|

市場調査レポート

商品コード

1849860

構造用断熱パネル:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Structural Insulated Panels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 構造用断熱パネル:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月24日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

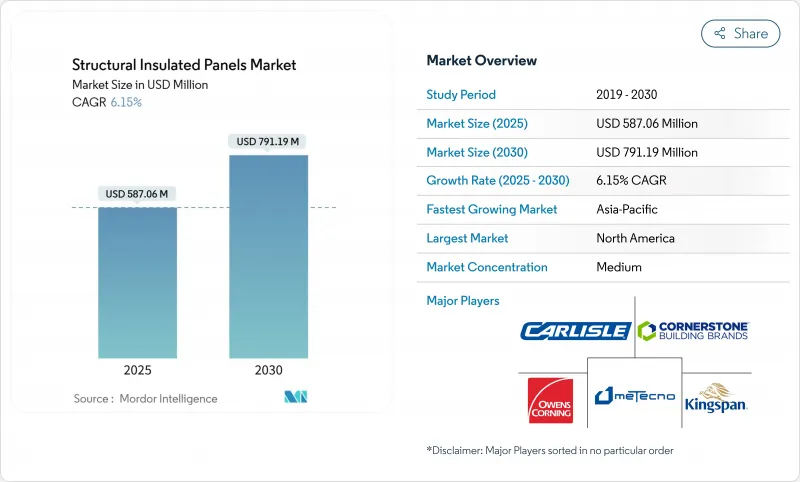

構造用断熱パネル市場の2025年の市場規模は5億8,706万米ドルで、2030年には7億9,119万米ドルに達すると予測され、CAGRは6.15%で推移します。

強い勢いは、エネルギー効率規制の強化、プレハブ化の加速、コールドチェーン・インフラの拡大から生じています。北米が規制面で主導権を維持する一方、アジア太平洋は急速な都市化により最速の数量増加を記録します。データセンター建設と温度管理されたロジスティクスは、製品革新に拍車をかけるプレミアム・ニッチを開きます。一方、配向性ストランドボード(OSB)のサプライチェーンが不安定であることと、初期コストが高いことが、幅広い普及を妨げる要因となっています。

世界の構造用断熱パネル市場の動向と洞察

採用を加速するエネルギー効率規制

2021年国際省エネルギー基準(IECC)は、米国連邦政府が融資する住宅の性能基準を34.4%引き上げます。構造用断熱パネル市場参入企業は、SIPの壁と屋根のアセンブリが、フレームを変更することなく規定のR値を満たしながら空気侵入を削減するため、利益を得ています。コロラド州のIECCの早期導入は、同州のエネルギーコード委員会がSIPをターンキーのコンプライアンス・ルートとして強調することで、州の義務付けが即座に材料シフトを引き起こすことを実証しています。商業開発業者もまた、LEEDポイントを確保するためにSIP外皮に注目し、一戸建て住宅以外の需要も拡大しています。

グローバルなコールドチェーン・インフラの拡大

コールドストア、ワクチンデポ、ラストマイル・フルフィルメントセンターは、高R値の連続断熱材を必要とします。PURおよびPIRコアSIPは、氷点下での使用に必要な寸法安定性と蒸気バリア性を備えており、従来のパネルに比べて25%のエネルギー削減が可能です。モジュール式冷蔵室は、工場で製造されたSIPを活用することで、設置時間を40%短縮し、アジア太平洋全域の食料品、医薬品、水産物の物流における迅速な拡張性をサポートします。

従来型フレームに比べて高い初期費用

EPSコアSIPは、平均で1フィート2あたり10~18米ドルであり、総建築コストに対して2~3%のプレミアムがかかります。これは、エネルギー料金の削減により5年以内にライフサイクル回収が可能であるにもかかわらず、予算重視のプロジェクトを阻害する要因になります。現在、米国でパネルを使用している住宅は全体の1~2%に過ぎず、施工業者への認知度も低いため、誤解が根強いです。インフレ抑制法に基づく連邦税制優遇措置により、現在ではその差額の一部は相殺されているが、新興市場における価格への敏感さは依然として販売量を抑制しています。

セグメント分析

EPSパネルは2024年の売上高の79.87%を占め、建築業者がより厳しい法規制に対応するためにSIPシェルを採用するなか、この材料のコスト・パフォーマンスのバランスの良さを裏付けています。構造用断熱パネル市場規模におけるこの圧倒的なシェアは、北米とアジア太平洋における安定した価格と供給を保証するEPS製造能力の普及と一致しています。また、軽量ボードは運賃を削減するため、開発者はクレーンの使用が制限される地方の土地を利用することができます。

2025年から2030年にかけて、EPSの数量はCAGR 6.29%で成長すると構造用断熱パネル市場は予測しています。PUR/PIRパネルはコールドルームやクリーンルームを保護するもので、低いk値とクローズドセル剛性が高いコストを正当化します。真空断熱とエアロゲル・コアのコンセプトは、ネット・ゼロのプロトタイプで有望視されているが、価格と取り扱いの複雑さからニッチにとどまっています。これと並行して、グラスウールコアは音響プロジェクトを引き付け、多機能アセンブリを求める建築家のための構造用断熱パネル業界ツールキットの幅を広げています。

OSBスキンは、2024年の構造用断熱パネル市場シェアの57.28%を占め、フレーミング作業員が慣れ親しんでいることと、従来の棒壁で使用されるファスナーとの互換性を活かしています。建築業者は、胴縁なしで直接被覆材を取り付けられるOSBのねじ引抜き強度を高く評価しています。

しかし、カイガラムシによる繊維不足と工場火災が供給リスクを浮き彫りにし、設計者をスチール、ファイバーセメント、酸化マグネシウムスキンに向かわせ、2030年までのCAGR成長率は7.06%となっています。金属フェーシングは、不燃性と電磁波シールドが重要なデータセンターのエンベロープに使用され、MgOボードは湿度の高い気候で耐カビ性を発揮します。これらの選択肢は調達を多様化させるが、レトロフィット作業員は工具やファスナーの選択を調整しなければならず、構造用断熱パネル市場の学習曲線は長くなります。

地域分析

北米は、2024年の世界売上高の37.12%を占め、米国がその中心となっています。米国では、連邦政府保証の住宅ローンにIECC 2021が採用され、新築住宅の主流はSIPレベルの性能となりました。カナダのメーカーは、貿易関税の摩擦にもかかわらず、国内のフレーマーと米国のプロジェクトの両方に製品を供給しており、この地域の寒冷な気候が高耐久性アセンブリの必要性を高めています。バージニア州、テキサス州、ケベック州ではデータセンターの建設が急ピッチで進んでおり、構造用断熱パネル市場にプレミアム商流を注入しています。

アジア太平洋地域の2030年までのCAGRは7.28%と最も速いです。中国の新築床面積規制には、集合住宅でのSIP使用を促進するグリーンビルディング比率が含まれており、インドのスマートシティプログラムは、パネルが敷地の回転を促進するモジュール式の手ごろな価格の住宅に資金を提供しています。現地のEPS樹脂生産能力と競争力のある労働力により、納入されるパネルコストは低く抑えられ、小規模な開発業者の間でも導入が進んでいます。日本の耐震基準は、軽量性とモーメントフレームの弾力性を併せ持つ、木材とスチールのハイブリッドSIP設計に拍車をかけ、建築に広く受け入れられています。

欧州では、建物のエネルギー性能に関する指令に支えられ、改修予算を外皮第一の戦略に振り向ける傾向が強まり、安定した需要が維持されています。スカンジナビアの建築業者は、クロスラミネート材をEPSコアと一体化させ、カーボンネガティブなモジュラーコテージを製造しています。主要3地域以外では、中東が地域の食料安全保障のために低温貯蔵能力に資金を提供し、チリが地震に耐えるSIP社会住宅のプロトタイプを実験しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- エネルギー効率規制の導入が加速

- グローバルコールドチェーンインフラの拡大

- 手頃な価格の住宅と住宅リフォームの増加

- 迅速なオフサイト建設への関心の高まり

- 木材ベースのSIPの炭素クレジット収益化

- 市場抑制要因

- 従来のフレーミングに比べて初期費用が高め

- 先進的なプレハブ壁システムによる代替の脅威

- OSB供給の不安定さ(甲虫の蔓延と工場の停止)

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品・サービスの脅威

- 競合の程度

第5章 市場規模と成長予測

- 製品別

- EPS(発泡ポリスチレン)パネル

- 硬質ポリウレタン(PUR)および硬質ポリイソシアヌレート(PIR)パネル

- グラスウールパネル

- その他の製品(例:真空断熱など)

- 肌の素材別

- 配向性ストランドボード(OSB)

- 合板

- その他の外壁材(繊維セメント板、亜鉛メッキ鋼板など)

- 用途別

- 建物の壁

- 建物の屋根

- コールドストレージ

- その他のモジュール構造(例:データセンター、フロア、デッキなど)

- エンドユーザー業界別

- 住宅用

- 商業用

- 産業および公共機関

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Alubel SpA

- ArcelorMital

- Balex-Metal

- Carlisle Companies Inc.

- Cornerstone Building Brands, Inc.

- DANA Group of Companies

- Italpannelli SRL

- Jiangsu Jingxue Energy Saving Technology Co., Ltd.

- Kingspan Group

- Manni Group

- Metecno

- Multicolor Steels(India)Pvt. Ltd.

- Nucor Building Systems

- Owens Corning

- Premium Building Systems

- Rautaruukki Corporation(Ruukki Construction)

- Structall Building Systems

- Tata Steel

- Thermocore Structural Insulated Panel Systems

- Zamil Steel Buildings India Private Limited