|

市場調査レポート

商品コード

1637799

欧州のパイプラインセキュリティ:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Pipeline Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のパイプラインセキュリティ:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

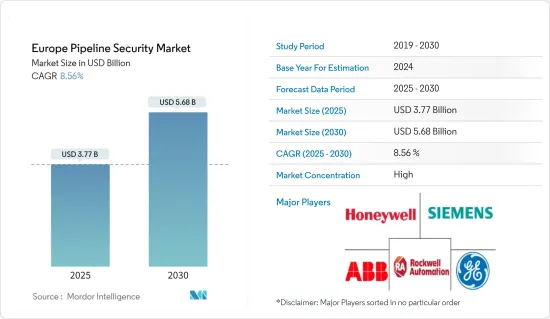

欧州のパイプラインセキュリティ市場規模は、2025年に37億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは8.56%で、2030年には56億8,000万米ドルに達すると予測されます。

主要ハイライト

- パイプラインシステムは、商業活動の主要なソリューションへと進化しています。パイプラインセキュリティ市場は、資源のサステイナブル利用に対する需要と、侵害や少量の輸送製品の盗難の頻度が高まっていることが背景にあります。

- パイプラインシステムは、18世紀から商業活動に利用されてきました。パイプラインは、大量の天然ガス、原油、化学品、水を国家間で輸送するための、最も安全で信頼性が高く、効率的な手段と考えられています。パイプライン設備は、高い重要性と価値を持つ重要インフラであり、それに対する脅威は、人々や組織のニーズを満たすことに大きな影響を与え、環境に害を及ぼす可能性があります。

- 商品輸送のために敷設されたパイプラインは、120カ国にわたり350万キロメートルに及ぶと推定されています。天然ガスと原油のパイプラインは、攻撃を最も受けやすいと予想されます。したがって、石油・ガス会社がパイプラインの安全を確保するために強固なセキュリティインフラを設置するために支出を増やしていることが、市場成長の主要理由となっています。

- 天然ガスの需要は、現在の石炭や石油の需要よりも急速に増加すると予想されています。天然ガスの使用量の増加が、パイプラインセキュリティの需要を高めています。

- さらに、国家主導の強固なサイバースパイキャンペーンは、石油・ガス部門が最も影響を受けており、物理インフラにも影響を及ぼす可能性があります。こうした脆弱性により、産業各社は多額の資金をセキュリティに振り向ける必要に迫られています。

- しかし、パイプラインセキュリティシステムは、施設が多様で点在しているため、高い配備コストとメンテナンス・コストがかかります。このことが、企業のパイプラインセキュリティシステム導入を制限しています。

欧州のパイプラインセキュリティ市場動向

SCADAセグメントが大きなシェアを占める

- モニタリング制御とデータ収集(SCADA)ソフトウェアは、過去10年間で急速な成長を遂げてきました。SCADAシステムは、エンドユーザー産業の従業員が遠隔地からデータを分析し、重要な意思決定を行うのに役立ちます。

- さらに、データを処理し、配信し、ヒューマンマシンインターフェース(HMI)に表示するため、迅速な対応で問題を軽減するのに役立ちます。パイプラインSCADAシステムは、危険や漏れを即座に検知し、保安部隊や保守作業員に効果的にアラームを発します。

- パイプラインSCADAシステムは、地上と地下での活動を検知するためのユニークなソリューションを記載しています。アプリケーションは特に掘削や漏れの検知に使用されます。

- 英国だけでも、石油製品を輸送するためのパイプラインが約2万キロメートルあります。SCADAシステムは、この巨大な石油パイプラインネットワークをモニタリング・制御するために採用されています。石油パイプラインのSCADAには、数百台のRTU(リモート・ターミナル・ユニット)があり、パイプラインを流れる石油の圧力、温度、流量を測定し、パイプラインに沿ったバルブやポンプの状態を変更するフィールド機器に接続されています。

- EIAによると、エネルギー需要は2040年までに68京1,000兆BTUに達すると予想されています。二酸化炭素排出量を削減するため、天然ガスの生産と供給に対する需要が世界的に高まっており、パイプラインセキュリティシステムが必要とされています。

石油・ガスへの投資の増加が市場を牽引

- 石油・ガスへの投資の増加は、この地域のパイプラインセキュリティ市場の成長に大きく貢献しています。欧州連合(EU)は、外部からの天然ガス供給に大きく依存しており、主に高圧天然ガスシステムの技術的な複雑さと、供給国の一部における政治的不安定さが原因で、過去に深刻なガスカットを経験しています。

- EU域内の天然ガス生産量が減少し、ガス需要が増加していることから、特にロシア・ウクライナ間のガス危機の余波を受けて、加盟国間の資源共有を拡大するための国境を越えた送電容量への投資が奨励されています。

- 操業コストを削減する必要性が高まるなか、この地域のパイプラインを運営する企業は、機能の自動化、設備の問題予測、石油・ガスの生産量増加のためにAIの助けを求めています。

- 現在、欧州諸国はアゼルバイジャンの石油の主要消費国のひとつです。イタリアは、この石油を世界市場で販売するアゼルバイジャンの主要貿易相手国です。今年の秋には、欧州もアゼルバイジャンのガスの消費を開始します。

- そのために、全長3,500キロの南部ガス回廊パイプラインが建設され、完成に近づいています。その最後の環であるアドリア海横断パイプラインは、アドリア海のイタリア海岸まで97%が完成しています。TAPは南部ガス回廊の欧州セクションであり、欧州のエネルギー安全保障を強化し、脱炭素化とガス供給の多様化に貢献します。

欧州のパイプラインセキュリティ産業概要

欧州のパイプラインセキュリティ市場の動向は、大手の市場シェアが高いため、緩やかな統合傾向にあります。市場におけるイノベーションは、開発者が適切なソリューションを提供するために産業プロセスをよりよく理解することを必要とし、またエンドユーザーのニーズに合わせて開発やカスタマイズを行う際に、利害関係者間の緊密なコラボレーションを促進します。同市場の著名ベンダーには、Honeywell International,、General Electric Company、ABBなどがあります。

2022年12月、ABBはSensi+アナライザを発売し、パイプラインの運転と保守の簡素化とコスト削減を実現する信頼性の高いソリューションを提供しました。このソリューションは、あらゆる天然ガスの流れに含まれる最大3つの汚染物質(H2S、H2O、CO2)を正確かつリアルタイムで分析できる単一の装置を通じて、より安全で簡単、かつ効率的なパイプラインのモニタリングと運用を可能にすると期待されました。

2022年10月、Blackline Safety Corpは全く新しいG6個人用ガス検知器を発売しました。これはコネクテッドウェアラブルで、迅速な事故対応と、安全性とコンプライアンス管理のより効果的なアプローチを実現し、単一ガス検知に変革をもたらします。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 石油・ガス会社の支出増加

- 世界の天然ガス需要の増加

- SCADAシステムに対する要求の高まり

- 市場抑制要因

- 施設の分散

- 高い導入コストとメンテナンスコスト

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の産業への影響評価

第5章 市場セグメンテーション

- 製品別

- 天然ガス

- 原油

- 有害液体パイプライン/化学製品

- その他

- 技術ソリューション別

- SCADAシステム

- 境界セキュリティ/侵入者検知システム

- 産業制御システムセキュリティ

- ビデオモニタリングとGISマッピング

- パイプライン・モニタリング

- その他の技術とソリューション

- 国別

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他の欧州

第6章 競合情勢

- 企業プロファイル

- Honeywell International Inc.

- General Electric Company

- ABB Ltd.

- Rockwell Automation, Inc.

- Siemens AG

- Schneider Electric S.E.

- Optasense Ltd.

- Senstar Corporation

- Huawei Technologies USA, Inc.

- ESRI Inc.

- Thales SA

第7章 投資分析

第8章 市場の将来

The Europe Pipeline Security Market size is estimated at USD 3.77 billion in 2025, and is expected to reach USD 5.68 billion by 2030, at a CAGR of 8.56% during the forecast period (2025-2030).

Key Highlights

- Pipeline systems have evolved to become the primary solution for commercial activities. The market for pipeline security has been boosted by the demand for sustainable use of resources and the rising frequency of breaches and theft of small quantities of the product being transported.

- The pipeline system has been used since the 18th century for commercial activities. The pipelines are considered the safest, most reliable, and most efficient means of transporting large quantities of natural gas, crude oil, chemicals, and water across nations. Pipeline installations are critical infrastructure of high importance and value, and a threat to it can significantly affect meeting people's and organizations' needs and harm the environment.

- The pipeline installed for transporting commodities is estimated to span 3.5 million kilometers across 120 countries. Natural gas and crude oil pipelines are expected to be the most vulnerable to attacks. Hence, the oil and gas corporation's increased spending to install robust security infrastructure to ensure the security of the pipelines has been the primary reason for the market's growth.

- Demand for natural gas is anticipated to increase faster than the current demand for coal or oil. The increasing natural gas usage is increasing the demand for pipeline security.

- Additionally, the robust state-sponsored cyber-espionage campaigns are the most affected by the oil and gas sector, which can also affect the physical infrastructure. These vulnerabilities have pushed the industry players to divert significant funds for security.

- However, the high deployment and maintenance cost is incorporated with the pipeline security systems as the facility is diverse and scattered. This factor is restricting companies from pipeline security system adoption.

Europe Pipeline Security Market Trends

SCADA Segment to Hold a Significant Share

- Supervisory Control and Data Acquisition (SCADA) software have experienced rapid growth over the past decade. SCADA system helps the end-user industry employees to analyze the data and make crucial decisions from a remote location.

- It further assists in mitigating the issues with a quick response as it processes, distributes, and displays the data on Human Machine Interface (HMI). Pipeline SCADA systems immediately detect hazards and leaks and effectively alarm security forces or maintenance crews.

- It offers a unique solution for the detection of on and underground activities. The applications are specifically used for the detection of digging and leakage.

- The UK alone has about 20,000 kilometers of pipelines for transporting petroleum products. SCADA systems are employed to monitor and control this massive oil pipeline network. The oil pipeline SCADA has several hundred RTUs (remote terminal units) connected to field instruments that measure pressure, temperature, and rate of flow of the oil flowing through the pipes and change the statuses of valves and pumps along the pipeline.

- According to EIA, the energy demand is expected to reach 681 quadrillions of BTU by 2040. The increasing demand for natural gas production and supply globally to reduce carbon emission demands pipeline security systems.

Increasing investments in oil and gas is driving the market

- The increasing investments in oil and gas significantly contribute to the region's pipeline security market growth. The European Union (EU) is highly dependent on external natural gas supplies and has experienced severe gas cuts in the past, mainly driven by the high-pressure natural gas system's technical complexity and political instability in some of the supplier countries.

- Declining indigenous natural gas production and growing demand for gas in the EU has encouraged investments in cross-border transmission capacity to increase resource-sharing between the member states, particularly in the aftermath of the Russia-Ukraine gas crisis.

- Amidst the growing need to cut operating costs, companies operating through the pipeline in the region seek help from AI to automate functions, predict equipment problems, and increase the output of oil and gas.

- At present, European countries are among the primary consumers of Azerbaijani oil. Italy is Azerbaijan's leading trading partner selling this oil on world markets. In the autumn of this year, Europe will also start consuming Azerbaijani gas.

- For this purpose, a 3,500-kilometer-long Southern Gas Corridor pipeline is being built and is nearing completion. Its last ring, the Trans-Adriatic Pipeline to the Adriatic Sea's Italian shores, is 97 percent completed. TAP is the Southern Gas Corridor's European section, enhancing Europe's energy security and contributing to decarbonization and gas supply diversification.

Europe Pipeline Security Industry Overview

Europe's Pipeline Security market trend is moderately towards consolidation as a significant market share lies with the major market players. Innovation in the market requires the developers to have a better understanding of the industrial process to deliver a suitable solution and also drives close collaboration among the stakeholders during development and customization to suit the end-users' needs. Some prominent vendors in the market include Honeywell International, General Electric Company, ABB Ltd., etc.

In December 2022, ABB launched the Sensi+ analyzer, offering a reliable solution that simplifies and decreases the cost of pipeline operation and maintenance. The solution was expected to enable safer, easier, and more efficient pipeline monitoring and operations through a single device that can analyze up to three contaminants (H2S, H2O, CO2) in any natural gas stream accurately and in real time.

In October 2022 - Blackline Safety Corp launched the all-new G6 personal gas detector, a connected wearable that delivers quick incident reaction time and a more effective approach to managing safety and compliance, to transform single-gas detection.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Spending of Oil and Gas Companies

- 4.2.2 Growing Worldwide Demand for Natural Gas

- 4.2.3 Increasing Requirement of SCADA System

- 4.3 Market Restraints

- 4.3.1 Scattered Facilities

- 4.3.2 High Implementation and Maintenance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of the impact of COVID-19 on the industry

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Natural Gas

- 5.1.2 Crude Oil

- 5.1.3 Hazardous liquid pipelines/ Chemicals

- 5.1.4 Other Products

- 5.2 By Technology and Solution

- 5.2.1 SCADA System

- 5.2.2 Perimeter Security/Intruder Detection System

- 5.2.3 Industrial Control Systems Security

- 5.2.4 Video Surveillance and GIS Mapping

- 5.2.5 Pipeline Monitoring

- 5.2.6 Other Technology and Solutions

- 5.3 By Country

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 Rest of the Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Honeywell International Inc.

- 6.1.2 General Electric Company

- 6.1.3 ABB Ltd.

- 6.1.4 Rockwell Automation, Inc.

- 6.1.5 Siemens AG

- 6.1.6 Schneider Electric S.E.

- 6.1.7 Optasense Ltd.

- 6.1.8 Senstar Corporation

- 6.1.9 Huawei Technologies USA, Inc.

- 6.1.10 ESRI Inc.

- 6.1.11 Thales SA