|

市場調査レポート

商品コード

1636254

医療機器・設備ロジスティクス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Medical Devices And Equipment Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医療機器・設備ロジスティクス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

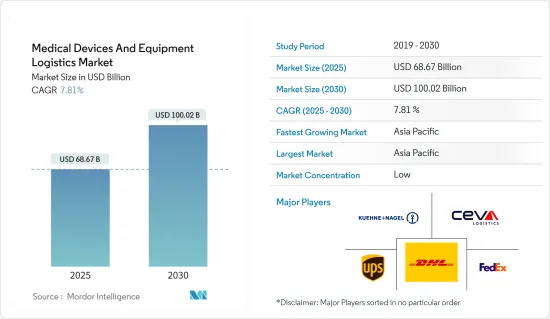

医療機器・設備ロジスティクス市場規模は、2025年に686億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.81%で、2030年には1,000億2,000万米ドルに達すると予測されます。

医療機器・設備ロジスティクス市場は、先進的医療サービスに対する需要の急増と医療機器の技術進歩に後押しされ、急速に拡大しています。メーカーや医療プロバイダーは、重要な機器のタイムリーな世界配送を確保するため、サプライチェーン業務の効率化をますます進めています。この効率化の推進は、自動化、リアルタイムの追跡システム、透明性の向上とコスト削減のための先進的在庫管理技術によってさらに強化されています。

2024年2月、GobalMed Logistix(GMLx)はアトランタ・キャンパスを200%拡大し、6万5,000平方フィートの新施設を導入することを発表し、話題となりました。この移転は、医療機器のロジスティクスとサードパーティサービスに対するニーズの高まりに直接対応するもので、産業のロジスティクス能力を大きく前進させるものです。

Wingとの協力により、Medtronicのドローン配送検査のような画期的な取り組みがラストマイルの医療物流に革命をもたらし、より迅速で適応性の高いサプライチェーンソリューションを約束しています。さらに、医療インフラの世界の拡大が続いており、特に新興国では、ロジスティクスプロバイダーが強固な物流ネットワークを構築し、高まる需要に対応できる環境が整いつつあります。

例えば、英国を拠点とするApianは2023年12月、NHSの医療供給配送を強化するためにZiplineと提携し、医療物流における継続的な技術革新の波を強調しています。

医療機器ロジスティクス市場の動向

医療機器メーカーが最先端の物流ソリューションを統合

メドトロニックは、インスリンポンプ、ペースメーカー、糖尿病治療などの医療機器や治療の多国籍メーカーです。2022年以降、Medtronicはロジスティクスとサプライチェーン業務の大規模な見直しに着手しており、2024年にその成果が結実する予定です。同社は、世界オペレーション&サプライチェーン(GOSC)、コア技術、大企業顧客を対象とした商業戦略の3つの主要セグメントに注力してきました。これは大きな方向転換を意味します。

2024年7月、Medtronicはアイルランドで最初にドローン配送会社Wingを利用し、医療用品や医療機器を病院に配送する企業のひとつとなりました。両社はダブリンのブラックロックヘルスとセント・ヴィンセント私立病院と提携し、ドローンを医療にどのように活用できるかを実証するため、ドローン配送のトライアルを開始します。

MedtronicとWingの取り組みは、医療機器市場で最先端の物流ソリューションを統合することの重要性が高まっていることを強調しています。競合他社や産業の利害関係者もこれに追随し、サプライチェーンの効率化と顧客サービスの向上を目的とした革新的技術の導入が加速する可能性があります。

英国の医療機器製造業がロジスティクス産業を牽引

2022年、Office for National Statistics(国家統計局)は、英国の医療機器・歯科用品製造業の粗付加価値額(GVA)が約29億8,000万英ポンド(38億1,000万米ドル)に上昇したと報告しました。この一貫した成長は、この産業の経済的重要性を浮き彫りにし、英国内での医療器具の生産と需要の高まりを反映しています。

産業の拡大に伴い、強固なサプライチェーンと流通ネットワークが最重要課題となっています。これらのネットワークは、医療製品の効率的な世界輸送に不可欠であり、医療施設への迅速な到着と厳しい規制への準拠を保証します。また、この産業の生産量の増加は、温度管理された倉庫、自動化された在庫システム、特殊な輸送ソリューションなど、最先端のロジスティクス技術への投資にも拍車をかけています。

ロシアによるウクライナ侵攻の影響を受けた民間人にUK-Medを通じて医薬品を提供したような、最近の人道的な試みは、産業の世界の医療支援の役割をさらに際立たせています。

要するに、英国の医療歯科用品製造産業におけるGVAの増加は、重要な医療機器の入手しやすさと利用しやすさを国内外に広げる上で、ロジスティクスが不可欠な役割を担っていることを強調しています。

医療機器・設備ロジスティクス産業概要

医療機器・設備ロジスティクス市場は、世界のロジスティクス強者からニッチなサービスプロバイダーまで、多様な参入企業を抱える競合情勢を誇っています。UPS Healthcare、DHL Supply Chain、FedEx Healthcare Solutions、Kuehne+Nagel、Ceva Logisticsといったロジスティクス大手が牽引しています。これらの産業大手は、広範な世界ネットワーク、最先端技術、充実したサービス群を活用しています。逆に、Cardinal Health、Owens & Minor、DB Schenkerのような専門的な参入企業も存在します。 これらの企業は、倉庫管理、流通、在庫管理などを含むヘルスケア業界向けの物流ソリューションをカスタマイズすることで、独自の地位を築いています。

ロジスティクス事業者と医療利害関係者のコラボレーションは、市場への浸透を広げ、サービスポートフォリオを充実させるために増加しています。IoT、AI、ブロックチェーンなどの技術の導入は、ロジスティクスチェーンの効率性と透明性を高めるため、極めて重要です。さらに、医療機器ロジスティクスのモニタリングが厳しいことを考えると、規制遵守と品質保証への確固としたコミットメントが依然として最も重要です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向

- サプライチェーン/バリューチェーン分析に関する洞察

- 産業の規制に関する洞察

- 産業の技術的進歩に関する洞察

- 地政学とパンデミックが市場に与える影響

第5章 市場力学

- 市場促進要因

- 医療サービスの世界的拡大

- 技術の進歩

- 市場抑制要因

- 高い運用コスト

- 規制の複雑さ

- 市場機会

- 新興市場への進出

- 医療プロバイダーとの戦略的パートナーシップとコラボレーションの構築

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 製品タイプ別

- 医療機器

- 医療設備

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第7章 競合情勢

- 市場集中度概要

- 企業プロファイル

- UPS Healthcare

- DHL Supply Chain

- FedEx Healthcare Solutions

- Kuehne+Nagel

- Ceva Logistics

- Cardinal Health

- Owens & Minor

- DB Schenker

- DSV

- World Courier*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

- マクロ経済指標

- 資本フロー洞察(運輸・倉庫部門への投資)

- eコマースと消費関連統計

- 対外貿易統計

The Medical Devices And Equipment Logistics Market size is estimated at USD 68.67 billion in 2025, and is expected to reach USD 100.02 billion by 2030, at a CAGR of 7.81% during the forecast period (2025-2030).

The medical devices and equipment logistics market is rapidly expanding, fueled by surging demand for advanced healthcare services and technological advancements in medical devices. Manufacturers and healthcare providers are increasingly streamlining their supply chain operations to ensure the timely global delivery of critical equipment. This efficiency drive is further empowered by automation, real-time tracking systems, and advanced inventory management techniques to boost transparency and cut costs.

In February 2024, GobalMed Logistix (GMLx) made headlines by unveiling a 200% expansion of its Atlanta campus, introducing a new 65,000-sq. ft facility. This move directly responds to the escalating need for medical device logistics and third-party services, marking a significant stride in the industry's logistics capabilities.

In collaboration with Wing, groundbreaking initiatives like Medtronic's drone delivery trials are revolutionizing last-mile healthcare logistics and promising swifter and more adaptable supply chain solutions. Moreover, the ongoing global expansion of healthcare infrastructure, especially in emerging economies, is creating a ripe environment for logistics providers to establish robust distribution networks and cater to mounting demands.

For instance, UK-based Apian partnered with Zipline in December 2023 to enhance NHS medical supply deliveries, underscoring the continuous wave of innovation in healthcare logistics.

Medical Devices and Equipment Logistics Market Trends

Medical Devices Manufacturer Integrate Cutting-edge Logistics Solutions

Medtronic is a multinational producer of medical devices and therapies, such as insulin pumps, pacemakers, and diabetes therapies. Since 2022, Medtronic has embarked on a massive overhaul of its logistics and supply chain operations that will culminate in 2024. The company has focused on three key areas: global operations and supply chain (GOSC), core technology, and commercial strategies targeting large enterprise customers. It represents a significant shift in direction.

In July 2024, Medtronic was among the first companies in Ireland to use the drone delivery company Wing to deliver medical supplies and devices to hospitals. The two companies are teaming up with Blackrock Health and St. Vincent's Private Hospital in Dublin to launch a drone delivery trial to demonstrate how drones can be used in healthcare.

Medtronic's initiative with Wing underscores the growing importance of integrating cutting-edge logistics solutions in the medical devices market. Competitors and industry stakeholders may follow suit, accelerating the adoption of innovative technologies to enhance supply chain efficiency and customer service.

UK Medical Devices Manufacturing Propels the Logistics Industry

In 2022, the Office for National Statistics reported that the UK manufacturing industry for medical and dental instruments and supplies saw its gross value added (GVA) climb to around GBP 2.98 billion (USD 3.81 billion). This consistent growth highlights the industry's economic significance and mirrors the escalating production and demand for medical instruments within the United Kingdom.

With the industry's expansion, robust supply chains and distribution networks become paramount. These networks are vital for the efficient global transportation of medical products, ensuring they reach healthcare facilities promptly and comply with stringent regulations. The industry's heightened manufacturing output also spurs investments in cutting-edge logistics technologies, including temperature-controlled storage, automated inventory systems, and specialized transportation solutions.

Recent humanitarian endeavors, like the country's provision of medical supplies to civilians affected by the Russian invasion of Ukraine through UK-Med, further underscore the industry's global healthcare support role.

In essence, the escalating GVA in the UK medical and dental supplies manufacturing industry accentuates the indispensable role of logistics in broadening the accessibility and availability of crucial healthcare equipment, both domestically and internationally.

Medical Devices and Equipment Logistics Industry Overview

The medical devices and equipment logistics market boasts a competitive landscape, hosting a diverse array of players, from global logistics powerhouses to niche service providers. Logistics giants like UPS Healthcare, DHL Supply Chain, FedEx Healthcare Solutions, Kuehne + Nagel, and Ceva Logistics lead the charge. These industry giants leverage their expansive global networks, cutting-edge technology, and a robust suite of services. Conversely, specialized players such as Cardinal Health, Owens & Minor, and DB Schenker carve their niche by tailoring logistics solutions for the healthcare sector, encompassing warehousing, distribution, and inventory management.

Collaborations between logistics entities and healthcare stakeholders are rising to broaden market penetration and enrich service portfolios. Embracing technologies like IoT, AI, and blockchain is pivotal, as they bolster efficiency and transparency in the logistics chain. Moreover, given the stringent oversight in medical device logistics, a steadfast commitment to regulatory compliance and quality assurance remains paramount.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights on Supply Chain/Value Chain Analysis

- 4.4 Insights into Governement Regualtions in the Industry

- 4.5 Insights into Technological Advancements in the Industry

- 4.6 Impact of Geopolitics and Pandemics on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Global Expansion of Healthcare Services

- 5.1.2 Technological Advancements

- 5.2 Market Restraints

- 5.2.1 High Operational Costs

- 5.2.2 Regulatory Complexity

- 5.3 Market Opportunities

- 5.3.1 Expansion into Emerging Markets

- 5.3.2 Forging Strategic Partnerships and Collaborations With Healthcare Providers

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Medical Devices

- 6.1.2 Medical Equipment

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.1.3 Mexico

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Spain

- 6.2.2.6 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 Australia

- 6.2.3.5 South Korea

- 6.2.3.6 Rest of Asia-Pacific

- 6.2.4 Middle East and Africa

- 6.2.4.1 GCC

- 6.2.4.2 South Africa

- 6.2.4.3 Rest of Middle East and Africa

- 6.2.5 South America

- 6.2.5.1 Brazil

- 6.2.5.2 Argentina

- 6.2.5.3 Rest of South America

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 UPS Healthcare

- 7.2.2 DHL Supply Chain

- 7.2.3 FedEx Healthcare Solutions

- 7.2.4 Kuehne + Nagel

- 7.2.5 Ceva Logistics

- 7.2.6 Cardinal Health

- 7.2.7 Owens & Minor

- 7.2.8 DB Schenker

- 7.2.9 DSV

- 7.2.10 World Courier*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 Macroeconomic Indicators

- 9.2 Insight Into Capital Flows (Investments In Transport and Storage Sector)

- 9.3 E-commerce and Consumer Spending-related Statistics

- 9.4 External Trade Statistics