メガデータセンター:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Mega Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1637740

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

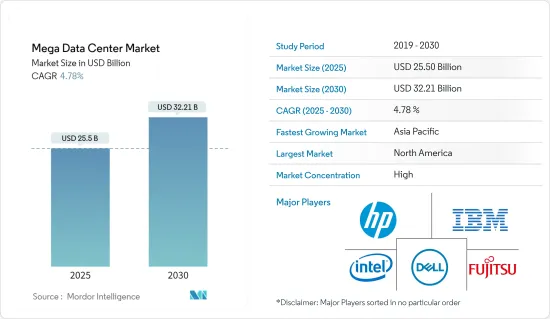

メガデータセンターの市場規模は2025年に255億米ドルと推定され、予測期間(2025-2030年)のCAGRは4.78%で、2030年には322億1,000万米ドルに達すると予測されます。

主なハイライト

- データセンター業界は、仮想化が長年にわたって牽引してきました。企業は、ITオペレーションをより少ない、より利用率の高いマシンに集中させることで、インフラを削減しようとしてきました。このプロセスにより、データセンター全般に対する見方が広まった。複数のデータセンターを運営する企業は、複雑さとコストを削減するために、より少数の大規模な実装に設備を集中させることを選択できます。

- 立地によっては、メガデータセンターの数を少なくすることで、税制上の優遇措置、低いエネルギー価格、気候、代替エネルギー源の利用可能性など、特定の地域のメリットを享受することができます。このように、メガデータセンターはコストを最小化し、利益を最大化しようとする試みから生まれます。

- ソフトウェア主導で、業界に関連し、適切にセットアップされたメガ・データ・センターを選択するメリットは、現在と比べてIT管理コストが低いこと、また、ローカル・データ・センターのスピードと帯域幅で膨大な量のインターネットや産業用インターネット・データにアクセスできることです。この能力は、世界中でIT支出に拍車をかける可能性が高いです。早期導入企業は、全体的なビジネス・コストを削減し、収益を増加させるための新しいIT技術に投資する大きな機会を得ることになるからです。

- クラウドやコロケーション・サービスの増加、それに伴うコストメリット、スケールメリットの向上などの要因が、メガデータセンター市場を牽引しています。マイクロソフト、グーグル、アマゾン・ウェブ・サービス(AWS)、フェイスブックのデータセンターは、それ自体が別格です。彼らは、すべてのノードに複数の経路があるため、特定のデータセンター内のどのノードにもアクセスできるファブリックを作るために、光ファイバーの速度で動作する完全自動の自己修復型ネットワーク化されたメガデータセンターを機能させなければならないです。

- しかし、初期投資が高く、リソースの利用可能性が低いことが、この市場の課題となっています。このような課題にもかかわらず、さまざまな組織がメガデータセンターをすでに導入しているか、導入を開始しています。

メガデータセンター市場の動向

銀行・金融セクターにおけるデータセンター需要の高まり

- 銀行・金融セクターは最大のデータ発生源の1つであり、運用コストを調整するためのデータセンターの必要性が主要な促進要因となっています。金融・銀行機構は、顧客記録、従業員管理、取引、リモートバンキング、テレバンキング、自己照会などの電子バンキング・サービスの保存にデータセンターを利用しており、これらのサービスを機能させるためにはデータセンターが必要です。

- インフラとしてのデータセンターは、金融の将来を担うものと考えられています。多くの金融機関がプライベート・クラウド・システムを構築し、大規模なネットワーク、ストレージ、サーバー容量を収容して、リテール金融センター、ATM、アクティブなオンライン口座をサポートしています。

- 多くの銀行が自前のデータセンターを維持しているが、銀行の収益が変動しているため、動向が変わりつつあることが確認されています。また、データセンターの維持には、適切な冷却、セキュリティ、電力設備が必要なため、IT、不動産、運用にかかるコストがかさみます。これは予測期間中、BFSI業界にとって課題となり得る。

アジア太平洋地域の需要拡大が市場を牽引

- 中国全土で高密度で冗長化された施設に対する需要が高まっていることが、同国のデータセンターの設計と開発に変化をもたらしています。中国のインターネットユーザー数は人口100人当たり50人で、多くの開発余地があることを示しており、接続エコシステムは73のコロケーションデータセンター、52のクラウドサービスプロバイダー、0のネットワークファブリックで構成されています。

- しかし、中国では電力、スペース、IPトランジットのすべてにコストがかかり、データセンターの維持が困難であることが強調されています。同様に、インドではデジタル経済がGDPの9.5%を占めています。デジタル経済には255億1,800万米ドルの固定電話契約と10億1,105万4,000の携帯電話契約が含まれ、データセンターの開発余地が大きいことを示しています。

- さらに、インドの多くの組織、特にBFSIセクターは、規制やセキュリティ上の理由から、国外にあるデータセンターでデータをホスティングすることを禁じられています。その結果、データセンター・プロバイダーはインド国内にデータセンターを設置するようになり、インドでメガデータセンター施設が増加していることを示しています。

メガデータセンター業界の概要

メガデータセンター市場は、初期投資が高く、リソースの供給が少ないため、集中度が高く、これがこの市場の課題となっています。同市場の主要企業には、シスコシステムズ、デル・ソフトウェア、富士通、ヒューレット・パッカード・エンタープライズなどがあります。市場の最近の動向としては、以下のようなものがある:

2022年9月、マイクロソフトはカタールに新しいデータセンター地域を開設し、同国でエンタープライズグレードのサービスを提供する初のハイパースケールクラウドプロバイダーとなった。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場促進要因と市場抑制要因のイントロダクション

- 市場促進要因

- データセンター統合需要の高まり

- 銀行・金融セクターにおけるデータセンター需要の高まり

- 市場抑制要因

- 高い投資と設置コスト

- 技術スナップショット

第5章 市場セグメンテーション

- ソリューション別

- ストレージ

- ネットワーク

- サーバー

- セキュリティ

- その他のソリューション

- エンドユーザー別

- BFSI

- 通信・IT

- 政府機関

- メディアおよびエンターテイメント

- その他エンドユーザー

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- Dell Software Inc.

- Fujitsu Ltd

- Hewlett-Packard Enterprise

- IBM Corporation

- Intel Corporation

- Juniper Networks Inc.

- Verizon Wireless

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Mega Data Center Market size is estimated at USD 25.50 billion in 2025, and is expected to reach USD 32.21 billion by 2030, at a CAGR of 4.78% during the forecast period (2025-2030).

Key Highlights

- Virtualization has driven the data center industry over the years. Companies have sought to reduce infrastructure by focusing IT operations on fewer, more highly utilized machines. This process has led to a wider view of data centers in general. Companies operating multiple data centers can choose to focus their facilities on fewer and larger implementations to decrease complexity and costs.

- Implementing fewer mega data centers, depending on their locations, can allow a company to enjoy advantages of certain local benefits, such as tax incentives, low energy prices, climate, or availability of alternative energy sources. Thus, mega data centers result from attempts to minimize cost and maximize profit.

- The merits of choosing a software-led, industry-relevant, and adequately set-up mega data center are lower costs of IT management compared to the present, as well as the ability to access a vast amount of internet and industrial Internet data at local data center speed and bandwidth. This capability is likely to spur IT spending worldwide, as early adopters will have substantial opportunities to invest in new IT techniques to reduce overall business costs and increase revenues.

- Factors including increasing cloud and colocation services, associated cost benefits, and improved economies of scale drive the market for mega data centers. Microsoft, Google, Amazon Web Services (AWS), and Facebook data centers are in a class by themselves. They have to function fully automatic, self-healing, networked mega data centers that operate at fiber optic speeds to make a fabric that can access any node in any particular data center, as there are multiple pathways to every node.

- However, higher initial investments and low resource availability are some factors presenting challenges to this market. Despite such challenges, various organizations have already adopted or are initiating the adoption of mega data centers.

Mega Data Centers Market Trends

Rising Demand of Data Centers in Banking and Finance Sectors

- The banking and finance sector is one of the largest generators of data, and the need for a data center to regulate the cost of operations is a primary driver. Finance and banking structures use data centers to store customer records, employee management, transactions, and electronic banking services, such as remote banking, telebanking, and self-inquiry, which need data centers to function.

- Data centers, as infrastructure, are believed to be the future of finance. Many institutions have created private cloud systems to accommodate massive network, storage, and server capacities to support their retail financial centers, ATMs, and active online accounts.

- Many banks maintain their own data centers, but it has been observed that the trend is changing due to fluctuations in the banks' profits. Also, maintaining a data center is cumbersome, owing to the cost drain on IT, real estate, and operations, as it requires proper cooling, security, and power facilities. This can act as a challenge for the BFSI industry during the forecast period.

Growing Demand from Asia-Pacific to Drive the Market

- The growing demand for high-density, redundant facilities throughout China is precipitating a shift in the design and development of the country's data centers. China has 50 internet users per 100 population, indicating scope for a lot of development, and the connectivity ecosystem comprises 73 colocation data centers, 52 cloud service providers, and 0 network fabrics.

- However, power, space, and IP transit all cost more in China, emphasizing the difficulties in maintaining a data center. Similarly, in India, the digital economy contributes 9.5% of the GDP. The digital economy includes USD 25,518 million fixed-line telephone subscriptions and 1,011.054 million mobile telephone subscriptions, indicating a lot of scope for the development of data centers.

- Moreover, owing to regulatory and security reasons, a number of organizations in India, especially from the BFSI sector, are not allowed to host their data in a data center that is out of the country. As a result, the data center providers are setting up local data centers in India, indicating the growing mega data center facilities in India.

Mega Data Centers Industry Overview

The mega data center market is highly concentrated due to higher initial investments and low availability of resources, which present challenges to this market. Some of the key players in the market are Cisco Systems Inc., Dell Software Inc., Fujitsu Ltd, and Hewlett-Packard Enterprise. Some recent developments in the market include:

In September 2022, Microsoft launched its new data center region in Qatar, becoming the first hyper-scale cloud provider to offer enterprise-grade services in the nation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Introduction to Market Drivers and Restraints

- 4.4 Market Drivers

- 4.4.1 Increasing Demand for Data Center Consolidation

- 4.4.2 Rising Demand of Data Centers in Banking and Finance Sectors

- 4.5 Market Restraints

- 4.5.1 High Investment and Installation Costs

- 4.6 Technology Snapshot

5 MARKET SEGMENTATION

- 5.1 By Solution

- 5.1.1 Storage

- 5.1.2 Networking

- 5.1.3 Server

- 5.1.4 Security

- 5.1.5 Other Solutions

- 5.2 By End-user

- 5.2.1 BFSI

- 5.2.2 Telecom and IT

- 5.2.3 Government

- 5.2.4 Media and Entertainment

- 5.2.5 Other End-users

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems Inc.

- 6.1.2 Dell Software Inc.

- 6.1.3 Fujitsu Ltd

- 6.1.4 Hewlett-Packard Enterprise

- 6.1.5 IBM Corporation

- 6.1.6 Intel Corporation

- 6.1.7 Juniper Networks Inc.

- 6.1.8 Verizon Wireless

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日