|

市場調査レポート

商品コード

1636563

欧州の電気自動車(EV)充電設備- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Electric Vehicle (EV) Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の電気自動車(EV)充電設備- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

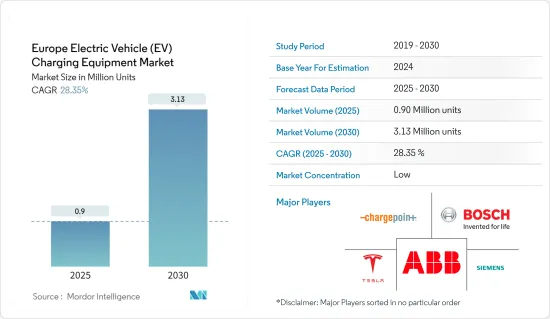

欧州の電気自動車充電設備市場規模は、2025年に90万台と推定され、予測期間(2025~2030年)のCAGRは28.35%で、2030年には313万台に達すると予測されます。

主要ハイライト

- 中期的には、電気自動車の普及拡大や政府のイニシアティブに支えられたEV充電インフラ強化への取り組みなどの要因が、予測期間中のEV充電機器市場を牽引すると予測されます。

- 逆に、充電ステーションの設置に伴う設置費用やメンテナンス費用の高さが、予測期間中の市場成長を阻害する可能性もあります。

- しかし、急成長する欧州市場の包括的なEV充電ネットワークに対する需要は、EV充電機器の技術的進歩と相まって、予測期間中の欧州EV充電機器市場に大きな機会をもたらします。

- 電気自動車の普及を促進する積極的なイニシアチブを持つドイツは、欧州の景観の中で注目すべき成長を遂げようとしています。

欧州の電気自動車(EV)充電機器市場動向

バッテリー電気自動車セグメントが市場を独占

- 一般に電気自動車として知られるバッテリー式電気自動車(BEV)は、電気モーターに電力を供給するために大きなトラクションバッテリーパックを利用します。充電するために、これらの車両は電気自動車供給設備(EVSE)に接続します。

- 完全な電気自動車であるBEVには、通常、内燃機関(ICE)、燃料タンク、排気管がないです。グリッドで充電されたバッテリーパックからエネルギーを得ています。ゼロ・エミッション車であるBEVは、従来のガソリン車に伴う有害なテールパイプ排出ガスを出さないため、大気汚染を軽減することができます。

- 欧州の自動車産業は大きな転換期を迎えており、バッテリー式電気自動車(BEV)の牽引力と人気が高まっています。技術の進歩、政府の後押し、環境意識の高まりに後押しされ、BEVは気候変動と闘い、化石燃料への依存を減らすための実行可能なソリューションとして台頭しつつあります。

- 国際エネルギー機関(IEA)のデータによると、EUにおけるBEV販売台数は2023年に約160万台に達し、2022年の120万台から33%増加しました。さらに、EUにおけるBEVの総在庫台数は約460万台にまで増加しています。BEVの販売台数が急増するにつれ、欧州では充電インフラの需要が高まっている

- さらに、いくつかの欧州政府は、今後数年間でEVの普及を促進する戦略を立てています。例えば、フランス政府は2024年5月、自国の自動車メーカーに対し、10年後までに200万台の電気自動車またはハイブリッド車を生産するという野心的な目標を設定しました。政府との新たな中期協定の一環として、自動車産業は2027年までに80万台の電気自動車販売という中間目標を目指しており、これは2022年の20万台から大幅に急増します。さらに自動車メーカーは、電気自動車(EV)の年間販売台数を2022年の1万6,500台から10万台に引き上げることを目標としています。このような野心的な目標は、同地域におけるEV充電装置の需要を大幅に押し上げる構えです。

- 欧州自動車工業会(ACEA)によると、EUでは2023年に約15万カ所(週平均3,000カ所以下)の公共充電ポイントが設置され、合計で63万カ所以上となる見込みです。これに対して欧州委員会は、2030年までに約350万カ所の充電ポイントを目標に掲げています。これを達成するには、年間約41万カ所(毎週約8,000カ所)の公共充電ポイントを設置する必要があります。

- 逆にACEAは、2030年までに880万箇所の充電ポイントが必要と予測しています。この需要を満たすには、現在の8倍にあたる年間120万台(毎週2万2,000台以上)の充電設備の設置が必要となります。このような野心的な目標は、欧州におけるBEV市場の成長と、それに伴うEV充電設備に対する需要の急増を強調しています。

- 近年、中国の著名な自動車メーカー数社が、欧州での製造・組立工場の設立に関心を示しており、価格競合自動車の販売を拡大し、欧州の自動車メーカーに対抗することを目指しています。例えば、輸出台数で中国トップの奇瑞汽車(Chery Auto)は2024年4月、スペインのEVモーターズ(EV Motors)との合弁で、カタルーニャ地方に欧州初の生産施設を設立すると発表し、2024年後半に生産を開始する予定です。さらに、この10年間に英国に自動車工場を建設する可能性についても協議が進められています。

- 2023年、世界有数のEVメーカーであるBYDは、ハンガリーに初の欧州生産拠点を建設し、3年後に操業を開始する計画を発表しました。この拠点は欧州市場に対応し、バッテリーEVとプラグインハイブリッドの両方を生産します。このような開発は、BEV製造セクターを強化し、EV充電インフラへの需要を高めると予想されます。

- このような動きの中で、BEVセグメントは今後数年間、欧州のEV充電設備市場をリードしていくと考えられます。

著しい成長を遂げるドイツ

- ドイツは、電気自動車(EV)機器とインフラを急速に拡大しており、EV産業に対する国の取り組みが加速していることを反映しています。国際エネルギー機関(IEA)によると、2023年末までに、ドイツは約10万8,000カ所のEV充電ポイントを公的に利用できるようにします。その内訳は、急速充電設備が約2万1,000基、低速充電設備が約8万7,000基です。特に2023年には、1万6,000カ所以上の低速充電ポイントと6,000カ所の急速充電ポイントが追加されました。

- ドイツ政府は野心的な計画を持っており、2030年末までに全国に100万カ所の公共充電ポイントを設置することを目標としています。しかし、2023年後半の時点で、この目標の約11%しか達成されていないです。このギャップを埋めるため、公共EV充電ポイントの大幅な増加が今後数年で予想され、EV充電機器市場の急成長を示唆しています。

- 政府は、公共スペースから住宅や商業施設まで、さまざまな場所でのEV充電設備の設置を積極的に承認しています。この取り組みは、道路を走る電気自動車の増加に対応し、EV充電装置の需要を促進しています。EV充電インフラの拡大はドイツにとって極めて重要であり、航続距離への不安を解消し、アクセシビリティを向上させることで、より多くの消費者の電気自動車への移行を促すことを目的としています。

- 2024年2月、欧州の著名なEV充電会社であるFastnedは、ドイツの高速道路沿いに34の急速充電サイトを設置する認可を受けました。ドイチュラントネッツ」入札の一環であるこのイニシアチブは、EV充電インフラの強化に対するドイツのコミットメントを強調するものです。ファストネッドの動きは、2030年までに欧州全域に1,000カ所の急速充電ステーションを設置するという野心的な目標に向けた前進です。

- ドイツでは、EVインフラを強化し、急増する充電設備需要に対応するための戦略として、自社でEV充電ハブを設置する企業が増えています。こうしたハブは、EVの普及を促進するだけでなく、二酸化炭素排出を抑制し、サステイナブル輸送ソリューションを支持する役割を担っています。

- 2023年11月、Mercedes-Benzはドイツ・マンハイムに初の自社製充電ハブを開設しました。この事業は、10年後までに2,000カ所以上の充電ステーションを設置し、10,000カ所以上の急速充電ポイントを設置するというMercedes-Benzの世界の目標に沿ったものです。

- ドイツはまた、サステイナブル輸送へのコミットメントを強化するため、ガソリンスタンドでのEV充電設備の設置を推進しています。この義務化は、クリーンエネルギー車を促進するだけでなく、より広範な気候変動の課題にも取り組んでいます。

- 2023年9月、ドイツのオラフ・ショルツ首相は、全ガソリンスタンドの80%に、最低150キロワットの急速充電オプションを提供することを義務付ける法律を近々制定すると発表しました。

- このような開発状況を踏まえると、ドイツの電気自動車(EV)充電設備市場は、EV普及率の上昇、旺盛な投資、政府の支援施策や目標に後押しされ、大きな成長が見込まれます。

欧州の電気自動車(EV)充電設備産業概要

欧州の電気自動車(EV)充電設備市場は半分断されています。同市場の主要企業(順不同)には、ABB Ltd、Robert Bosch GmbH、ChargePoint Inc.、Siemens AG、Tesla Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:台)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及と関連投資の拡大

- 政府のイニシアティブに支えられたEV充電インフラ増強への取り組み

- 抑制要因

- 充電ステーション設置に伴う高い設置コストとメンテナンスコスト

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 車種

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

- アプリケーション

- 家庭用充電

- 職場充電

- 公共充電

- 充電タイプ

- AC充電(レベル1とレベル2)

- DC充電

- 地域

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ABB Ltd

- Robert Bosch GmbH

- Delta Electronics Inc.

- Siemens AG

- Tesla Inc.

- ChargePoint Inc.

- Enphase Energy, Inc.

- Powercharge

- Ampure

- Exicom Tele-Systems Ltd

- Schneider Electric SE

- Eaton Corporation

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- EV充電機器の技術進歩

- 新興欧州市場における堅牢なEV充電ネットワークの必要性

目次

Product Code: 50004069

The Europe Electric Vehicle Charging Equipment Market size is estimated at 0.90 million units in 2025, and is expected to reach 3.13 million units by 2030, at a CAGR of 28.35% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing adoption of electric vehicles and the efforts to enhance EV charging infrastructure supported by government initiatives are expected to drive the EV charging equipment market during the forecast period.

- Conversely, the market's growth during the forecast period may be stunted by the high installation and maintenance costs tied to setting up charging stations.

- However, the burgeoning European markets' demand for a comprehensive EV charging network, coupled with technological strides in EV charging equipment, presents substantial opportunities for the Europe EV charging equipment market during the forecast period.

- Germany, with its proactive initiatives promoting electric vehicle adoption, is poised for notable growth in the European landscape.

Europe Electric Vehicle (EV) Charging Equipment Market Trends

Battery Electric Vehicles Segment to Dominate the Market

- Battery electric vehicles (BEVs), commonly known as electric vehicles, utilize a sizable traction battery pack to power their electric motors. To recharge, these vehicles connect to electric vehicle supply equipment (EVSE).

- BEVs, being entirely electric, typically lack an internal combustion engine (ICE), fuel tank, or exhaust pipe. They derive their energy from a grid-recharged battery pack. As zero-emission vehicles, BEVs do not produce the harmful tailpipe emissions associated with traditional gasoline-powered cars, thus mitigating air pollution.

- Europe's automotive industry is undergoing a significant shift, with battery electric vehicles (BEVs) gaining traction and popularity. Driven by technological advancements, governmental backing, and heightened environmental awareness, BEVs are emerging as a viable solution to combat climate change and lessen dependence on fossil fuels.

- Data from the International Energy Agency (IEA) reveals that BEV sales in the European Union reached approximately 1.6 million units in 2023, marking a 33% increase from 1.2 million units in 2022. Furthermore, the total BEV stock in the EU has climbed to around 4.6 million units. As BEV sales surge, the demand for charging infrastructure in Europe intensifies.

- Moreover, several European governments are strategizing to amplify EV adoption in the upcoming years. For instance, in May 2024, the French government set an ambitious target for its automakers: to produce two million electric or hybrid vehicles by the decade's end. As part of a new medium-term agreement with the government, the industry aims for an interim target of 800,000 electric vehicle sales by 2027, a significant jump from 200,000 in 2022. Additionally, carmakers are setting their sights on boosting electric light utility vehicle sales to 100,000 annually, up from 16,500 in 2022. Such ambitious goals are poised to drive a substantial demand for EV charging equipment in the region.

- According to the European Automobile Manufacturers' Association (ACEA), the EU saw the installation of only about 150,000 public charging points in 2023 (averaging less than 3,000 weekly), bringing the total to over 630,000. In contrast, the European Commission aims for a target of around 3.5 million charging points by 2030. Achieving this would necessitate an installation rate of approximately 410,000 public charging points annually (or nearly 8,000 weekly), nearly three times the current rate.

- Conversely, ACEA projects a need for 8.8 million charging points by 2030. Meeting this demand would require an annual installation of 1.2 million chargers (or over 22,000 weekly), which is eight times the current rate. Such ambitious targets underscore the growing BEV market in Europe and the corresponding surge in demand for EV charging equipment.

- In recent years, several prominent Chinese automakers have expressed interest in establishing manufacturing and assembly plants in Europe, aiming to boost sales of competitively priced vehicles and challenge their European counterparts. For instance, in April 2024, Chery Auto, China's leading automaker by export volume, announced a joint venture with Spain's EV Motors to inaugurate its inaugural European manufacturing facility in Catalonia, with production slated to commence later in 2024. Furthermore, discussions are underway for potential car factories in Britain this decade.

- In 2023, BYD, the world's foremost EV manufacturer, declared plans for its maiden European production base in Hungary, set to commence operations in three years. This facility will cater to the European market, producing both battery EVs and plug-in hybrids. Such developments are anticipated to bolster the BEV manufacturing sector, subsequently amplifying the demand for a robust EV charging infrastructure.

- Given these dynamics, the BEV segment is poised to lead the European EV charging equipment market in the coming years.

Germany to Witness a Significant Growth

- Germany has been rapidly expanding its electric vehicle (EV) equipment and infrastructure, mirroring the nation's increasing embrace of the EV industry. According to the International Energy Agency (IEA), by the close of 2023, Germany boasted approximately 108,000 publicly available EV charging points. This tally comprised around 21,000 fast chargers and 87,000 slow chargers. Notably, in 2023, Germany added over 16,000 public slow charging points and 6,000 public fast charging points.

- The German government has ambitious plans, targeting the installation of 1 million public charging points nationwide by the end of 2030. Yet, as of late 2023, only about 11% of this target has been met. To bridge this gap, a substantial increase in public EV charging points is anticipated in the coming years, signaling a burgeoning market for EV charging equipment.

- The government is actively approving EV charging installations in diverse locales, from public spaces to residential and commercial properties. This initiative has spurred demand for EV charging equipment, catering to the rising number of electric vehicles on the roads. Expanding the EV charging infrastructure is pivotal for Germany, as it aims to alleviate range anxiety and enhance accessibility, thereby encouraging more consumers to transition to electric vehicles.

- In February 2024, Fastned, a prominent European EV charging firm, received approval to establish 34 fast-charging sites along Germany's highways. This initiative, part of the "Deutschlandnetz" tender, underscores Germany's commitment to bolstering its EV charging infrastructure. Fastned's move is a stride towards its ambitious goal of 1,000 fast charging stations across Europe by 2030.

- Companies in Germany are increasingly setting up their own EV charging hubs, a strategy to bolster the nation's EV infrastructure and cater to the surging demand for charging equipment. These hubs not only promote EV adoption but also play a role in curbing carbon emissions and championing sustainable transport solutions.

- In November 2023, Mercedes-Benz inaugurated its inaugural proprietary charging hub in Mannheim, Germany. This venture aligns with the company's global ambition of establishing over 2,000 charging stations by decade's end, featuring upwards of 10,000 fast-charging points.

- Germany is also pushing for EV chargers at gas stations, reinforcing its commitment to sustainable transport. This mandate not only promotes clean energy vehicles but also addresses broader climate change challenges.

- In September 2023, German Chancellor Olaf Scholz announced a forthcoming law stipulating that 80% of all service stations must offer fast-charging options, with a minimum capacity of 150 kilowatts.

- Given these developments, the EV charging equipment market in Germany is poised for significant growth, buoyed by rising EV adoption, robust investments, and supportive government policies and targets.

Europe Electric Vehicle (EV) Charging Equipment Industry Overview

The Europe electric vehicle (EV) charging equipment market is semi-fragmented. Some of the key players in the market (not in any particular order) include ABB Ltd, Robert Bosch GmbH, ChargePoint Inc., Siemens AG, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in Units, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Electric Vehicles and Related Investments

- 4.5.1.2 Efforts to Boost EV Charging Infrastructure Supported by Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 High Installation Costs Associated With Setting Up Charging Stations And Maintenance Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Battery Electric Vehicle (BEV)

- 5.1.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.1.3 Hybrid Electric Vehicle (HEV)

- 5.2 Application

- 5.2.1 Home Charging

- 5.2.2 Workplace Charging

- 5.2.3 Public Charging

- 5.3 Charging Type

- 5.3.1 AC Charging (Level 1 and Level 2)

- 5.3.2 DC Charging

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Nordic

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 Robert Bosch GmbH

- 6.3.3 Delta Electronics Inc.

- 6.3.4 Siemens AG

- 6.3.5 Tesla Inc.

- 6.3.6 ChargePoint Inc.

- 6.3.7 Enphase Energy, Inc.

- 6.3.8 Powercharge

- 6.3.9 Ampure

- 6.3.10 Exicom Tele-Systems Ltd

- 6.3.11 Schneider Electric SE

- 6.3.12 Eaton Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technology Advancement in the EV Charging Equipment

- 7.2 Need for a Robust EV Charging Network in the Emerging European Markets