|

市場調査レポート

商品コード

1636535

アジア太平洋地域のバイオ医療廃棄物管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)APAC Bio-Medical Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のバイオ医療廃棄物管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

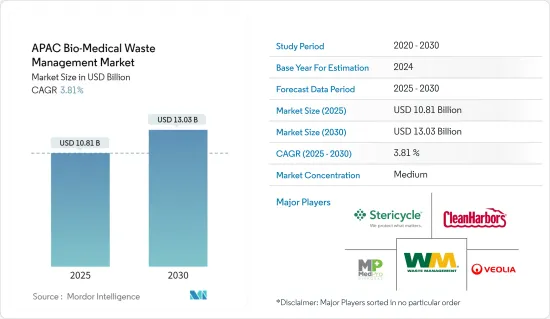

アジア太平洋地域のバイオ医療廃棄物管理の市場規模は2025年に108億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.81%で、2030年には130億3,000万米ドルに達すると予測されます。

アジア太平洋地域のバイオ医療廃棄物管理市場は、病院、クリニック、研究所、研究機関などのヘルスケア施設から発生する廃棄物の収集、処理、処分に焦点を当てています。この市場を牽引しているのは、厳しい政府規制、ヘルスケア部門の成長、不適切なバイオ医療廃棄物処理が環境に与える影響に対する意識の高まりです。

インドでは、合計1,590TPDの処理能力があるにもかかわらず、約700TPDのバイオ医療廃棄物が発生し、640TPDが処理されています。焼却処理能力は857TPD、オートクレーブ処理能力は752TPDと報告されています。

このような余剰能力にもかかわらず、国内の20の州では、CBWTFが不足しているため、キャプティブ処理手段や深穴埋設に頼っています。しかし、既存のギャップや漏れに対処しなければ、廃棄物発生量の増加が課題となる可能性があります。すべてのSPCBは、ギャップ分析を行い、漏れを推定し、このシナリオに取り組むためにより新しいCBWTFを戦略的に計画するよう求められています。

13,500以上の医療施設があるベトナムでは、毎日およそ22トンのプラスチック廃棄物が発生しています。このうち65%以上が感染性です。感染性プラスチック廃棄物が蔓延している主な原因は、器具や用具から点滴ラインや注射器に至るまで、様々な医療用途でプラスチックが多用されていることにあります。

事態の深刻さを認識したCHERADは、ベトナムの複数の病院と提携し、循環経済モデルを試験的に導入しました。汚染削減」プロジェクトの一環として、カントー中央総合病院は医療用プラスチック廃棄物を消毒するオートクレーブシステムを採用しました。この取り組みには、廃棄物の分別、リサイクル、コミュニティへの参加を強化するためのトレーニング・セッションも含まれています。

パンデミックの間、インドネシアでは1日当たりの医療廃棄物が30%急増し、その総量は約382トンと、パンデミック前の293トンから増加しました。このデータは、全国2,820の病院と9,884の保健所から得られたものです。特にジャカルタでは、首都から約30キロ離れた西ジャワ州ブカシのブランケン埋立地で、医療廃棄物が500%も急増しました。

インドネシアは多くの国と同様、リサイクル不可能で生分解性のないプラスチック廃棄物の課題に取り組んでおり、埋立地の著しい蓄積につながっています。インドネシア最大のジャカルタにあるバンタル・ゲバン埋立地では、毎日900台以上のトラックが5,000トン以上の固形廃棄物を下ろしています。この緊急性を認識したインドネシアは、2025年までにプラスチック廃棄物を70%削減するという野心的な目標を設定し、この目標に向けて毎年10億米ドルを拠出しています。

インド、ベトナム、インドネシアのような国々がバイオ医療的廃棄物管理で前進している一方で、特に都市部と農村部の間には格差が存在します。インドの急成長は、新興国が廃棄物管理システムの著しい改善を示すなど、状況が進化していることを裏付けています。

結論として、バイオ医療的廃棄物の管理は、特に廃棄物発生量の増加やリサイクル不可能な物質がもたらす課題に直面する多くの国々にとって、依然として重要な問題です。

特に新興国では大きな進展が見られるもの、持続可能で効果的な廃棄物管理を実践するためには、継続的な投資、戦略的計画、地域社会の関与が明らかに必要です。

インド、ベトナム、インドネシアなどの国々の努力は、バイオ医療的廃棄物が環境と健康に与える影響を軽減するために、能力と運営上の課題の両方に取り組むことの重要性を強調しています。

アジア太平洋地域のバイオ医療廃棄物管理市場の動向

有害廃棄物セグメントが市場を独占

2022会計年度、南アジアでは有害廃棄物の生産量が急増し、1,200万トンを超え、ほぼ半分が利用可能とみなされました。Indian Journal of Pharmacy Practiceの報告書によると、医薬品需要の急増は医薬品廃棄物の増加に直結すると強調されています。

インドの中央公害管理委員会(Central Pollution Control Board)のデータによると、インドの医療施設は合計で毎日4,075トン以上の廃棄物を排出しています。WHOとユニセフの共同評価によると、24カ国の医療施設のうち、適切な医薬品廃棄物管理システムを導入しているのは58%に過ぎないです。

同報告書はまた、医薬品廃棄物の処理に化学消毒剤を使用すると、誤って有害化合物を大気中に放出してしまう可能性があり、取り扱いを誤ると重大な健康被害をもたらすと警告しています。

ベトナムに焦点を移すと、同国は13,500を超える医療施設を誇り、合計で毎日約22トンのプラスチック廃棄物を排出しており、感染性廃棄物はこの量の65%以上を占めています。一方、中国は2022年に100万トンを超える有害産業廃棄物を処理しました。

この産業廃棄物は固体、半固体、液体に及び、未処理のまま放置されると、本質的に毒性があり、汚染し、危険です。浄化方法には、化学的・生物学的治療、熱利用、固形化などがあります。

結論として、南アジア、ベトナム、中国における有害廃棄物の生産量の増加は、効果的な廃棄物管理ソリューションの緊急の必要性を強調しています。このデータは、健康リスクと環境汚染を軽減するための適切な処理・処分方法の重要な役割を浮き彫りにしています。

医薬品と産業活動の需要が増加し続ける中、公衆衛生と環境を守るため、強固な廃棄物管理手法の導入がますます重要になっています。

市場をリードする中国

14億人を超える人口を抱える中国は、膨大な医療廃棄物を排出する巨大ヘルスケアシステムを運営しており、堅牢な廃棄物管理ソリューションが必要とされています。

中国における都市化と経済成長はヘルスケア施設の拡大につながり、その結果、バイオ医療的廃棄物の発生がエスカレートしています。にもかかわらず、中国の医療費は伸びているとはいえ、多くの高所得国に比べればまだ遅れています。高齢化と富裕層の増加によるプレッシャーの高まりを予測し、政府は今後10年間でヘルスケア予算を強化する計画です。

さらに、社会的支出は中国の医療状況を形成する上で極めて重要な役割を果たすことになると思われます。China Merchants Securitiesのチーフ・マクロ・アナリストであるXie Yaxuanは、保険、健康保険料、社会医療補助を含む社会的・商業的チャネルからの割合が増加しているヘルスケア資金のシフトを強調しました。

中国政府は、環境と公衆衛生のリスクを軽減するため、医療廃棄物の適切な処理を確保するための厳格な規制を導入しました。政府は集中処理システムを確立し、焼却のような先進技術を活用することで、効率と環境への優しさを高めました。

バイオメディカル廃棄物管理における中国の優位性は、廃棄物の大量発生につながる膨大な人口と広範なヘルスケア・システム、政府の厳しい監督、最先端技術への多額の投資、持続的な経済成長、環境意識の高まりなど、いくつかの要因に起因します。これらの要素が相まって、中国は効果的なバイオ医療廃棄物管理のフロントランナーとしての地位を確固たるものにしています。

アジア太平洋地域バイオ医療廃棄物管理産業の概要

アジア太平洋地域のバイオ医療廃棄物管理市場は、主に一握りの主要企業が主導する著しい集中が特徴です。この優位性は、手ごわい参入障壁、インフラや技術投資に対する大きな需要、大規模な事業体が小規模な競合他社を吸収する動向に起因しています。

この情勢における注目すべきプレーヤーは、Stericycle Inc.、Veolia Environmental Services、Waste Management Inc.、Clean Harbors Inc.、MedPro Disposalなどです。その結果、市場の競合情勢は引き続き安定し、これらの大手企業が市場力学に影響を与え、イノベーションを推進すると予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 新興経済諸国における病院数の増加

- 医療廃棄物発生量の増加

- 市場抑制要因

- 高額な設備投資

- 認識不足

- 市場機会

- 効果的な医療廃棄物管理のための新技術開発

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 地政学とCOVID-19パンデミックが市場に与える影響

第5章 市場セグメンテーション

- 廃棄物タイプ別

- 有害

- 非有害

- サービスタイプ別

- 回収

- 輸送・保管

- 治療と処分

- その他のサービスタイプ

- 地域別

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

第6章 競合情勢

- 市場集中

- 企業プロファイル

- Veolia Environnement SA

- Waste Management Inc.

- Clean Harbors Inc.

- Remondis SE & Co. KG(Rethmann Se & Co. Kg)

- Biomedical Waste Solutions LLC

- Daniels Sharpsmart Inc.(Daniel Health)

- Sharps Compliance Inc.

- Republic Services Inc.(Cascade Investment Group Inc.)

- EcoMed Services(Tristel PLC)

- Stericycle Inc.

- その他の企業

第7章 市場機会と今後の動向

第8章 付録

The APAC Bio-Medical Waste Management Market size is estimated at USD 10.81 billion in 2025, and is expected to reach USD 13.03 billion by 2030, at a CAGR of 3.81% during the forecast period (2025-2030).

The APAC Bio-Medical Waste Management Market focuses on the collection, treatment, and disposal of waste generated from healthcare facilities like hospitals, clinics, laboratories, and research institutions. This market is driven by stringent government regulations, the growing healthcare sector, and increasing awareness about the environmental impact of improper biomedical waste disposal.

India generates approximately 700 TPD of biomedical waste, with 640 TPD being treated, despite a combined treatment capacity of 1,590 TPD. The reported incineration capacity of the country stands at 857 TPD while autoclaving capacity is 752 TPD.

Despite this surplus capacity, 20 states in the country resort to captive treatment measures and deep pit burials due to the lack of CBWTFs. However, the rising waste generation could pose challenges if existing gaps and leakages are not addressed. All SPCBs are urged to conduct gap analyses, estimate leakages, and strategically plan newer CBWTFs to tackle this scenario.

Vietnam, with over 13,500 medical facilities, generates roughly 22 tons of plastic waste daily. Of this, more than 65% is infectious. The prevalence of infectious plastic waste is primarily due to the extensive use of plastic in various medical applications, from equipment and tools to intravenous lines and syringes.

Recognizing the gravity of the situation, CHERAD partnered with multiple hospitals in Vietnam to pilot a circular economy model. As part of the "Reducing Pollution" project, Can Tho Central General Hospital adopted an autoclave system to disinfect medical plastic waste. This initiative includes training sessions to enhance waste separation, recycling, and community engagement.

During the pandemic, Indonesia witnessed a 30% surge in daily medical waste, totaling around 382 tonnes, up from pre-pandemic figures of 293 tonnes. This data was sourced from 2,820 hospitals and 9,884 health centers nationwide. Notably, Jakarta saw a 500% spike in medical waste at the Burangkeng landfill in Bekasi, West Java, around 30 kilometers from the capital.

Indonesia, like many nations, grapples with the challenge of non-recyclable and non-biodegradable plastic waste, leading to significant landfill accumulation. The Bantar Gebang landfill in Jakarta, Indonesia's largest, witnesses over 900 trucks daily, unloading more than 5,000 tonnes of solid waste. Recognizing the urgency, Indonesia has set an ambitious target of slashing plastic waste by 70% by 2025, with a commitment of USD 1 billion annually toward this goal.

While countries like India, Vietnam, and Indonesia are making strides in biomedical waste management, disparities exist, especially between urban and rural regions. India's rapid growth underscores the evolving landscape, with emerging economies showing marked improvements in their waste management systems.

In conclusion, the management of biomedical waste remains a critical issue for many countries, particularly in the face of increasing waste generation and the challenges posed by non-recyclable materials.

While significant progress has been made, especially in emerging economies, there is a clear need for continued investment, strategic planning, and community engagement to ensure sustainable and effective waste management practices.

The efforts of countries like India, Vietnam, and Indonesia highlight the importance of addressing both capacity and operational challenges to mitigate the environmental and health impacts of biomedical waste.

APAC Bio-Medical Waste Management Market Trends

The Hazardous Waste Segment is Dominating the Market

In the financial year 2022, South Asia saw a surge in hazardous waste production, exceeding 12 million metric tons, with almost half being deemed utilizable. A report from the Indian Journal of Pharmacy Practice highlighted that the upsurge in pharmaceutical demand directly correlates with increased drug wastage.

Data from India's Central Pollution Control Board revealed that healthcare facilities in the country collectively produce over 4,075 tons of waste daily. A joint assessment by WHO and UNICEF found that only 58% of healthcare facilities across 24 countries have proper pharmaceutical waste management systems in place.

The report also warns that using chemical disinfectants to treat pharmaceutical waste can inadvertently release harmful compounds into the atmosphere, posing significant health risks if mishandled.

Shifting focus to Vietnam, the nation boasts over 13,500 medical facilities, collectively generating approximately 22 tons of plastic waste each day, with infectious waste accounting for over 65% of this volume. Meanwhile, in 2022, China disposed of over one million metric tons of hazardous industrial waste.

This industrial waste, spanning solid, semi-solid, and liquid forms, is inherently toxic, polluting, and hazardous if left untreated. Remediation methods encompass chemical and biological treatments, heat applications, and solidification.

In conclusion, the escalating production of hazardous waste in South Asia, Vietnam, and China underscores the urgent need for effective waste management solutions. The data highlights the critical role of proper treatment and disposal methods to mitigate health risks and environmental pollution.

As the demand for pharmaceuticals and industrial activities continues to rise, implementing robust waste management practices becomes increasingly vital to safeguard public health and the environment.

China is Poised to Lead the Market

With a population exceeding 1.4 billion, China operates a vast healthcare system that yields substantial volumes of medical waste, necessitating robust waste management solutions.

Urbanization and economic growth in China have led to the expansion of healthcare facilities, consequently escalating the generation of biomedical waste. Despite this, China's healthcare expenditure, while growing, still lags behind that of many high-income nations. Anticipating heightened pressure from an aging and increasingly affluent populace, the government plans to bolster healthcare budgets over the coming decade.

Furthermore, social expenditures are poised to be pivotal in shaping China's healthcare landscape. Xie Yaxuan, Chief Macro Analyst at China Merchants Securities, highlighted a shift in healthcare funding, with an increasing share coming from social and commercial channels, including insurance, health premiums, and social healthcare aid.

The Chinese government rolled out stringent regulations to ensure the proper disposal of medical waste, aiming to mitigate environmental and public health risks. The government established centralized disposal systems, leveraging advanced technologies like incineration, enhancing efficiency and eco-friendliness.

China's preeminence in biomedical waste management results from several factors, including its massive population and extensive healthcare system, leading to high waste generation, stringent government oversight, substantial investments in cutting-edge technologies, sustained economic growth, and increasing environmental consciousness. These elements collectively solidify China's position as a frontrunner in effective biomedical waste management.

APAC Bio-Medical Waste Management Industry Overview

The bio-medical waste management market in Asia-Pacific is characterized by significant concentration, primarily led by a handful of key players. This dominance results from formidable entry barriers, substantial demands for infrastructural and technological investments, and the trend of larger entities absorbing smaller competitors.

Notable players in this landscape encompass Stericycle Inc., Veolia Environmental Services, Waste Management Inc., Clean Harbors Inc., and MedPro Disposal. Consequently, the market's competitive landscape is expected to remain stable, with these major players continuing to influence market dynamics and drive innovation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Number of Hospitals in Developing Economies

- 4.2.2 Increasing Volume of Medical Waste Generated

- 4.3 Market Restraints

- 4.3.1 High Capital Investment

- 4.3.2 Lack of Awareness

- 4.4 Market Opportunities

- 4.4.1 Development of New Technologies for Effective Biomedical Waste Management

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Porter's Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Geopolitics and the COVID-19 Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Type of Waste

- 5.1.1 Hazardous

- 5.1.2 Non-hazardous

- 5.2 By Service Type

- 5.2.1 Collection

- 5.2.2 Transportation and Storage

- 5.2.3 Treatment and Disposal

- 5.2.4 Other Service Types

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Veolia Environnement SA

- 6.2.2 Waste Management Inc.

- 6.2.3 Clean Harbors Inc.

- 6.2.4 Remondis SE & Co. KG (Rethmann Se & Co. Kg)

- 6.2.5 Biomedical Waste Solutions LLC

- 6.2.6 Daniels Sharpsmart Inc. (Daniel Health)

- 6.2.7 Sharps Compliance Inc.

- 6.2.8 Republic Services Inc. (Cascade Investment Group Inc.)

- 6.2.9 EcoMed Services (Tristel PLC)

- 6.2.10 Stericycle Inc.*

- 6.3 Other Companies