|

市場調査レポート

商品コード

1636262

ASEAN諸国の内陸水路貨物輸送:市場シェア分析、産業動向、成長予測(2025年~2030年)ASEAN Inland Waterway Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEAN諸国の内陸水路貨物輸送:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

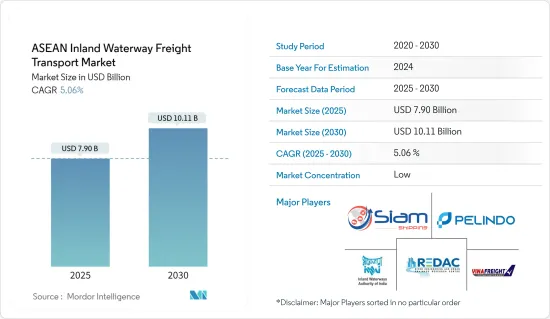

2025年のASEAN諸国の内陸水路貨物輸送市場規模は79億米ドルと推定され、予測期間(2025~2030年)のCAGRは5.06%で、2030年には101億1,000万米ドルに達すると予測されます。

主要ハイライト

- ASEAN諸国の内陸水路貨物輸送市場は、サステイナブルロジスティクスと貿易拡大に対する需要の高まりが主因となっています。

- 河川と水路の広範なネットワークを持つASEANは、内陸水路輸送に大きく依存しています。この輸送手段は貿易を円滑にするだけでなく、経済成長を促進し、ASEAN諸国の多様な地域間の結びつきを促進します。

- ASEAN諸国には河川、運河、湖沼の強力なネットワークがあり、輸送において極めて重要な役割を果たしています。メコン川、チャオプラヤ川、イラワジ川、紅河のような著名な河川は、航行の利便性を高め、国境を越えた貿易を強化するために利用され、保全されてきました。

- ASEAN諸国は、内陸水運を強化するための協定や枠組みを積極的に構築してきました。そのような取り組みのひとつが、「通過貨物の円滑化のためのASEAN枠組み協定(AFAFGIT)」です。その主要目的は、税関手続きを合理化し、国境を越えた貿易の円滑化を促進することです。同時に、ASEAN海上輸送ワーキンググループ(MTWG)は、域内の海上輸送と内陸水路輸送の連結性を強化することに注力しています。

- 内陸水路輸送は、その利点にもかかわらず、いくつかの課題を抱えています。これらの課題には、未整備のインフラ、不十分なメンテナンス、国境を越えた規制の調和の必要性などが含まれます。しかし、市場には進歩のための有望な道もあります。インフラ投資の増加、官民協力の可能性、効率性と安全性の両方を強化するための技術的進歩の統合などです。

ASEAN諸国の内陸水路貨物輸送市場の動向

コンテナ輸送需要が市場を牽引

- ASEAN諸国の内陸水路貨物輸送市場の主要原動力は、持続可能性と貿易活動の拡大に対する需要の高まりです。ASEAN諸国の経済は目覚ましい成長を遂げ、世界貿易への参加を強化しています。この拡大は、シームレスで信頼性の高い物資輸送の重要性を浮き彫りにしました。

- ASEAN諸国は積極的に世界貿易を推進し、多様なパートナーと協定を結んできました。コンテナ輸送は、このような国際貿易の急増とともに成長してきました。コンテナを活用することで、企業は国境を越えた輸送を合理化し、貿易を促進し、経済協力を強化しています。

- ASEAN諸国の数カ国は製造業の中心地として台頭し、輸出向けのさまざまな商品を生産しています。コンテナ輸送は、こうした製品に信頼性と安全性の高い輸送手段を記載しています。エレクトロニクス、自動車、繊維製品、消費財などの主要セクターは、世界市場に到達するためにコンテナ輸送に大きく依存しています。

- 地域統合に対するASEAN諸国のコミットメントは、ASEAN経済共同体(AEC)のようなイニシアティブを通じて明らかです。AECは、域内全域における商品、サービス、投資の自由な移動を促進することを目的としています。この一体化の推進は、ASEAN域内の貿易を促進するだけでなく、コンテナ輸送の必要性を高めています。

- 寧波舟山港集団によると、2024年1月から5月までの中国の港湾のコンテナ処理量は1億3,280万TEUで、2022年から8.8%増加しました。上海港のコンテナ処理量は2,090万TEUで前年比8.6%増、寧波舟山港は1,580万TEUで同6.5%増となりました。

- ASEAN諸国は貨物取扱の最前線にいます。世界銀行とS&P世界のマーケットインテリジェンスが共同で作成したコンテナ港湾パフォーマンス指数(CPPI)によると、世界の上位25港のうち18港がアジアにあり、そのうち11港が東アジア、4港が西アジアにあります。

シンガポールの港が新記録を樹立、世界貿易における優位性を反映

内陸水路が限られているにもかかわらず、シンガポールは高度で効率的な港湾システムを誇り、世界貿易の最前線に立っています。世界有数の繁華性を誇るシンガポール港は、国際貿易において極めて重要な地位を占めています。

2023年、シンガポール港は3,901万TEUという記録的なコンテナ処理能力を達成し、2021年に記録した3,757万TEUを上回りました。さらに、船舶の入港トン数も大幅に増加し、初めて30億GT(総トン数)の大台を超えました。これは、2022年から9.4%という顕著な急上昇を示し、2023年には30億9,000万GTという新記録を達成しました。

2023年の時点で、新たに運用が開始されたチュアス港フェーズ1の8つのバースが機能しています。さらに、フェーズ2の埋め立て工事は70%完了しました。港の好調な業績と連動して、貨物取扱量も一貫した成長を示し、2023年の取扱量は5億9,170万トンに達し、2022年の5億7,822万トンから増加しました。

ASEAN諸国の内陸水路貨物輸送産業概要

ASEAN諸国の内陸水路貨物輸送市場は激しい競争状態にあります。市場の主要企業には、Siam Shipping、PT Pelindo、Vinafreight、River Engineering and Urban Drainage、River Engineering and Urban Drainage Research Center、Inland Water Transport Corporation(IWTC)などがあります。

市場には複数の参入企業が存在し、市場シェアの確保に努めています。新興国市場には、規制や市場開拓に大きな影響力を持つ国営事業者が存在します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析方法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 接続性と複合一貫輸送の強化

- 経済成長と貿易が市場を牽引

- 抑制要因

- 市場に影響を与える規制遵守

- 非効率な通関手続き

- 機会

- 市場を牽引する技術の進歩

- 市場を牽引する環境の持続可能性

- 促進要因

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場における技術の進歩

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 輸送タイプ別

- 液体バルク輸送

- ドライバルク輸送

- 船舶タイプ別

- 貨物船

- コンテナ船

- タンカー

- その他

- 地域別

- シンガポール

- タイ

- ベトナム

- インドネシア

- マレーシア

- フィリピン

- その他のASEAN諸国

第6章 競合情勢

- 企業プロファイル

- Siam Shipping

- PT Pelindo

- Vinafreight

- River Engineering and Urban Drainage

- Inland Water Transport Corporation(IWTC)

- Port of Singapore Authority

- Port Klang Authority

- Port of Bangkok

- Port of Manila

- Port of Yangon*

- その他の企業

第7章 市場の将来

第8章 付録

- GDP分布(活動別、地域別)

- 資本移動に関する洞察

- eコマースと越境eコマースに関する主要データ

- 製品カテゴリー別eコマース売上高

- 対外貿易統計輸出と輸入(製品別)

The ASEAN Inland Waterway Freight Transport Market size is estimated at USD 7.90 billion in 2025, and is expected to reach USD 10.11 billion by 2030, at a CAGR of 5.06% during the forecast period (2025-2030).

Key Highlights

- The ASEAN market for inland waterway freight transport is mainly driven by the increasing demand for sustainable logistics and expanding trade.

- With its extensive network of rivers and waterways, ASEAN relies heavily on inland waterway transport. This mode of transportation not only facilitates trade but also fuels economic growth and fosters connectivity among ASEAN's diverse regions.

- ASEAN is home to a robust network of rivers, canals, and lakes, which play a pivotal role in transportation. Prominent rivers like the Mekong, Chao Phraya, Irrawaddy, and Red River have been harnessed and preserved to enhance navigability and bolster cross-border trade.

- ASEAN member states have proactively forged agreements and frameworks to bolster inland waterway transport. One such initiative is the ASEAN Framework Agreement for the Facilitation of Goods in Transit (AFAFGIT). Its primary objective is to streamline customs procedures, fostering smoother cross-border trade facilitation. Simultaneously, the ASEAN Maritime Transport Working Group (MTWG) concentrates on bolstering both maritime and inland waterway transport connectivity across the region.

- Inland waterway transport, despite its advantages, grapples with several challenges. These challenges encompass issues like underdeveloped infrastructure, insufficient maintenance, and the necessity for harmonized cross-border regulations. However, the market also holds promising avenues for progress. These include increased infrastructure investments, the potential for public-private collaborations, and the integration of technological advancements to bolster both efficiency and safety.

ASEAN Inland Waterway Freight Transport Market Trends

The Demand For Containerized Shipping is Driving the Market

- The ASEAN inland waterway transport market is mainly driven by the increasing demand for sustainability and expansion of trade activities. The economies of ASEAN countries have experienced remarkable growth, bolstering their participation in global trade. This expansion underscored the importance of seamless and reliable transportation for goods.

- ASEAN nations have actively pursued global trade, forging agreements with diverse partners. Containerized shipping has grown in tandem with this international trade surge. By leveraging containers, businesses streamline cross-border transportation, fostering trade and bolstering economic collaboration.

- Several ASEAN nations have emerged as pivotal manufacturing hubs, churning out a wide array of export-oriented goods. Containerized shipping offers a dependable and secure transport mode for these products. Key sectors like electronics, automotive, textiles, and consumer goods rely heavily on containerized shipping to reach global markets.

- ASEAN's commitment to regional integration is evident through initiatives like the ASEAN Economic Community (AEC). The AEC aims to promote unhindered movement of goods, services, and investments across the region. This drive for cohesion has not only boosted trade within ASEAN but also increased the need for containerized shipping.

- From January to May 2024, Chinese ports processed a container throughput of 132.8 million TEUs, an 8.8% uptick from 2022, according to the Ningbo Zhoushan Port Group. Shanghai Port's container throughput hit 20.9 million TEUs, marking an 8.6% Y-o-Y rise, while Ningbo Zhoushan Port recorded 15.8 million TEUs, an increase of 6.5%.

- ASEAN countries are at the forefront of cargo handling. The Container Port Performance Index (CPPI), produced jointly by the World Bank and S&P Global Market Intelligence, indicates that 18 of the world's top 25 ports are in Asia, with 11 in Eastern Asia and four in Western Asia.

Singapore's Port Sets New Records, Reflecting its Dominance in Global Trade

Despite its limited inland waterways, Singapore boasts a highly advanced and efficient port system that stands at the forefront of global trade. The Port of Singapore, renowned as one of the world's busiest, holds a pivotal position in international commerce.

In 2023, the Port of Singapore achieved a record-breaking container throughput of 39.01 million TEUs, surpassing its previous milestone of 37.57 million TEUs set in 2021. Additionally, the port witnessed a significant uptick in vessel arrival tonnage, with figures crossing the 3 billion GT (gross tonnage) mark for the first time. This marked a notable 9.4% surge from 2022, culminating in a new record of 3.09 billion GT in 2023.

As of 2023, eight berths in the newly operational Tuas Port Phase 1 were functional. Furthermore, Phase 2's reclamation works reached 70% completion. In tandem with the port's strong performance, cargo handling demonstrated consistent growth, with volumes in 2023 hitting 591.70 million tonnes, a rise from 578.22 million tonnes in 2022.

ASEAN Inland Waterway Freight Transport Industry Overview

The ASEAN inland waterway freight transport market is fiercely competitive. The major players in the market include Siam Shipping, PT Pelindo, Vinafreight, River Engineering and Urban Drainage, River Engineering and Urban Drainage Research Center, and Inland Water Transport Corporation (IWTC).

Multiple players in the market strive to secure their market share. Several ASEAN nations have state-owned operators that wield considerable influence over both regulations and infrastructure development in this market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Enhanced connectivity and intermodal integration

- 4.2.1.2 Economic growth and trade driving the market

- 4.2.2 Restraints

- 4.2.2.1 Regulatory compliances affecting the market

- 4.2.2.2 Inefficient custom procedures

- 4.2.3 Opportunities

- 4.2.3.1 Technological advancements driving the market

- 4.2.3.2 Environmental sustainability driving the market

- 4.2.1 Drivers

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Technological Advancements in the Market

- 4.6 Impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Type of Transportation

- 5.1.1 Liquid Bulk Transportation

- 5.1.2 Dry Bulk Transportation

- 5.2 By Vessel Type

- 5.2.1 Cargo Ships

- 5.2.2 Container Ships

- 5.2.3 Tankers

- 5.2.4 Other Vessel Types

- 5.3 By Geogrpahy

- 5.3.1 Singapore

- 5.3.2 Thailand

- 5.3.3 Vietnam

- 5.3.4 Indonesia

- 5.3.5 Malaysia

- 5.3.6 Philippines

- 5.3.7 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Overview

- 6.2 Company Profiles

- 6.2.1 Siam Shipping

- 6.2.2 PT Pelindo

- 6.2.3 Vinafreight

- 6.2.4 River Engineering and Urban Drainage

- 6.2.5 Inland Water Transport Corporation(IWTC)

- 6.2.6 Port of Singapore Authority

- 6.2.7 Port Klang Authority

- 6.2.8 Port of Bangkok

- 6.2.9 Port of Manila

- 6.2.10 Port of Yangon*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 GDP Distribution, by Activity and Region

- 8.2 Insights on Capital Flows

- 8.3 Key Data related to E-Commerce and Cross-Border E-Commerce

- 8.4 E-Commerce Sales by Product category

- 8.5 External Trade Statistics Export and Import, by Product