|

市場調査レポート

商品コード

1938995

欧州の紙包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の紙包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

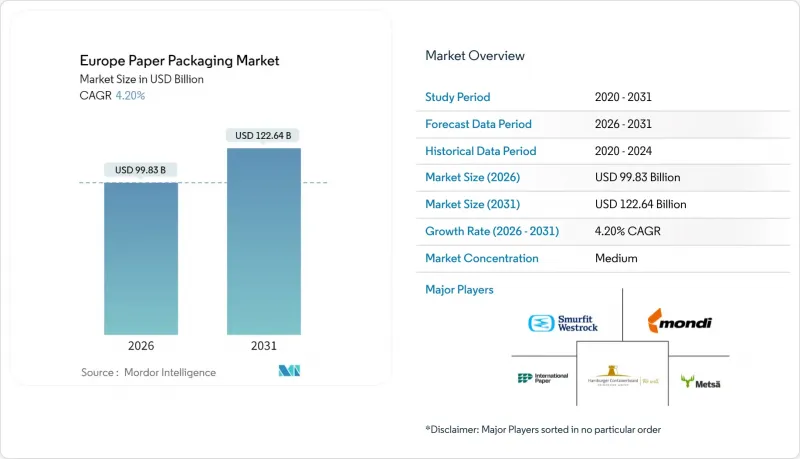

欧州の紙包装市場は、2025年の958億1,000万米ドルから2026年には998億3,000万米ドルへ成長し、2026年から2031年にかけてCAGR4.20%で推移し、2031年までに1,226億4,000万米ドルに達すると予測されております。

本市場の成長は、欧州大陸における循環型経済モデルへの規制転換、小売業者によるカーブサイドリサイクル対応フォーマットの広範な選好、高強度段ボール基材における継続的な技術革新により推進されています。繊維ベースのソリューションは、ISO 14040ライフサイクルアセスメントで確認されたリサイクルの容易さと低炭素強度を兼ね備えるため、外食産業、電子商取引、ミールキット用途においてプラスチックをますます置き換えています。再生材含有板紙の生産能力に対する上流投資、特に北欧の製紙工場における投資は、原材料リスクを軽減すると同時に、供給業者がEU炭素国境調整メカニズムへの対応を可能にします。2024年のスマーフィット社とウェストロック社の合併を含む活発な合併活動は、競合を激化させ垂直統合を加速させ、主要企業がバージン繊維と再生繊維の供給を確保し、輸送コストを最適化し、欧州全域の顧客基盤において持続可能な調達監査を標準化することを可能にします。エネルギー価格変動に伴う短期的な投入コストの上昇圧力が利益率を圧迫しております。しかしながら、オンライン小売の浸透、クイックコマースの利便性、そしてますます厳格化する使い捨てプラスチック禁止措置が相まって包装需要を押し上げているため、下流需要は堅調に推移しております。

欧州紙包装市場の動向と洞察

食品・飲料分野における持続可能かつリサイクル可能な包装材への需要増加

欧州の食品・飲料ブランドは2030年までに100%リサイクル可能な包装目標を公約しており、多層プラスチックよりも繊維素材を優先する調達評価基準が導入されています。主要小売業者は棚出し対応基準を課し、単一素材の繊維トレイを優遇しており、2025年5月にマークス&スペンサーが紙繊維製レディミールトレイを導入した事例がこれを示しています。蒸留酒メーカーや醸造所は、スコッチウイスキー向け90%紙製ボトルなどの主力製品を発表し、紙が環境負荷の低さを体現するという消費者の認識を強化しています。チョコレートバー包装紙を対象としたライフサイクル調査では、あらゆる中間カテゴリーにおいて、紙が配向性ポリプロピレン(OPP)よりも温室効果ガス排出量が少ないことが確認されています。包装加工業者は、2026年8月に施行予定の25ppb PFAS規制に対応するため、コーティング技術サプライヤーとの連携を強化し、製品再設計をブランドオーナーの公開サステナビリティロードマップに整合させます。ISO 14040準拠が国境を越えた中央調達入札で義務化される中、検証済みの製造工程データ(クレードル・トゥ・ゲート)を有する紙ソリューションは、多国籍食品飲料グループ全体で優先サプライヤーとしての地位を獲得します。

電子商取引小包量の急増

欧州のオンライン小売購入は二桁成長を維持し、フルフィルメントセンターにおける箱数と補助緩衝材の急激な増加を促進しています。オムニチャネル食品小売業者や専門小売業者が流通ネットワークを強化した結果、英国の段ボール消費量は2010年から2024年にかけて12.6%増加しました。アマゾンは、2025年1月に欧州事業において100%再生可能な紙製ポーチとボード封筒への切り替えを実施した結果、2018年以降10億枚以上の使い捨てプラスチック製配送袋を削減したと報告しております。モンディ社とCMC Packaging Automation社が共同開発したソリューションなどの自動最適サイズ包装設備は、オンデマンドで箱の寸法を生成し、紙の使用量を最大40%削減すると同時に、トラックの積載効率を向上させます。都市部における食料品クイックコマース市場は、2021年の250億ユーロから2025年までに720億ユーロへ急成長すると予測されており、10分間の配達時間枠内で製品の完全性を保つ寸法最適化された二次包装が求められています。このため、コンバーター企業は、EC事業者が求める大量生産規模とブランディングの柔軟性の両方を満たすため、高速型抜き加工、デジタル印刷によるカスタマイズ、インライン品質管理センサーを優先的に導入しています。

森林破壊への懸念と原材料供給の不安定性

2025年施行のEU森林破壊規制では、地理的位置情報に基づく森林区画までのトレーサビリティが義務付けられ、コンバーターが衛星検証やブロックチェーン台帳を導入する過程で調達コストが3~5%増加します。北欧の製材所では電力コスト急騰や定期的な労働停止による稼働中断が発生し、バージンパルプの供給量も逼迫しているため、買い手はプレミアム価格でのスポット市場調達を余儀なくされています。ビレルード社の生産性向上プログラムは、パルプ価格高騰と原料不足による利益率圧縮を相殺する業界全体の緊急性を浮き彫りにしています。小麦わらやミスカンサスなどの代替繊維は成形繊維製食品容器で注目を集めていますが、繊維長と白度のばらつきが原因で高精細印刷パッケージへの採用は限定的です。イベリア半島やバルト海沿岸の森林への地理的多様化は集中リスクを軽減する一方、物流チェーンを延長し、カーボンフットプリント削減効果を部分的に相殺しています。中期的には、製紙工場は利害関係者への安心感提供と厳格化するデューデリジェンス監査への対応を目的に、閉鎖型水循環システムと森林再生の取り組みを加速させております。

セグメント分析

段ボール箱は2025年の収益の37.92%を占め、フルフィルメント、産業、食料品流通チャネル全体における主力フォーマットとしての地位を強調しています。欧州の段ボール箱向け紙包装市場規模は、EC小包の急増、カスタマイズ印刷の需要、耐圧強度を損なわずに貨物排出量を削減する軽量化の継続的進展により、着実な成長が見込まれます。液体用カートンは2031年までCAGR5.12%と最も高い伸びを示し、代替乳飲料、常温保存可能ジュースライン、多層プラスチック使用削減に向けたブランド主導の取り組みが牽引します。

折り畳み式カートンなどの二次製品は、医薬品ブリスター包装のオーバーラップや、精密な折り目加工と光沢ニスによる陳列効果を重視する高グラフィックのパーソナルケア製品包装において、引き続き重要性を維持します。紙袋や小売用バッグは、使い捨てプラスチック袋の全国的な禁止により勢いを取り戻しています。食料品店では、再利用時の耐久性を高める耐湿性添加剤を配合したクラフト紙製品への切り替えが進んでいます。特殊ニッチ市場(耐引裂性冷凍用袋、成形繊維トレイ、成形パルプ緩衝材)は対応可能量を拡大していますが、段ボールは依然として、地域全体のコンバーター工場稼働率と設備投資の正当性を支える基幹製品です。

2025年には再生紙グレードが55.98%のシェアを獲得。これは厳格な使用済み消費者内容物目標と、国内製紙工場へ供給する堅調な回収システムの結果です。欧州の紙包装市場における再生ライナーのシェアは、CBAM(カーボンボーダー調整メカニズム)により、低炭素再生シートと比較してバージングレードの輸入コストが高騰するため、拡大が見込まれます。高品質のホワイトトップテストライナーは、印刷可能な表面を必要とするディスプレイ対応ケースで支持を得ていますが、ブラウンテストライナーは標準的な輸送用カートンで主流です。

純粋な印刷再現性と優れた剛性が求められる高級化粧品ギフトボックス、医療機器マニュアル、折り畳み式カートンには、依然としてバージンパルプ基材が不可欠です。分散型または押出型バリア層を備えた複合板紙は、水蒸気・油脂抵抗性が重要な中間領域を占めますが、PFAS段階的廃止リスクにより短期的な拡大は抑制されています。サプライチェーンでは、強度と平滑性のバランスを図るため、スカンジナビア産針葉樹クラフトとイベリア産ユーカリ広葉樹を組み合わせたデュアルソーシング戦略が主流となりつつあります。製紙工場は小売業者と循環型パートナーシップを構築し、流通センターから古段ボール(OCC)を回収することで、循環時間を短縮し、食品グレード再生素材に不可欠な原料純度を確保しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 食品・飲料分野における持続可能かつリサイクル可能な包装材への需要増加

- 電子商取引小包取扱量の急激な増加

- EU使い捨てプラスチック指令による繊維代替の加速

- 軽量・高強度段ボール技術の進展

- ミールキットおよびクイックコマースの成長に伴う適正サイズ包装の需要

- EU炭素国境調整メカニズムがリサイクル工場を推進

- 市場抑制要因

- 森林破壊への懸念と原材料供給の変動性

- 柔軟性プラスチックのリサイクル性向上による優位性の縮小

- エネルギー価格の急騰による製紙工場の運営コスト上昇

- バリアコーティング紙におけるPFAS段階的廃止の不確実性

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済要因が市場に与える影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- 折り畳み式カートン

- 段ボール箱

- 紙袋および紙袋類

- 液体用カートン

- その他の紙包装

- 素材タイプ別

- バージンパルプ紙

- 再生紙

- 複合板紙

- エンドユーザー業界別

- 食品

- 飲料

- 医療・医薬品

- パーソナルケア・家庭用品

- 電子商取引・小売業

- タバコ

- その他の最終ユーザー産業

- 包装形態別

- 一次包装

- 二次包装

- 三次包装

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Smurfit WestRock

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Svenska Cellulosa Aktiebolaget SCA

- Metsa Board Oyj

- Mayr-Melnhof Karton AG

- Prinzhorn Holding GmbH

- Progroup AG

- Schumacher Packaging GmbH

- Klingele Papierwerke GmbH & Co. KG

- Graphic Packaging Holding Company

- RAJA Groupe

- VPK Packaging Group NV

- RDM Group(Reno De Medici S.p.A.)

- Lucart S.p.A.

- Essity AB

- Palm GmbH & Co. KG