|

市場調査レポート

商品コード

1636435

世界の地中中電圧ケーブル-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Global Underground Medium Voltage Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の地中中電圧ケーブル-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

地中中電圧ケーブルの世界市場規模は2025年に168億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.71%で、2030年には243億9,000万米ドルに達すると予測されています。

主要ハイライト

- 中期的には、世界の地中中電圧ケーブル市場は、再生可能エネルギー発電の統合の増加、送電網の老朽化、送配電インフラへの大規模投資によって牽引されています。

- その一方で、原料価格の上昇や分散型再生可能エネルギー発電に必要な投資が市場成長を抑制しています。

- 信頼性が高く弾力性のある配電システムの必要性、データセンター、病院、その他の産業用建物の増加、ケーブル技術の進歩、エネルギーインフラの近代化を目的とした政府の支援施策などがあります。世界の地中中電圧ケーブル市場は、今後も成長軌道を維持すると予想されます。

- アジア太平洋は最近大きな市場シェアを占めており、予測期間中最も急成長する市場になると予想されます。

世界の地中中電圧ケーブル市場動向

商業・産業セグメントが支配的と予想

- 都市部では、信頼性と安全性の高い電力供給を確保するため、地中中電圧ケーブルが広く利用されています。これらのケーブルは、架空線の乱雑さを解消するだけでなく、悪天候や物理的損傷による停電のリスクを軽減します。

- これらのケーブルは、従来型電源と再生可能電源の両方を含む発電所からエンドユーザーまでの安定的かつ効率的な配電を促進します。電力需要の急増に伴い、発電所の数も増加すると予想されています。

- 例えば、世界の発電量は2022年の29,188.1 TWhから2023年には29,924.8 TWhに増加し、2.52%の成長率を記録しました。さらに、2030年までに世界の電力市場は、再生可能エネルギー容量をさらに5500GW増加させるという予測もあります。このような開発により、地中中電圧ケーブルの需要が拡大する見込みです。

- 大規模なデータセンター、商業オフィス、ホテル、病院、IT・電気通信部門、鉄道、中小規模の産業など、商業・産業団体は、操業に不可欠な安全で中断のない電力供給のために、地中の中電圧(MV)電力ケーブルに依存しています。

- 北米や欧州などの地域では、商業運営における厳格な安全・信頼性規制により、これらのケーブルの採用が先行しています。さらに、老朽化した産業用インフラのアップグレードにも注目が集まっています。持続可能性とエネルギー効率に向けた世界のシフトは、再生可能エネルギーの入力を管理し、出力を最適化することに長けた先進的ケーブルソリューションの採用をさらに加速しています。

- 2024年4月、NKTはデンマーク、スウェーデン、チェコ共和国にある中電圧(MV)工場の生産能力増強を目的とした1億ユーロの投資を発表しました。この戦略的拡大は、欧州全域における送電網の増強と再生可能エネルギーへの取り組みを強化するもので、新たに増強された生産能力は2025~2026年にかけて稼働を開始する予定です。

- このような動きの中で、商業・産業セグメントは、このセグメントの自由化と増え続ける電力需要に後押しされ、市場の優位性を維持する構えです。

アジア太平洋が支配的となる展望

- インド、中国、日本、韓国における急速な都市化、工業化、エネルギー需要の増加により、アジア太平洋が世界の地中中電圧ケーブル市場の先陣を切ることになります。

- 歴史的に、アジア太平洋はインフラ開発投資のホットスポットでした。中国、インド、日本などの国々は、架空ケーブルから地中ケーブルへの移行を進めており、この移行は急速な都市化と産業成長に大きく後押しされています。

- アジア太平洋の発電量は、2022年の1万4,543.4 TWhから2023年には1万5,282.0 TWhに増加し、5.08%の成長率を記録しました。この一貫した上昇は、急増するエネルギー需要に対応するためのこの地域のコミットメントを強調するものです。

- 最近では、再生可能エネルギープロジェクトや革新的な送電網構想の急増が目立っています。これを踏まえ、各国政府は電力インフラの近代化のために多額の投資を行っており、特に地中中電圧(MV)ケーブルの敷設に力を入れています。

- 例えば、インド政府は今後10年間で設備容量を倍増させることを目指しており、再生可能エネルギーの強化に力を入れています。2030年までに、再生可能エネルギーによる発電容量を5,000GWにすることを目標としており、そのためには約2,250億~2,500億米ドルの投資が必要となります。

- 電力需要の増大に鑑み、中国政府は2021~2025年にかけて、送電網のインフラ整備に9,000億米ドル近くを割り当てています。同時に、中国国民生用電子機器網総公司は、送電、電気自動車充電器、デジタルインフラなどのセグメントに重点を置き、送電網インフラと関連セグメントへの投資が6兆人民元を超えると予測しています。

- このような力学を考えると、アジア太平洋は地中中電圧ケーブル市場における優位性を維持する構えです。

世界の地中中電圧ケーブル産業概要

世界の地中中電圧ケーブル市場は半分断されています。この市場の主要企業(順不同)には、Prysmian SpA、NKT A/S、Sumitomo Electric Industries Ltd、Nexans SA、Southwire Companyなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 調査の前提条件と市場定義

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:100万米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 再生可能エネルギー発電の統合の増加

- 電力網の老朽化と送配電インフラへの投資

- 抑制要因

- 原料価格の上昇と分散型再生可能エネルギー発電への投資

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 投資分析

第5章 市場セグメンテーション

- 電圧レベル

- 18KV以下

- 18~36KV

- 用途

- 住宅用

- 商業と工業用

- 公益事業

- 絶縁

- 架橋ポリエチレン(XLPE)

- エチレンプロピレンゴム(EPR)

- その他

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- ベトナム

- タイ

- インドネシア

- マレーシア

- その他のアジア太平洋

- 南米

- アルゼンチン

- ブラジル

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- カタール

- 南アフリカ

- ナイジェリア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- 合併、買収、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Hellenic Cables SA

- Nexans SA

- Southwire Company LLC

- NKT AS

- Prysmian SPA

- Hengtong Group

- LS Cable & System Limited

- Polycab India Limited

- The Okonite Company

- USA Wire & Cable, Inc.

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 住宅、商業、産業部門における信頼性と回復力のある配電システムの必要性

目次

Product Code: 50003666

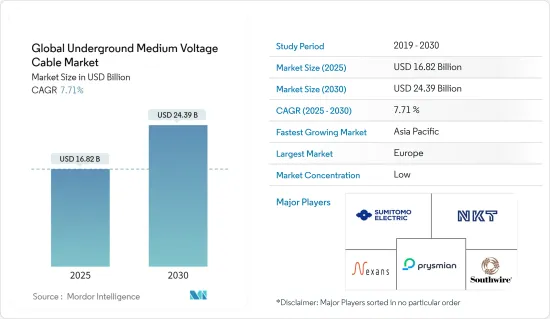

The Global Underground Medium Voltage Cable Market size is estimated at USD 16.82 billion in 2025, and is expected to reach USD 24.39 billion by 2030, at a CAGR of 7.71% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the global underground medium voltage cables market has been driven by the increasing integration of renewable energy generation, the aging power grid, and significant investments in transmission and distribution infrastructure.

- On the other hand, the market growth is restrained by rising raw material prices and the investments required for distributed renewable energy generation.

- Nevertheless, due to the need for reliable and resilient power distribution systems, increasing data centers, hospitals, and other industrial buildings, advancements in cable technology, and supportive government policies aimed at modernizing energy infrastructure. The global underground medium voltage cables market is expected to continue its growth trajectory.

- Asia-Pacific recently held a significant market share, and it is expected to be the fastest growing market during the forecast period.

Global Underground Medium Voltage Cable Market Trends

Commercial & Industrial Segment is Expected to Dominate

- Urban areas extensively utilize underground medium voltage cables to ensure a reliable and safe power supply. These cables not only eliminate the clutter of overhead lines but also mitigate the risk of power outages due to adverse weather or physical damage.

- These cables facilitate stable and efficient electricity distribution from power generation plants, encompassing both conventional and renewable sources, to end-users. As power demand surges, the number of power plants is anticipated to rise correspondingly.

- For instance, global electricity generation saw an uptick from 29,188.1 TWh in 2022 to 29,924.8 TWh in 2023, marking a growth rate of 2.52%. Moreover, projections indicate that by 2030, the global power market will augment its renewable capacity by an additional 5500 GW. Such developments are poised to escalate the demand for underground medium-voltage cables.

- Commercial and industrial entities, spanning large-scale data centers, commercial offices, hotels, hospitals, the IT and telecom sectors, railways, and small to medium-sized industries, depend on underground medium voltage (MV) power cables for a secure and uninterrupted power supply vital to their operations.

- Regions such as North America and Europe spearhead the adoption of these cables, driven by stringent safety and reliability regulations in commercial operations. Additionally, there's a pronounced focus on upgrading aging industrial infrastructure. The global shift towards sustainability and energy efficiency has further accelerated the adoption of advanced cabling solutions, adept at managing renewable energy inputs and optimizing outputs.

- In April 2024, NKT unveiled a EUR 100 million investment aimed at bolstering production capacity at its medium-voltage (MV) factories located in Denmark, Sweden, and the Czech Republic. This strategic expansion is set to bolster grid upgrades and renewable energy initiatives throughout Europe, with the newly enhanced production capacity slated to commence operations between 2025 and 2026.

- Given these dynamics, the commercial and industrial segment is poised to maintain its market dominance, fueled by the sector's liberalization and an ever-growing electricity demand.

Asia-Pacific Region is Expected to Dominate

- Due to rapid urbanization, industrialization, and rising energy demands in India, China, Japan, and South Korea, the Asia-Pacific (APAC) region is set to spearhead the global underground medium voltage cables market.

- Historically, the APAC region has been a hotspot for infrastructure development investments. Countries like China, India, and Japan have increasingly transitioned from overhead to underground cables, a shift largely fueled by their swift urbanization and industrial growth.

- Electricity generation in the Asia-Pacific region rose from 14,543.4 TWh in 2022 to 15,282.0 TWh in 2023, marking a growth rate of 5.08%. This consistent uptick underscores the region's commitment to addressing its burgeoning energy needs.

- Recently, there's been a notable surge in renewable energy projects and innovative grid initiatives. In light of this, governments are heavily investing to modernize their power infrastructure, with a pronounced emphasis on installing underground medium voltage (MV) cables.

- For example, the Indian government aims to double its installed capacity over the next decade, with a keen focus on boosting renewable energy. By 2030, India targets a renewable power generation capacity of 500 GW, a goal that will require an investment of about USD 225-250 billion.

- In light of escalating power demands, the Chinese government has allocated nearly USD 900 billion for its power grid infrastructure from 2021 to 2025. At the same time, the State Grid Corporation of China anticipates investments in power grid infrastructure and related sectors to surpass CNY 6 trillion, emphasizing areas like power transmission, electric vehicle chargers, and digital infrastructure.

- Given these dynamics, the Asia-Pacific region is poised to maintain its dominance in the underground medium voltage cables market.

Global Underground Medium Voltage Cable Industry Overview

The Global underground medium voltage cable market is semi-fragmented. Some of the key players in this market (in no particular order) include Prysmian SpA, NKT A/S, Sumitomo Electric Industries Ltd, Nexans SA, and Southwire Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

- 1.2 Study Assumptions and Market Definition

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, In USD Million, Till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing integration of renewable energy generation

- 4.5.1.2 Aging power grids and investments in transmission and distribution infrastructure

- 4.5.2 Restraints

- 4.5.2.1 Increasing raw material prices and investments in distributed renewable energy generation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products And Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Voltage Level

- 5.1.1 Less Than 18 KV

- 5.1.2 18 KV To 36 KV

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Commercial and Industrial

- 5.2.3 Utility

- 5.3 Insulation

- 5.3.1 Cross-linked Polyethylene (XLPE)

- 5.3.2 Ethylene Propylene Rubber (EPR)

- 5.3.3 Other Insulations

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Turkey

- 5.4.2.7 Russia

- 5.4.2.8 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Vietnam

- 5.4.3.5 Thailand

- 5.4.3.6 Indonesia

- 5.4.3.7 Malaysia

- 5.4.3.8 Rest of Asia Pacific

- 5.4.4 South America

- 5.4.4.1 Argentina

- 5.4.4.2 Brazil

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Egypt

- 5.4.5.4 Qatar

- 5.4.5.5 South Africa

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, And Agreements

- 6.2 Strategies Adopted By Leading Players

- 6.3 Company Profiles

- 6.3.1 Hellenic Cables SA

- 6.3.2 Nexans SA

- 6.3.3 Southwire Company LLC

- 6.3.4 NKT AS

- 6.3.5 Prysmian SPA

- 6.3.6 Hengtong Group

- 6.3.7 LS Cable & System Limited

- 6.3.8 Polycab India Limited

- 6.3.9 The Okonite Company

- 6.3.10 USA Wire & Cable, Inc.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Need for reliable and resilient power distribution systems for residential, commercial, and industrial sectors