|

市場調査レポート

商品コード

1637727

高電圧開閉装置:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)High Voltage Switchgear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 高電圧開閉装置:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

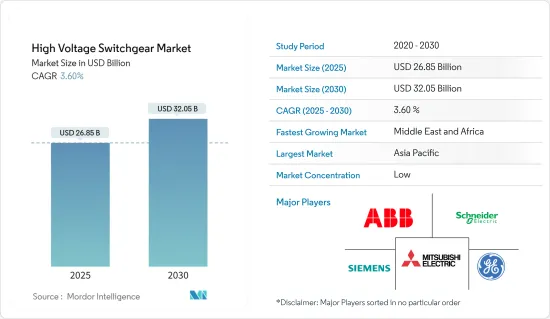

高電圧開閉装置市場規模は2025年に268億5,000万米ドル、2030年には320億5,000万米ドルに達すると推定・予測、予測期間(2025~2030年)のCAGRは3.6%。

主要ハイライト

- 中期的には、再生可能エネルギーへの適応が進み、送電網のアップグレードや近代化活動が活発化していることが、予測期間中の市場調査を促進するとみられます。

- 一方、初期設備投資が高額であることが、予測期間中の市場成長の妨げになると予想されます。

- 運輸部門の電化が進んでいることから、高電圧開閉装置市場に大きなビジネス機会が生まれると期待されています。

- アジア太平洋は、エネルギー需要の増加とインフラ開発活動の活発化により、同市場の主要地域になると予想されます。

高電圧開閉装置市場の動向

ガス絶縁開閉装置が著しい成長を遂げる

- ガス絶縁開閉装置は、都市化が進みインフラに利用可能な土地が不足する中、非常にコンパクトでスペース効率が高いです。

- ガス絶縁開閉装置は設置面積が小さいという極めて重要な利点があり、公益事業企業は人口密集地でのスペース利用を最適化できます。この戦略は、エネルギー容量の拡大と物理的なインフラ要件の最小化との間でバランスを取るという最新の配電システムの必須要件に適合しています。

- ガス絶縁開閉装置技術は、環境への影響を最小限に抑える固有の能力を備えており、その優位性を大幅に高めています。ガス絶縁開閉装置に絶縁ガスを使用することで、温室効果ガスやその他の汚染物質の放出が緩和されるため、世界の持続可能性の義務付けに共鳴します。

- さらに、ガス絶縁開閉装置の優れた動作信頼性と安全性が、その優位性を実証しています。カプセル化された設計は、重要な部品を外部要因から保護し、環境上の危険や潜在的な人為的干渉から保護します。

- 電力需要の増加により、さまざまな国がエネルギー需要を満たすために近隣諸国からエネルギーを輸入しています。この輸入に伴い、新しいトランスミッションと配電ネットワークが開発され、この地域での開閉装置の需要が増加しています。

- 例えば、シンガポール政府は2022年6月、増大するエネルギー需要に対応するため、近隣諸国との多国間電力取引を通じて、再生可能エネルギーによる最初の電力輸入を開始しました。ラオス・タイ・マレーシア・シンガポール電力統合プロジェクト(LTMS-PIP)は、既存の送配電システムをアップグレードし、最大100メガワット(MW)の再生可能水力電力をラオスからタイ、マレーシアを経由してシンガポールに輸入することを可能にするものです。

- Energy Institute Statistical Review of World Energy 2023によると、世界の電力生産量は2022~2021年の間に2.3%増加しました。2022年の世界の累積電力生産量は、2021年の28520.2テラワット時に対し2万9,165.1テラワット時を記録し、過去10年間の電力生産量は2012~2022年にかけて毎年2.5%増加しました。

- したがって、予測期間中はガス絶縁開閉装置市場セグメントが高電圧開閉装置市場を独占すると予想されます。

アジア太平洋が市場を独占する

- 高電圧開閉装置市場におけるアジア太平洋の急成長は、多面的な市場力学と戦略的要請の集大成として現れています。この地域のエネルギー消費パターンに見られる戦略的要請が、予想される優位性を立証しています。急速な都市化、工業の拡大、アジア太平洋経済圏における電力需要の増大が、高電圧開閉装置の必要性を高めています。

- アジア太平洋の急成長する経済は、増大する送電要件を満たす効率的な高電圧ケーブル網を含む、強固なエネルギーインフラを必要としています。この戦略的な適合は、エネルギー・アクセスの格差に対処し、この地域の世界のエネルギー大国としての役割を促進します。

- さらに、規制による支援と市場インセンティブが、この地域のリーダーとしての地位を強固なものにしています。再生可能エネルギーの統合と排出削減を提唱する政府のイニシアチブは、有利な施策枠組みと財政的インセンティブと相まって、高電圧開閉装置の採用を促進しました。

- 例えば、2023年7月、ROSATOMの風力発電部門であるNovaWindとAn Xuan Energyの代表者との間で、ベトナムにおける風力発電所の開発に関する協力協定が締結されました。この協定は、ベトナムの北西部に位置するソンラ省に128MWの風力発電所を建設するためのパートナーシップ概要を示しています。

- この地域の技術革新のための強固なエコシステムは、研究開発イニシアチブの普及と相まって、高電圧開閉装置の加速的な進歩をもたらす態勢を整えています。現地での技術革新が優れたシステム効率、信頼性の向上、コスト競合を生むことから、アジア太平洋は最先端技術を育む坩堝として浮上しています。

- したがって、上記の点から、予測期間中、アジア太平洋が市場を独占すると予想されます。

高電圧開閉装置産業概要

高電圧開閉装置市場は適度にセグメント化されています。この市場の主要企業(順不同)には、ABB Ltd、Schneider Electric SE、General Electric Company、Toshiba International Corporation、Mitsubishi Electric Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 送電網の近代化

- 再生可能エネルギーの統合

- 抑制要因

- 初期コストの高さ

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- タイプ

- 空気絶縁

- ガス絶縁

- その他

- 市場分析:地域別2028年までの市場規模と需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ABB Ltd

- Schneider Electric SE

- General Electric Company

- Toshiba International Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Larson & Turbo Limited

- Bharat Heavy Electricals Limited

第7章 市場機会と今後の動向

- 輸送部門の電化

目次

Product Code: 46388

The High Voltage Switchgear Market size is estimated at USD 26.85 billion in 2025, and is expected to reach USD 32.05 billion by 2030, at a CAGR of 3.6% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adaption of renewable energies coupled with increasing grid upgradation and modernization activities are expected to drive the market studied during the forecast period.

- On the other hand, high initial capital investments are expected to hinder the growth of the market studied during the forecast period.

- Nevertheless, the ongoing electrification of the transportation sector is expected to create huge opportunities for the high-voltage switchgear market.

- Asia-Pacific is expected to be a dominant region for the market studied due to the increasing demand for energy coupled with increasing infrastructure development activities in the region.

High Voltage Switchgear Market Trends

Gas-insulated Switchgear to Witness a Significant Growth

- The gas-insulated switchgear is exceptionally compact and space-efficient as urbanization intensifies and available land for infrastructure becomes scarce.

- Gas-insulated switchgear's reduced footprint offers a pivotal advantage, allowing utilities to optimize space utilization in densely populated areas. This strategy fits in with the imperative of modern power distribution systems to strike a balance between expanding energy capacity and minimal physical infrastructure requirements.

- Gas-insulated switchgear technologies' inherent capability to minimize environmental impact significantly bolsters its prominence. Using insulating gases in gas-insulated switchgear mitigates the release of greenhouse gases and other pollutants, thus resonating with global sustainability mandates.

- Moreover, gas-insulated switch gears' superior operational reliability and safety features substantiate its anticipated dominance. The encapsulated design shields critical components from external factors, safeguarding them from environmental hazards and potential human interference.

- The increasing demand for electricity has allowed various countries to import energy from neighboring countries to meet their energy demands. With this import, new transmission and distribution networks are being developed, increasing the demand for switchgear in the region.

- For instance, in June 2022, to address the country's increasing energy demand, Singapore's government initiated its initial renewable energy electricity import through a multilateral power trade with neighboring countries. The Lao PDR-Thailand-Malaysia-Singapore Power Integration Project (LTMS-PIP) would upgrade its existing transmission and distribution systems to enable the importation of up to 100 megawatts (MW) of renewable hydropower from Lao PDR to Singapore through Thailand and Malaysia.

- According to the Energy Institute Statistical Review of World Energy 2023, global electricity production increased by 2.3% between 2022 and 2021. In 2022, the cumulative electricity production globally was recorded at 29165.1 terawatt hours compared to 28520.2 terawatt hours in 2021, while electricity production in the last decade grew by 2.5% annually between 2012 and 2022.

- Therefore, the gas-insulated switchgear market segment is expected to dominate the high-voltage switchgear market during the forecast period.

Asia-Pacific to Dominate the Market

- The burgeoning dominance of the Asia-Pacific region in the high-voltage switchgear market emerges as a culmination of multifaceted market dynamics and strategic imperatives. Strategic imperatives routed in regional energy consumption patterns substantiate the anticipated dominance. Rapid urbanization, industrial expansion, and growing electricity demand within the Asia-Pacific economies collectively amplify the need for high-voltage switchgear.

- Asia Pacific's burgeoning economies necessitate robust energy infrastructure, including efficient high-voltage cable networks to meet escalating power transmission requirements. This strategic fit addresses energy access disparities and catalyzes the region's role as a global energy powerhouse.

- Furthermore, regulatory support and market incentives fortify the region's leadership position. Government initiatives advocating for renewable energy integration and emissions reduction coupled with favorable policy frameworks and financial incentives catalyzed the adoption of high-voltage switchgear.

- For instance, in July 2023, a collaboration agreement was signed between NovaWind, the wind power arm of ROSATOM, and An Xuan Energy representatives to develop a wind farm in Vietnam. The agreement outlines a partnership to construct a wind farm with a 128 MW capacity in the Son La Province, located in the northwestern region of Vietnam.

- The region's robust ecosystem for technological innovation, coupled with the proliferation of research and development initiatives, is poised to yield accelerated advancements in high-voltage switchgear. As local innovation begets superior system efficiency, enhanced reliability, and cost competitiveness, the Asia-Pacific emerges as a crucible for fostering cutting-edge technologies.

- Therefore, due to the abovementioned points, Asia-Pacific is expected to dominate the market studied during the forecast period.

High Voltage Switchgear Industry Overview

The high-voltage switchgear market is moderately fragmented. Some of the key players in this market (in no particular order) include ABB Ltd, Schneider Electric SE, General Electric Company, Toshiba International Corporation, and Mitsubishi Electric Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Grid Modernization

- 4.5.1.2 Renewable Energy Integration

- 4.5.2 Restraints

- 4.5.2.1 High Initial Cost

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Air-insulated

- 5.1.2 Gas-insulated

- 5.1.3 Other Types

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Qatar

- 5.2.5.4 Egypt

- 5.2.5.5 South Africa

- 5.2.5.6 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 Schneider Electric SE

- 6.3.3 General Electric Company

- 6.3.4 Toshiba International Corporation

- 6.3.5 Mitsubishi Electric Corporation

- 6.3.6 Siemens AG

- 6.3.7 Larson & Turbo Limited

- 6.3.8 Bharat Heavy Electricals Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Electrification of Transportation Sector