石油・ガス産業用ガスコンプレッサ:市場シェア分析、産業動向、成長予測(2025~2030年)

Oil And Gas Industry Gas Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1637776

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

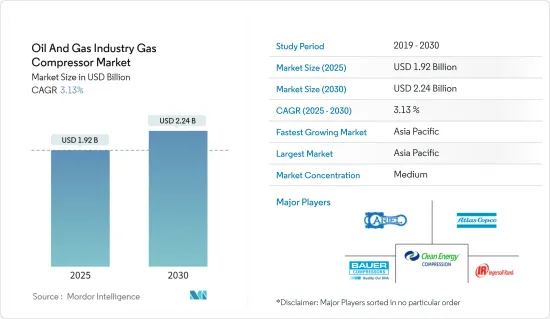

石油・ガス産業用ガスコンプレッサ市場規模は2025年に19億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.13%で、2030年には22億4,000万米ドルに達すると予測されます。

主要ハイライト

- 長期的には、様々な用途での天然ガス消費量の伸びが市場を大きく牽引しており、ガス生産・供給プロジェクトの増加や、現在のシナリオにおける妥当な天然ガス価格が上流部門に好影響を与えています。

- 一方、エネルギー部門における再生可能エネルギーの普及拡大は、天然ガス消費に厳しい競合をもたらし、その結果、多くの用途におけるガスコンプレッサ展開の成長を妨げています。

- 天然ガスの確認埋蔵量の増加、特に最近の画像にある沖合ガス田は、ガスコンプレッサ市場に大きな機会をもたらしています。ごく最近、ロシアのグループであるLukoilがメキシコ沖で発見した石油・ガス田がその一例です。今後新たに生産される油田は、ギャザリングライン用のガスコンプレッサの配備拡大につながると考えられます。

石油・ガスコンプレッサ市場動向

中流部門が市場を独占する見込み

- 石油・ガス産業の中流で使用されるガスコンプレッサは、ガス送電パイプラインネットワーク内か、圧縮ガス貯蔵ユニットのどちらかに配備されます。パイプライン内を流れるガスは、流速とパイプの長さに応じて増加する圧力損失を受けます。そのため、50~100マイルごとに、ガスを再圧縮して圧力損失を補うためのコンプレッサ・ステーションが必要となります。

- 天然ガスの消費量は過去10年間、継続的に増加傾向を示しており、2022年の消費量は約3兆9,413億立方メートルです。多くの国々で政府がよりクリーンなエネルギー生成方法を推進しているため、需要は今後数年間で拡大すると予想されます。今後数年間で、多くのパイプラインやLNGプロジェクトが、多くの中流企業の達成済みプロジェクトリストに追加されようとしています。

- 例えば、アデルフィア・ゲートウェイプロジェクトは、米国連邦エネルギー規制委員会(FERC)から第2期プロジェクトの建設承認を受けました。このプロジェクトには、既存の84マイルの石油パイプラインを、フィラデルフィア地域で配給するためのガス供給パイプラインに転換することが含まれています。開発元のAdelphia Gateway LLCは、2023年末までにパイプラインから最初のガスを供給できる見込みです。

- さらに2023年2月、インドの国営炭化水素大手である石油・天然ガス公社は、同社の主要な西海岸油田からの生産にとって重要なプロジェクトである、大がかりなパイプライン交換プロジェクトを開始しました。この4億4,600万米ドルのプロジェクトは、西海岸沿いの4万平方キロメートルに及ぶONGCの油田からの石油・ガスの安定供給を保証するものです。石油・ガス産業においてコンプレッサは、天然ガスの圧力を高め、生産現場からの天然ガス輸送を可能にするという重要な役割を担っているため、このようなプロジェクトは、ひいては産業全体におけるコンプレッサの利用を促進することになります。

- こうした開発は、予測期間中、石油・ガス産業のガスコンプレッサ市場にプラスの影響を与えることは必至です。

アジア太平洋が市場成長を支配する見込み

- アジア太平洋は、輸送と産業部門での消費の増加により、近い将来、ガス需要の増加分の半分を占める可能性があります。発電産業やその他の用途の天然ガス需要に対応するため、この地域では主にインドや中国などの国々でパイプライン網の拡大が見られます。

- 中国のLNGとパイプラインによる天然ガスの輸入は2022年に記録的な水準に達し、LNGの輸入量は過去10年間で16.6%以上増加し、パイプラインによる月間輸入は400万トンのピークレベルに近づきました。輸入の急増は、国内のパイプラインインフラの拡張につながります。さらに、インドは2023年までに3万4,384kmの新規パイプラインを稼働させると予想されています。

- 2023年3月、Aramcoと合弁パートナーのPanjin Xincheng Industrial GroupとNORINCO Groupは、中国北東部で大規模な統合製油所と石油化学コンプレックスの建設を開始する計画を発表しました。このコンプレックスは、Nissan30万バレルの製油所と、年産165万トンのエチレンと200万トンのパラキシレンを生産する石油化学プラントを併せ持つ予定です。建設は、プロジェクトが行政認可を確保した後、2023年第2四半期に開始される予定です。2026年までにフル稼働する予定です。

- また、CNG給油所のネットワークが急速に拡大していることも、アジア太平洋におけるガスコンプレッサ市場の発展につながっています。例えば、インド政府は2023年4月、2030年までに全国に約1万7,700のCNGステーションを設置する目標を定めたと発表しました。

- このような発展により、ガスコンプレッサ市場は調査期間中、アジア太平洋で最も繁栄すると予想されます。

石油・ガスコンプレッサ産業概要

石油・ガス産業のガスコンプレッサ市場は半固体化しています。主要企業(順不同)には、Atlas Copco AB、Ariel Corporation、Bauer Compressor Inc.、Clean Energy Fuels Corp.、Ingersoll Rand PLCなどがあります。

Atlas Copco ABは、研究開発への注力、市場開発の拡大、業務効率の向上、より優れた価値を提供するサステイナブル新製品やソリューションの開発、エネルギー効率の改善など、多くの戦略を採用しています。一例として、Atlas Copcoは2023年2月に次世代GAとGA+固定速度スマート産業用エアコンプレッサを発表しました。このような技術革新は、多様な製品ポートフォリオにより、産業用顧客の変化するニーズによりよく対応することを可能にします。これらの新しいタイプのコンプレッサは、天然ガス処理や水素製造などのクリーンエネルギー用途にも使用できます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 様々な用途での天然ガス消費の伸び

- 抑制要因

- エネルギーセグメントにおける再生可能エネルギーの普及拡大

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- レシプロ

- スクリュー

- 用途

- 上流

- 下流

- 中流

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- スペイン

- 英国

- その他の欧州

- アジア太平洋

- 中国

- インド

- マレーシア

- インドネシア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Ariel Corporation

- Atlas Corporation AB

- Bauer Compressors Inc.

- Burckhardt Compression Holding AG

- Clean Energy Fuels Corp.

- General Electric Company

- HMS Group

- Howden Group Ltd

- Ingersoll Rand PLC

- Siemens AG

第7章 市場機会と今後の動向

- 天然ガス確認埋蔵量の増加、特にオフショアガス田の増加

目次

The Oil And Gas Industry Gas Compressor Market size is estimated at USD 1.92 billion in 2025, and is expected to reach USD 2.24 billion by 2030, at a CAGR of 3.13% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the market is largely driven by the growth in natural gas consumption for various applications, which has led to more gas production and transmission projects and reasonable natural gas prices in the current scenario, which has a positive impact on the upstream sector.

- On the other hand, the growing penetration of renewables in the energy sector offers stiff competition to natural gas consumption and thus impedes the growth of gas compressor deployment in numerous applications.

- Nevertheless, the increase in natural gas proved reserves, particularly offshore gas fields in the recent picture, places a tremendous opportunity for the gas compressor market. The very recent Russian group's Lukoil's oil and gas field discovery off the coast of Mexico is an example of the same. The new upcoming producing fields will lead to a greater deployment of gas compressors for gathering lines.

Oil and Gas Compressor Market Trends

Midstream Sector Expected to Dominate the Market

- The gas compressors used in the midstream oil and gas industry are deployed either within the gas transmission pipeline network or at the compressed gas storage units. Gas flowing in pipelines suffers from pressure losses that increase with flow velocity and the length of the pipe. Therefore, every 50 to 100 miles, a compressor station is necessary to recompress the gas and compensate for the pressure losses.

- Natural gas consumption continuously showed an advancing trend over the last 10 years, with around 3941.3 billion cubic meters of consumption in 2022. The demand is expected to grow in the coming years due to the government's push for cleaner methods of energy generation in many countries. A number of pipeline and LNG projects are about to be added to the list of accomplished projects of many midstream companies in the coming years.

- For instance, the Adelphia Gateway Project received approval for the construction of the second phase of the project from the Federal Energy Regulatory Commission (FERC), United States. The project includes the conversion of an existing 84-mile oil pipeline to a gas supply pipeline for distribution in the Philadelphia region. The developer, Adelphia Gateway LLC, is expected to be able to supply the first gas from the pipeline by the end of 2023.

- Furthermore, in February 2023, Oil and Natural Gas Corporation, India's state-owned hydrocarbon giant, initiated a big-buck pipeline replacement project, a crucial project for the company's production from key west coast fields. The USD 446 million project will ensure a stable supply of oil and gas from ONGC wells covering an area of 40,000 square kilometers along the western coast. Since compressors play a crucial role in the oil and gas industry in increasing the pressure of natural gas and allowing natural gas transportation from the production site, this kind of project will, in turn, promote the usage of compressors across the industry.

- Such developments will inevitably have a positive impact on the gas compressor market in the oil and gas industry during the forecast period.

Asia-Pacific Expected to Dominate Market Growth

- Asia-Pacific can account for half of the incremental gas demand in the near future due to increased consumption in the transport and industrial sectors. To serve the natural gas demand for the power generation industry and other applications, the region has witnessed an expansion in the pipeline network, mainly in countries like India and China.

- China's LNG and pipeline imports of natural gas reached record levels in 2022, with an increment of more than 16.6% in LNG imports during the last decade, whereas the gas pipeline monthly imports approached a peak level of 4 million metric tons. The surge in imports will lead to an expansion of the supporting pipeline infrastructure in the country. Moreover, India is expected to bring 34,384 km of new pipelines online by 2023.

- In March 2023, Aramco and joint venture partners Panjin Xincheng Industrial Group and NORINCO Group announced plans to start the construction of a significant integrated refinery and petrochemical complex in northeast China. The complex is going to have combination of a 300,000 barrels per day refinery and a petrochemical plant with an annual production capacity of 1.65 million tons of ethylene and 2 million metric tons of paraxylene. Construction is expected to start in the second quarter of 2023 after the project has secured administrative approvals. It is expected to be fully operational by 2026.

- Also, the rapidly growing network of CNG fueling stations has led to the development of the gas compressor market in the Asia-Pacific region. For example, in April 2023, the government of India announced the target has been fixed to establish around 17,700 CNG stations across the country by 2030.

- Owing to such developments, the gas compressor market is expected to flourish to the greatest extent in the Asia-Pacific region during the study period.

Oil and Gas Compressor Industry Overview

The oil and gas industry's gas compressor market is semi-consolidated. Some of the major companies (in no particular order) include Atlas Copco AB, Ariel Corporation, Bauer Compressor Inc., Clean Energy Fuels Corp., and Ingersoll Rand PLC, among others.

Atlas Copco AB has adopted many strategies like focus on research and development, increase market coverage, increase operational efficiency, develop new sustainable products and solutions offering better value and improved energy efficiency. As an example, in February 2023, the company launched its next generation GA and GA+fixed speed smart industrial air compressors,. Such technological innovations would enable the company to better respond to the changing needs of the industrial customers with diversified product portfolio. These new type of compressors can also be used for clean energy applications like natural gas processing, and hydrogen production.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growth in Natural Gas Consumption for Various Applications

- 4.5.2 Restraints

- 4.5.2.1 Growing Penetration of Renewables in the Energy Sector

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Reciprocating

- 5.1.2 Screw

- 5.2 Application

- 5.2.1 Upstream

- 5.2.2 Downstream

- 5.2.3 Midstream

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 Spain

- 5.3.2.4 United Kingdom

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Malaysia

- 5.3.3.4 Indonesia

- 5.3.3.5 Rest of Asia-Pacifc

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirated

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Ariel Corporation

- 6.3.2 Atlas Corporation AB

- 6.3.3 Bauer Compressors Inc.

- 6.3.4 Burckhardt Compression Holding AG

- 6.3.5 Clean Energy Fuels Corp.

- 6.3.6 General Electric Company

- 6.3.7 HMS Group

- 6.3.8 Howden Group Ltd

- 6.3.9 Ingersoll Rand PLC

- 6.3.10 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Natural Gas Proved Reserves, Particularly Offshore Gas Fields

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日