|

市場調査レポート

商品コード

1637918

インドのネットワークセキュリティおよびサイバーリスク管理:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Network Security And Cyber Risk Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのネットワークセキュリティおよびサイバーリスク管理:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

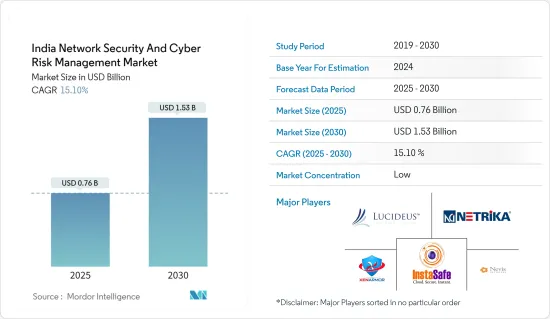

インドのネットワークセキュリティおよびサイバーリスク管理市場規模は、2025年に7億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは15.1%で、2030年には15億3,000万米ドルに達すると予測されます。

過去において、インドは主に政治的な理由からサイバー攻撃の標的となってきたが、動向から見ると、より高度な技術が利用可能になり、取引が複雑化するにつれて、システムの脆弱性が増しているため、このような状況はますます顕著になると思われます。

主なハイライト

- インド産業のデジタル化を目指す政府の取り組みが、市場の主な牽引要因になると予想されます。Make in India」、「Start-Up India」、「Digital India」などの政府スキームは、インドのサイバーセキュリティ市場の成長を補完し、官民パートナーシップ(PPP)モデルへの連結ピンとなっています。

- インドでは、重要インフラは公共部門と民間部門の両方が所有しており、サイバー攻撃からインフラを保護するための規範やプロトコルで運営されています。しかし、公的領域と民間領域で行われている取り組みを統合する国家セキュリティ・アーキテクチャは存在しないです。

- リモートワークの動向がボーダーレスなネットワーク配置へと向かう中、クラウドの導入は国際的に重要な投資目標となっています。この急速なデジタル化は、データとプライバシーに対する規制の強化、新しいテクノロジー・スタックの企業ITへの統合、クラウドとリモート・コラボレーション・テクノロジーという結果をもたらしました。

- このような変化とボードの増加は、世界なサイバーセキュリティの需要と支出を促進しています。世界の知識と経験を持つインドのITサービスと、独創的なインドのサイバーセキュリティ製品エコシステムは、顧客の世界なデジタル変革の旅を確実にする双子の成長エンジンとなっています。

- さらに、COVID-19はインドのデジタル変革の道を加速させました。当初は事業継続に重点が置かれていたが、現在ではデジタル化の力学に顕著な変化が見られます。組織が新しい現実に適応するにつれ、デジタル主導の組織戦略を開発するようになり、それがサイバー攻撃のリスクを高めています。

インドのネットワークセキュリティおよびサイバーリスク管理市場の動向

侵入検知・防御システムが市場を席巻

- 侵入検知・防御ソフトウェア(IDPS)は、ネットワーク・トラフィックを監視して攻撃の兆候を探ります。潜在的に危険な活動を検出すると、攻撃を阻止するための措置を講じる。多くの場合、悪意のあるパケットをドロップしたり、ネットワーク・トラフィックをブロックしたり、接続をリセットしたりします。また、IDPSは通常、潜在的な悪意のあるアクティビティについてセキュリティ管理者にアラートを送信します。

- IDSまたはIPSの導入と運用を成功に導く2つの主な要因は、導入されたシグネチャとそれを通過するネットワーク・トラフィックです。

- 市場は、新奇で低価格の安全な低電力侵入検知・防止ソリューションを提供するために、公的機関および商業組織の両方による研究開発費が増加した結果、拡大しています。市場規模は、家庭や商業施設の安全とセキュリティに対する意識の高まりによって拡大しています。

- さらに、製造業への投資を奨励することでインド製製品の開発、製造、組み立てを促進することを目的とした「Make in India」のような政府の取り組みや、インターネットの接続性を向上させ、国民を技術面でデジタル・エンパワーメントさせるために開始された「Digital India」のような政府のキャンペーンが、国内のIDPシステムの成長に影響を与えています。

携帯電話の成長が市場成長を大きく牽引

- インドでは技術に精通した人口が著しく増加しており、携帯電話は最初のデジタルメディアです。インドには12億人の携帯電話ユーザーがおり、そのうち7億5,000万人がスマートフォンを利用しています。今後5年間で、インドは第2位のスマートフォン製造国になると予想されています。

- インドではスマートフォンの普及に伴い、インターネットの需要も継続的に伸びています。IAMAI(The Internet and Mobile Association of India)が発表した報告書によると、国内のアクティブ・インターネット・ユーザーは現在6億9,200万人で、農村部の成長に牽引され、2025年には9億人に達すると推定されています。

- 同時に、インドのIT支出は大幅に伸びており、モノのインターネット(IoT)、クラウド・コンピューティング、人工知能(AI)、ブロックチェーンなどの技術利用も拡大しています。

- エリクソンによると、2022年、インドで使用されているスマートフォン契約数の主流技術はLTEで、約8億500万台に達しました。2024年には約8億3,860万契約でピークに達すると予想され、3G接続はその時点で2,200万と推定されました。5Gは、2027年末にはインドの全スマートフォン契約数11億3,000万件のうち約6億4,650万件になると予測されました。

インドのネットワークセキュリティおよびサイバーリスク管理産業の概要

インドのネットワークセキュリティおよびサイバーリスク管理市場は断片化されており、Lucideus Tech、Instasafe、XenArmor、ArraySheild Technologies、Netrika Consulting India Pvt Ltd.などの大手企業が存在します。同市場のプレーヤーは、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年2月- インドで保険とリスク管理サービスを提供するRaghnall Insurance Broking社は、あらゆる規模の企業向けにBusiness Cyber Shieldを発表しました。この技術は、完全なサイバーセキュリティ・ソリューションを提供することを目的としています。ビジネス・サイバー・シールドのイントロダクションより、ラグナールは、サイバー攻撃の危険性の高まりに関連するリスクを特定、最小化、管理するための最新のデジタル・ソリューションを顧客に提供することに専念していることを示します。

- 2023年1月-InstaSafeは、インドと東南アジアのテクノロジーサービスとソリューションプロバイダーであるValue InfoSolutionsと提携し、インドとSAARC地域を通じて製品提供を拡大する計画を発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因のイントロダクション

- 市場促進要因

- 産業のデジタル化に向けた政府の取り組みが市場成長を促進

- 市場抑制要因

- 国家安全保障インフラの不在が市場成長を阻害している

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- セグメント別

- セキュリティ情報・イベント管理(SIEM)

- セキュリティ・ウェブ・ゲートウェイ(SWG)

- アイデンティティ・ガバナンスと管理(IGA)

- エンタープライズ・コンテンツ・アウェア・データ・ロス防止(DLP)

- ソリューション別

- 暗号化

- アイデンティティ・アクセス管理(IAM)

- データ損失防止(DLP)

- 侵入検知システム/侵入防御システム(IDS/IPS)

- その他のソリューション

- サービス別

- ネットワークセキュリティ

- エンドポイントセキュリティ

- ワイヤレスセキュリティ

- クラウドセキュリティ

- その他のサービス

- 業界別

- 航空宇宙・防衛

- 小売

- 政府機関

- ヘルスケア

- IT&テレコム

- BFSI

第6章 競合情勢

- 企業プロファイル

- Lucideus Tech

- Instasafe

- XenArmor

- ArraySheild Technologies

- Netrika Consulting India Pvt Ltd.

- Aspirantz InfoSec

- Cyberoam

- Data Resolve Technologies

- Mirox Cyber Security & Technology

第7章 投資分析

第8章 市場機会と今後の動向

The India Network Security And Cyber Risk Management Market size is estimated at USD 0.76 billion in 2025, and is expected to reach USD 1.53 billion by 2030, at a CAGR of 15.1% during the forecast period (2025-2030).

In the past, India has been targeted through cyber-attacks primarily for political reasons, and trends show that this landscape seems to only gain prominence with the availability of more sophisticated technology and more complex transactions increasing the vulnerability of systems.

Key Highlights

- Government initiatives aimed at digitizing Indian industries are expected to be the major driving factor for the market. Government schemes such as 'Make in India,' 'Start-Up India,' and 'Digital India' supplement the growth of Cyber Security market in India and are a linking pin towards Public-Private Partnership (PPP) models.

- In India, Critical infrastructure is owned by both Public Sector and Private sector, operating with their norms and protocols for protecting their infrastructure from cyber-attacks. But there is no national security architecture that unifies the efforts taking place in the public sphere and the private sphere.

- As the trend of remote working is driving into a borderless network arrangement, cloud adoption has become a critical investment goal internationally. This fast digitization has resulted in a greater regulatory focus on data and privacy, integration of new technology stacks into company IT, and cloud and remote collaboration technologies.

- These changes and increased board are driving global cybersecurity demand and spending. Indian IT services, with their worldwide knowledge and experience, and the creative Indian cybersecurity product ecosystem have been the twin growth engines ensuring customers' global digital transformative journeys.

- Moreover, COVID-19 accelerated the country's digital transformation path. Initially, the emphasis was on business continuity, but there is now a noticeable shift in the dynamics of digitalization. As organizations adjust to the new reality, they are developing digitally led organizational strategies, which has increased the risk of cyber attacks.

India Network Security And Cyber Risk Management Market Trends

Intrusion Detection and Prevention System to Dominate the Market

- An Intrusion Detection and Prevention Software (IDPS) monitors network traffic for signs of a possible attack. When it detects potentially dangerous activity, it takes action to stop the attack. Often this takes the form of dropping malicious packets, blocking network traffic or resetting connections. The IDPS also usually sends an alert to security administrators about the potential malicious activity.

- The two main contributors to the successful deployment and operation of an IDS or IPS are the deployed signatures and the network traffic that flows through it.

- The market is expanding as a result of rising R&D expenditures by both public and commercial organisations to provide novel and affordable secured low-power intrusion detection and prevention solutions. The market size is increased by rising awareness of home and commercial safety and security.

- Moreover, government initiatives like 'Make in India', which aims to promote the development, manufacture, and assembly of products made in India by incentivizing dedicated investments into manufacturing, and government campaigns like 'Digital India,' which was launched to ensure increased Internet connectivity and make the nation digitally empowered in terms of technology, have been influencing the growth of the IDP system in the country.

Growth in Mobile Phones to Significantly Drive the Market Growth

- India has seen a tremendous growth in tech savvy population, with mobile phones being the first digital medium. In India, there are 1.2 billion mobile customers, 750 million of whom use smartphones. The nation is anticipated to be the second-largest smartphone manufacturer in the coming five years.

- With the growing number of smartphones in India, the demand for the Internet is continuously growing in the country. According to the report published by IAMAI (The Internet and Mobile Association of India), there are currently 692 million active internet users in the country, and the number is estimated to hit 900 million by 2025, led by growth in rural areas.

- At the same time, there has been substantial growth in IT spending in India and a scaling up in the use of technologies such as the Internet of Things (IoT), Cloud Computing, Artificial Intelligence (AI), and BlockChain.

- According to Ericsson, In 2022, the dominant technology of smartphone subscriptions used in India was LTE, which had reached nearly 805 million. It was expected to peak in 2024 at around 838.6 million subscriptions, with 3G connections estimated at 22 million by that point. 5G was forecasted to be about 646.5 million of all 1.13 billion smartphone subscriptions in India at the end of 2027.

India Network Security And Cyber Risk Management Industry Overview

India Network Security And Cyber Risk Management Market is fragmented, with the presence of major players like Lucideus Tech, Instasafe, XenArmor, ArraySheild Technologies, and Netrika Consulting India Pvt Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- February 2023 - Raghnall Insurance Broking, a supplier of insurance and risk management services in India, announced the launch of Business Cyber Shield for companies of all sizes. This technology is intended to offer complete cybersecurity solutions. With the introduction of Business Cyber Shield, Raghnall demonstrates its dedication to giving its clients access to the most up-to-date digital solutions for identifying, minimizing, and managing the risks connected with the rising danger of cyber-attacks.

- January 2023 - InstaSafe announced plans to expand its product offerings through India and the SAARC region by partnering with Value InfoSolutions, a technology services and solutions provider in India and Southeast Asia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Government Initiatives Towards Digitizing Industries is Driving the Market Growth

- 4.4 Market Restraints

- 4.4.1 Absence of National Security Infrastructure is Discouraging the Market Growth

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Segment

- 5.1.1 Security Information and Event Management (SIEM)

- 5.1.2 Security Web Gateway (SWG)

- 5.1.3 Identity Governance and Administration (IGA)

- 5.1.4 Enterprise Content-Aware Data Loss Prevention (DLP)

- 5.2 By Solution

- 5.2.1 Encryption

- 5.2.2 Identity and Access Management (IAM)

- 5.2.3 Data Loss Protection (DLP)

- 5.2.4 Intrusion Detection System/Intrusion Prevention System (IDS/IPS)

- 5.2.5 Other Solutions

- 5.3 By Service

- 5.3.1 Network Security

- 5.3.2 Endpoint Security

- 5.3.3 Wireless Security

- 5.3.4 Cloud Security

- 5.3.5 Other Services

- 5.4 By End-user Vertical

- 5.4.1 Aerospace and Defense

- 5.4.2 Retail

- 5.4.3 Government

- 5.4.4 Healthcare

- 5.4.5 IT & Telecom

- 5.4.6 BFSI

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Lucideus Tech

- 6.1.2 Instasafe

- 6.1.3 XenArmor

- 6.1.4 ArraySheild Technologies

- 6.1.5 Netrika Consulting India Pvt Ltd.

- 6.1.6 Aspirantz InfoSec

- 6.1.7 Cyberoam

- 6.1.8 Data Resolve Technologies

- 6.1.9 Mirox Cyber Security & Technology