|

市場調査レポート

商品コード

1636256

廃棄物リサイクルサービス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Waste Recycling Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 廃棄物リサイクルサービス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

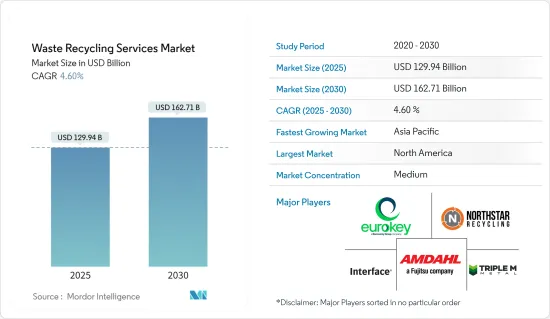

廃棄物リサイクルサービス市場規模は2025年に1,299億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.6%で、2030年には1,627億1,000万米ドルに達すると予測されます。

主要ハイライト

- 持続可能性への需要の高まりと急速な人口増加が、廃棄物リサイクルサービス市場を牽引しています。

- 現代経済における廃棄物量の増加と複雑化は、生態系と人間の健康をますます危険にさらしています。世界全体では、年間112億トンの固形廃棄物が回収されていると推定され、その有機物の腐敗は世界の温室効果ガス排出量の約5%に寄与しています。特に、電気・電子機器から排出される廃棄物には、有害物質が含まれており、先進国でも開発途上国でも最重要課題として浮上しています。

- 回収システムの欠如から不適切な廃棄方法に至るまで、廃棄物管理の不備は大気汚染につながり、水や土壌を汚染します。不適切な埋立地はさらに飲料水を汚染し、健康リスクや病気のトランスミッションを引き起こします。瓦礫の飛散は生態系に害を及ぼし、電子廃棄物や産業廃棄物から出る有害物質は都市の健康と環境の両方に負担をかける。

- 第一の解決策は廃棄物の最小化にあります。廃棄物が避けられない場合は、再製造やリサイクルに加え、材料やエネルギーの回収に重点を移します。特にリサイクルは、資源を大幅に節約できます。例えば、1トンの紙をリサイクルすれば、17本の木と通常使用される水の50%を節約できます。さらに、リサイクル産業は重要な雇用創出源であり、ブラジル、中国、米国全体で1,200万人以上を雇用しています。

- 2024年3月15日、環境・森林・気候変動省(MOEFCC)は、2016年のプラスチック廃棄物管理規則をさらに洗練させた「2024年プラスチック廃棄物管理(改正)規則」をインド官報で発表しました。発表と同時に発効したこの改正は、プラスチック汚染と闘うインドのコミットメントを強調するものです。そのため、各地域の政府機関は廃棄物を最小限に抑え、リサイクルサービスを推進する取り組みを強化しています。

廃棄物リサイクルサービスの市場動向

廃棄物リサイクル活動が活発化する自治体セグメント

国連環境計画(UNEP)の最新報告書では、自治体からの廃棄物が3分の2に急増し、関連コストが一世代でほぼ倍増すると予測されていることから、持続可能で安価な未来を確保するためには、廃棄物の発生を大幅に削減することが急務であると強調されています。

UNEPの報告書は、2023年に23億トンだった世界の都市固形廃棄物発生量が、2050年には38億トンに達すると予測しています。不適切な廃棄物管理がもたらす広範な影響(汚染、健康被害、気候変動など)を考慮すると、推定コストは3,610億米ドルにまで膨れ上がります。廃棄物管理問題への迅速な対処を怠れば、2050年までにこの世界の年間コストは6,403億米ドルという途方もない額にまで膨れ上がる可能性があり、各国が自治体廃棄物のリサイクル・イニシアチブを優先させることが急務であることを浮き彫りにしています。

世界第2位の人口を誇る中国は、産業、農業、家庭の各部門で年間100億トン以上の廃棄物を排出するという途方もない課題に直面しています。生態環境部が2024年1月に発表したこのデータは、この問題の大きさを浮き彫りにしています。しかし、中国の国内廃棄物治療には前向きな前進もあります。生活環境を改善し、経済的利益を強化するために、趙のような企業は革新的なアプローチを採用しています。特定の地域から廃棄物を集め、リサイクルできない廃棄物を焼却して都市部に電力を供給し、焼却前に果物の皮を発酵・脱水するなど、難易度の高い廃棄物に対して独自の方法を採用しています。

Saudi Investment Recycling Company(SIRC)は、2030年までに3GWの廃棄物発電能力を達成するという国の野心に沿い、廃棄物発電所への投資計画を発表しました。SIRCにとって重要な焦点は、廃棄物発電プロセスのコスト効率を高めることです。そのため、地域政府はリサイクルを促進するための様々なイニシアチブを先導しています。

市場の著しい成長を観察するアジア太平洋

アジアの急速な経済成長と都市化は、固形廃棄物の発生と管理に関する懸念を増幅させています。さらに複雑なことに、アジアの国や地域は、地理的には同じ地域であるにもかかわらず、廃棄物管理やマテリアル・サイクル施策に対する独自のアプローチを誇っています。

世界が循環型経済を推進する中、アジア太平洋市場における廃棄物管理への注目はますます高まっています。国連地域開発センターの報告によると、2014年に同地域で発生したプラスチック廃棄物の量は、なんと7,000万~1億400万トンでした。この数字は、バージンプラスチック消費量の絶え間ない増加により、2030年までに1億4,000万トンに急増する可能性があると予測されています。

再生プラスチックの需要が増加する一方で、この地域は廃棄物インフラの不足に悩まされています。しかし、このハードルを乗り越え、循環型経済のビジョンを実現するために、協力、規制、投資における協調的な取り組みが進められています。

アジア太平洋では、特に北東アジアとインド亜大陸において、機械リサイクルの存在感が確立しています。この地域の機械リサイクルの現在の設備容量は、年間1,800万トンを超えています。特に中国がこの生産能力の66%を占め、インドが約8%のシェアで続いています。2012~2022年にかけて、この地域の機械式リサイクル能力は倍増し、2018年以降は年平均約4%の成長率を維持しています。ICISの予測によると、機械式リサイクルの生産量は大幅に急増し、2023年の1,200万トンから2040年には年間3,500万トンになると推定されています。これにより、アジア太平洋は日々発生する廃棄物を削減するために乗り越えられない努力をしています。

廃棄物リサイクルサービス産業概要

廃棄物リサイクルサービス市場は細分化されています。競合情勢は多様でダイナミックです。様々な企業が、リサイクルサービス、廃棄物の収集、選別、処理、処分の提供を競っています。市場の主要企業には、Eurokey Recycling Ltd、Northstar Recycling、Triple M Metal LP、Amdahl Corp.、Interface Inc.などがあります。

中小企業も廃棄物リサイクルサービス市場で重要な役割を果たしており、専門的なサービスを提供したり、特定の地域や廃棄物の流れに対応しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 持続可能性への需要の高まりが市場を牽引

- 環境問題への関心の高まり

- 抑制要因

- 市場に影響を与える規制要因

- 市場に影響を与えるインフラの課題

- 市場機会

- 市場を牽引する技術の進歩

- 促進要因

- バリューチェーン/サプライチェーン分析

- 政府の規制、貿易協定、イニシアチブ

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 廃棄物リサイクルサービス市場における技術開拓

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 製品別

- 紙・板紙

- 金属

- プラスチック

- ガラス

- 電池・エレクトロニクス

- その他

- 供給源別

- 地方自治体(住宅と商業施設)

- 工業用

- その他の供給源

- 地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- 南米

第6章 競合情勢

- 市場集中概要

- 企業プロファイル

- Eurokey Recycling Ltd

- Northstar Recycling

- Triple M Metal LP

- Amdahl Corp.

- Interface Inc.

- Covanta

- Epson Inc.

- Collins & Aikman

- Xerox Corp.

- Fetzer Vineyards*

- その他の企業

第7章 市場の将来

第8章 付録

The Waste Recycling Services Market size is estimated at USD 129.94 billion in 2025, and is expected to reach USD 162.71 billion by 2030, at a CAGR of 4.6% during the forecast period (2025-2030).

Key Highlights

- The increasing demand for sustainability and rapid population growth drives the waste recycling services market.

- The modern economy's escalating waste volume and complexity are increasingly endangering ecosystems and human health. Globally, an estimated 11.2 billion tonnes of solid waste are collected annually, with the decay of its organic fraction contributing to about 5% of the world's greenhouse gas emissions. Notably, waste from electrical and electronic equipment, laden with new and hazardous substances, is emerging as a top challenge in both developed and developing nations.

- Poor waste management, spanning from absent collection systems to inadequate disposal methods, leads to air pollution and contaminates water and soil. Improper landfills further contaminate drinking water, posing health risks and disease transmission. Debris dispersal harms ecosystems, while hazardous substances from electronic and industrial waste strain both urban health and the environment.

- The primary solution lies in waste minimization. When waste is inevitable, the focus shifts to material and energy recovery, alongside remanufacturing and recycling. Recycling, in particular, offers significant resource savings. For instance, recycling a tonne of paper saves 17 trees and 50% of the water typically used. Additionally, the recycling industry is a significant job creator, employing over 12 million individuals across Brazil, China, and the United States.

- On March 15, 2024, the Ministry of Environment, Forest and Climate Change (MOEFCC) announced the Plastic Waste Management (Amendment) Rules, 2024, in the Gazette of India, further refining the 2016 Plastic Waste Management Rules. Effective immediately upon publication, this amendment underscored India's commitment to combating plastic pollution. Hence, government bodies across various regions are intensifying efforts to minimize waste and promote recycling services.

Waste Recycling Services Market Trends

Municipal Segment Seeing an Upsurge in Waste Recycling Activities

With municipal waste projected to surge by two-thirds and its associated costs nearly doubling within a generation, a recent report by the UN Environment Programme (UNEP) highlights the urgent need for a significant reduction in waste generation to ensure a sustainable and affordable future.

The UNEP report forecasts that global municipal solid waste generation, which stood at 2.3 billion tonnes in 2023, will reach 3.8 billion tonnes by 2050. When considering the broader impacts of inadequate waste management-such as pollution, health hazards, and climate change-the estimated cost escalates to a substantial USD 361 billion. Failing to address waste management issues promptly could see this annual global cost soar to a monumental USD 640.3 billion by 2050, underscoring the pressing need for nations to prioritize municipal waste recycling initiatives.

China, the world's second most populous country, faces a monumental challenge, producing over 10 billion tons of waste annually, spanning industrial, agricultural, and domestic sectors. This data, released by the Ministry of Ecology and Environment in January 2024, underscores the scale of the issue. However, there are positive strides in China's domestic waste treatment. In an effort to enhance living conditions and bolster economic gains, companies like Zhao's are adopting innovative approaches. They are gathering waste from specific zones, incinerating non-recyclables to power urban areas, and employing unique methods for challenging waste, like fermenting and dehydrating fruit peels before incineration.

Saudi Investment Recycling Company (SIRC) announced plans to invest in waste-to-energy plants, aligning with the nation's ambition to achieve a 3GW waste-to-energy capacity by 2030. A key focus for SIRC is enhancing the cost-efficiency of waste-to-energy processes. Hence, regional governments are spearheading various initiatives to promote recycling endeavors.

Asia-Pacific Observing Significant Growth in the Market

Asia's rapid economic growth and urbanization are amplifying concerns about solid waste generation and management. Adding complexity, each Asian country and region boasts unique approaches to waste management and material-cycle policies despite their shared geographic region.

As the world pushes toward a circular economy, the spotlight on waste management in the Asia-Pacific market intensifies. The United Nations Centre for Regional Development reported that in 2014, the region generated a staggering 70-104 million tonnes of plastic waste. Projections indicate this number could surge to 140 million tonnes by 2030, propelled by a relentless rise in virgin plastic consumption.

While the demand for recycled plastics is on the upswing, the region grapples with a glaring deficit in waste infrastructure. However, concerted efforts in collaboration, regulation, and investment are underway, aiming to surmount this hurdle and actualize the circular economy vision.

In Asia-Pacific, mechanical recycling, especially in Northeast Asia and the Indian subcontinent, has a well-established presence. The region's current installed capacity for mechanical recycling stands at over 18 million tonnes annually. Notably, China leads, accounting for 66% of this capacity, with India following with an approximately 8% share. From 2012 to 2022, the region's mechanical recycling capacity doubled, and it has maintained an average annual growth rate of about 4% since 2018. Projections from ICIS indicate a significant surge in mechanical recycling output, from 12 million tonnes in 2023 to an estimated 35 million tonnes annually by 2040. With this, Asia-Pacific is making a surmountable effort to reduce the waste generated every day.

Waste Recycling Services Industry Overview

The waste recycling services market is fragmented in nature. The competitive landscape is diverse and dynamic. Various companies compete to provide recycling services, waste collection, sorting, processing, and disposal. Some key players in the market include Eurokey Recycling Ltd, Northstar Recycling, Triple M Metal LP, Amdahl Corp., and Interface Inc.

Small and medium-sized enterprises also play a significant role in the waste recycling services market, offering specialized services or catering to specific regions or waste streams.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Demand for Sustainability Driving the Market

- 4.2.1.2 Environmental Concerns Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Regulatory Factors Affecting the Market

- 4.2.2.2 Infrastructure Challenges Affecting the Market

- 4.2.3 Opportunities

- 4.2.3.1 Technological Advancements Driving the Market

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Government Regulations, Trade Agreements, and Initiatives

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technological Developments in the Waste Recycling Services Market

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Paper & Paperboard

- 5.1.2 Metals

- 5.1.3 Plastics

- 5.1.4 Glass

- 5.1.5 Batteries & Electronics

- 5.1.6 Other Products

- 5.2 By Source

- 5.2.1 Municipal (Residential and Commercial)

- 5.2.2 Industrial

- 5.2.3 Other Sources

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Eurokey Recycling Ltd

- 6.2.2 Northstar Recycling

- 6.2.3 Triple M Metal LP

- 6.2.4 Amdahl Corp.

- 6.2.5 Interface Inc.

- 6.2.6 Covanta

- 6.2.7 Epson Inc.

- 6.2.8 Collins & Aikman

- 6.2.9 Xerox Corp.

- 6.2.10 Fetzer Vineyards*

- 6.3 Other Companies