さを排除し、配送コストを削減する常温保存製品への需要を促進しています。常温保存可能な飲料が最も恩恵を受け、液体包装用カートン市場はEコマース効率化の直接的な推進役として位置づけられています。小売業者は積み重ね可能で軽量、かつリサイクル可能な繊維系包装を優先しており、この移行をさらに加速させています。こうした利点は、ラストマイルの排出量や渋滞が包装選択を左右する都市部で特に強く支持されています。

PETボトルの軽量化が炭素差を縮小

軽量化が進むPETは、カートンのライフサイクルにおけるカーボン優位性を浸食しており、飲料使用事例によっては製造から廃棄までの差が1,000リットルあたり20kg CO2e未満にまで縮小しています。PETに再生素材の含有率が高まるにつれ、コストパフォーマンスが向上し、価格に敏感なジュースや水ブランドがポリマーボトルを維持する誘因となっています。そのため、特にPETエコシステムが既に十分に確立されている北米およびEU市場において、カートンサプライヤーは代替品への移行を防ぐため、バリア技術革新とリサイクル率の向上を加速させる必要があります。

セグメント分析

2025年時点で、液体包装用カートン市場における牛乳のシェアは48.30%(約300万トン)を維持しました。しかし、非乳製品代替飲料は5.42%のCAGRで急成長し、食習慣の変化、乳糖不耐症への配慮、倫理的購買行動の促進により、2031年までに市場シェアを21.80%まで拡大する見込みです。オート麦、アーモンド、大豆飲料向け液体包装用カートン市場規模は、添加物なしで栄養素を保持する無菌加工技術の恩恵を受けています。せん断応答性均質化や酵素補助粘度制御といった技術的適応には、酸化による風味劣化を抑制する堅牢なバリア材が求められます。このため、コンバーターは充填業者と協力し、保存期間とコストのバランスを取るカスタマイズ仕様を開発しています。

栄養強化や風味添加を施したプレミアム処方は製品価値を高め、ブランドオーナーが高コストの紙容器を吸収することを可能にします。乳製品は消費習慣が定着した地域、特に政府主導の学生栄養支援策が実施されている地域では依然として重要です。しかしながら乳製品分野内でも、価値は低脂肪・ビタミン強化製品へと移行しており、パッケージ上のストーリーテリングを可能にする高精細印刷対応の紙容器が好まれています。予測期間においては、乳製品と植物性カテゴリーの共存が、市場規模を食い合うのではなく、対象となる液体包装用カートン市場を拡大させる見込みです。

液体包装用カートン市場レポートは、液体タイプ(乳製品ベースのミルク、非乳製品ミルク、ジュース、エネルギー飲料・機能性飲料など)、包装タイプ(無菌カートン、ゲーブルトップカートン)、開口形式(スクリューキャップ、ストロー穴、プルタブ)、地域(北米、欧州、アジア太平洋、南米、中東・アフリカ)別に分類されています。市場予測は数量(トン)単位で提供されます。

地域別分析

アジア太平洋地域は2025年の出荷量の45.38%(約280万トン)を占め、5.92%のCAGRにより、2031年までに395万トンを超える見込みです。拡大の背景には、8,200万人の受益者を対象としたインドネシアの学校給食イニシアチブや、規制基準の強化により適合したカートン供給業者を優遇する中国の動向が挙げられます。東南アジアでは都市化が進み、外出先での飲料需要が加速しており、プルタブや小型無菌パックの需要を後押ししています。

北米は成熟市場ながら高付加価値分野で存在感を示しています。植物性ミルクの普及に伴う漸進的成長が見込まれる一方、EPR規制の強化が国内リサイクルラインへの投資を促進しています。欧州の需要は安定しており、砂糖税改革による製品改良や、PETよりも繊維素材を優先するESG融資が下支えしています。ただし、PET容器の軽量化が急速に進むことで、ディスカウントプライベートブランドジュース市場における液体包装用カートンのシェアは縮小傾向にあります。

ラテンアメリカでは、乳製品強化プログラムと拡大する中産階級の購買力が追い風となる一方、通貨変動とサプライチェーンの脆弱性が直近の上昇を抑制しています。中東・アフリカ地域では、冷蔵コストが依然として障壁となる気候下で常温保存可能な包装が乳製品へのアクセスを支え、緩やかながら着実な伸びを示しています。地域分散化により、世界の液体包装用カートン市場は地域的なショックの影響を緩和し、複数大陸にわたる均衡ある拡大に向けた基盤を築いています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 新興アジア地域におけるUHT乳製品の需要

- 電子商取引による食料品販売の成長が常温保存形態を推進

- ESG連動型融資が繊維系包装材を優遇

- 砂糖税を背景とした製品改良により、ジュース用カートン容器の採用が増加

- セルロース系バリア技術の革新によるポリマー層削減

- 乳製品および植物由来セグメントにおけるブランドの高付加価値化が、高付加価値カートンフォーマットの需要を促進しております

- 市場抑制要因

- PETボトルの軽量化によるカーボンギャップの縮小

- 無菌リサイクルインフラの不足

- パルプ不足に伴う液体用板紙価格の変動性

- 表示および食品接触規制への対応コストが、世界の規制強化に伴い上昇しています

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 液体タイプ別

- 乳製品ベースのミルク

- 植物性ミルク

- ジュース

- エネルギー飲料および機能性飲料

- その他の液体タイプ

- パッケージングタイプ別

- 無菌カートン

- ガブルトップカートン

- 開設形式別

- スクリューキャップ

- ストローホール

- プルタブ

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリアおよびニュージーランド

- インドネシア

- タイ

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Tetra Pak International SA

- SIG Group AG

- Pactiv Evergreen Inc.(Novolex)

- Elopak AS

- Greatview Aseptic Packaging Co. Ltd

- Nippon Paper Industries Co. Ltd

- UFlex Limited(ASEPTO)

- IPI Srl(Coesia)

- Lami Packaging(Kunshan)Co. Ltd

- Visy Industries

- Klabin SA

- Obeikan Industrial Investment Group

- Nampak Ltd

- Italpack Srl

- Parksons Packaging Ltd

- Shandong Bihai Packaging Materials Co. Ltd

- Southern Packaging Group Ltd