世界の歯車-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Global Gear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636218

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

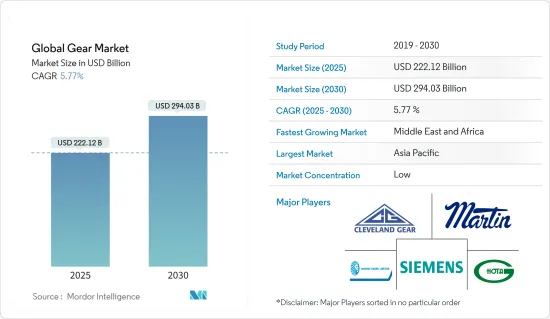

世界の歯車市場規模は、2025年に2,221億2,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは5.77%で、2030年には2,940億3,000万米ドルに達すると予測されています。

主要ハイライト

- 中期的には、産業オートメーションの台頭や世界の風力発電設備の増加といった要因が、予測期間中の世界歯車市場の最も大きな促進要因の1つになると予想されます。

- 歯車の高い生産コストは、予測期間中、世界の歯車市場を脅かすと予想されます。

- しかし、顧客の需要を効果的に満たすために、カスタマイズ型歯車を製造するための継続的な努力がなされています。この要因は、将来的に市場にいくつかの機会を生み出すと予想されます。

- アジア太平洋は、予測期間中に大きく成長し、最も高い年間成長率を記録すると予想されます。これは、同地域の製造業の成長と風力発電設備への注力によるものです。

世界の歯車市場動向

油田機器セグメントが成長を確認する

- 油田機器セグメントは、石油・ガスのバリューチェーン全体にわたる広範なアプリケーションを包含し、世界歯車市場の大部分を占めています。このセグメントでは、石油・ガス資源の探査、抽出、処理、輸送に不可欠な掘削装置、ポンプ、コンプレッサーなどの重要な機械に歯車が使用されています。

- 上流セグメント、つまり探査と生産(E&P)セグメントは、油田機器セグメントにおける歯車の重要な消費者です。歯車は、掘削装置、泥水ポンプ、ドローワーク、坑口システムなどの様々な装置で重要な役割を果たしています。上流セグメントにおける歯車の需要は、主に世界の石油・ガス価格、探査技術(地震探査や水平掘削など)の技術進歩、深海・超深海探査への注目の高まりによってもたらされています。

- 原油生産は、アジア太平洋とアフリカの経済拡大による原油需要の増加により、近年著しい伸びを示しています。また、ロシアへの制裁措置により、需要増に対応するために原油生産が増加しています。

- Energy Institute Statistical Review of World Energyによると、原油生産量は2022~2023年にかけて2%の大幅な伸びを示しました。同様に、過去10年間のCAGRは1.1%以上であり、原油の増加傾向を示しています。この成長は設備需要を促進し、産業の歯車需要を煽る。

- 中流部門には、パイプライン、トラック輸送船団、タンカー船、貯蔵施設が含まれます。歯車は、ポンプ、コンプレッサー、このセグメントで使用されるその他の機器、特にパイプライン操作とLNG処理プラントで不可欠です。中流セグメントにおける歯車需要の主要促進要因としては、パイプラインインフラの拡大、液化天然ガス(LNG)の世界の取引の増加、より効率的な輸送・貯蔵ソリューションの必要性などが挙げられます。

- 例えば、2024年6月、Oil and Natural Gas Corporation(ONGC)とIndian Oil Corp(IOC)は、マディヤ・プラデーシュ州のハッタ・ガス田に隣接するコンパクトな液化天然ガス(LNG)施設を設立する契約を締結しました。先進技術を駆使したこのプラントは、従来の化石燃料に代わる、より環境に優しいLNGを生産する予定です。LNGプラントの運転と保守には特殊な歯車が不可欠であるため、このようなLNG需要の増加は歯車市場の成長を促進すると考えられます。この開発は、歯車製造技術の革新と投資を刺激すると予想されます。

- 川下セグメントは、油田機器市場における歯車のもう一つの重要なエンドユーザーです。歯車は、ポンプ、コンプレッサー、ミキサー、コンベアシステムなど、精製所や処理プラント内の様々な機器に使用されています。下流セグメントにおける歯車需要の促進要因としては、石油精製製品に対する世界の需要の増加、より効率的で環境に優しい精製プロセスの必要性、石油化学産業の成長などが挙げられます。

- したがって、上記の点から、石油・ガス機器エンドユーザー産業は予測期間中に成長すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、世界の歯車市場において極めて重要なセグメントです。人口が急増し、経済が力強く成長しているインド、中国、韓国、ASEAN地域の国々は、工業と製造業を積極的に強化しています。このような協調的な取り組みが、歯車市場にとって有利な市場環境を作り出しています。

- 自動車産業は、アジア太平洋における歯車の主要なエンドユーザーのひとつであり、日本、韓国、中国、インドといった国々は主要な自動車製造拠点です。トランスミッションやディファレンシャルからステアリング機構やエンジン部品に至るまで、歯車の需要は広範囲に及んでいます。

- 国際自動車工業会によると、アジア太平洋の自動車生産台数は2022~2023年にかけて大幅に増加しました。2023年、同地域は5,511万5,837台の自動車を製造し、10%の成長率を再開しました。2019~2023年にかけてのCAGRは12%を超えており、この地域における歯車需要の高まりを意味しています。

- 同様に、この地域では産業セグメントが大きな成長を遂げており、産業セグメントの拡大とともに歯車の需要も増加しています。歯車は、工作機械、マテリアルハンドリング機器、建設や鉱業で使用される重機械など、様々な用途で非常に重要です。アジア太平洋全域、特に中国、インド、東南アジアのような国々における急速な工業化が、工業用歯車の大幅な需要を牽引しています。

- 例えば、2023会計年度には、インドの製造業輸出は過去最高を記録し、4,474億6,000万米ドルに達し、前年度(22年度)の4,220億米ドルから6.03%の伸びを示しました。インドのGDPの17%に寄与し、2,730万人以上の労働者を雇用する製造業は、国家経済において極めて重要です。インド政府は、さまざまな取り組みや施策により、2025年までに製造業の市場シェアを25%に引き上げることを目指しています。

- さらに、航空宇宙・防衛産業は、アジア太平洋における歯車のもう一つの重要なエンドユーザーです。日本、韓国、中国、インドなどの国々は、航空宇宙製造能力を拡大しています。この拡大が、航空機エンジン、着陸装置システム、様々な制御機構における高精度歯車の需要を牽引しています。

- したがって、上記のように、アジア太平洋は予測期間中に市場を独占すると予想されます。

世界の歯車産業概要

世界の歯車市場はセグメント化されています。この市場の主要参入企業(順不同)には、Cleveland Gear Co.、Siemens AG、Martin Sprocket & Gear Inc.、Hota Industrial Mfg.、Bharat Gears Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 産業オートメーションへの注目の高まり

- 風力エネルギー導入の増加

- 抑制要因

- 高い製造コスト

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 歯車タイプ

- 平歯車

- はすば歯車

- 遊星歯車

- ラック&ピニオン歯車

- ウォーム歯車

- かさ歯車

- その他の歯車

- エンドユーザー産業

- 油田機器

- 鉱山機械

- 産業機械

- 発電所

- 建設機械

- その他

- 2029年までの市場規模・需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ノルディック

- ロシア

- トルコ

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- カタール

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Cleveland Gear Co.

- Siemens AG

- Martin Sprocket & Gear Inc.

- Hota Industrial Mfg. Co. Ltd

- OKUBO GEAR Co. Ltd

- Bharat Gears Ltd

- Elecon Engineering Company Limited

- Precipart

- Kohara Gear Industry Co. Ltd

- Aero Gear Inc.

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- カスタマイズサービスの増加

目次

Product Code: 50003481

The Global Gear Market size is estimated at USD 222.12 billion in 2025, and is expected to reach USD 294.03 billion by 2030, at a CAGR of 5.77% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising industrial automation and the growing global wind energy installation are expected to be among the most significant drivers for the global gear market during the forecast period.

- High production costs for gears are expected to threaten the global gear market during the forecast period.

- However, continued efforts are being made to manufacture customized gears to effectively meet the client's demand. This factor is expected to create several opportunities for the market in the future.

- Asia-Pacific is expected to grow significantly and register the highest annual growth rate during the forecast period. This is due to the region's growing manufacturing industry and focus on wind energy installations.

Global Gear Market Trends

The Oilfield Equipment Segment to Witness Growth

- The oilfield equipment segment represents a significant portion of the global gear market, encompassing a wide range of applications across the entire oil and gas value chain. This segment utilizes gears in critical machinery such as drilling rigs, pumps, compressors, and other equipment essential for the exploration, extraction, processing, and transportation of oil and gas resources.

- The upstream segment, or the exploration and production (E&P) segment, is a significant consumer of gears in the oilfield equipment segment. Gears play a crucial role in various equipment such as drilling rigs, mud pumps, drawworks, and wellhead systems. The demand for gears in the upstream segment is primarily driven by global oil and gas prices, technological advancements in exploration techniques (e.g., seismic imaging and horizontal drilling), and the increasing focus on deepwater and ultra-deepwater exploration.

- Crude oil production has witnessed significant growth in recent years due to the rising demand for crude oil due to expanding economies in Asia-Pacific and Africa. Additionally, due to sanctions on Russia, oil production has increased to meet the rising demand.

- According to the Energy Institute Statistical Review of World Energy, crude oil production witnessed a significant growth of 2% between 2022 and 2023. Similarly, the average annual growth rate over the past decade has been more than 1.1%, indicating an increasing growth in crude oil. This growth drives the demand for equipment, which fuels the demand for gear in the industry.

- The midstream segment includes pipelines, trucking fleets, tanker ships, and storage facilities. Gears are essential in pumps, compressors, and other equipment used in this segment, particularly in pipeline operations and LNG processing plants. The primary driving factors for gear demand in the midstream segment include the expansion of pipeline infrastructure, increasing global trade of liquefied natural gas (LNG), and the need for more efficient transportation and storage solutions.

- For instance, in June 2024, India's State-owned Oil and Natural Gas Corporation (ONGC) and Indian Oil Corporation (IOC) inked a deal to establish a compact liquefied natural gas (LNG) facility adjacent to the Hatta gas field in Madhya Pradesh. The plant, leveraging advanced technology, is poised to churn out LNG, heralded as a greener substitute to conventional fossil fuels. This increased demand for LNG will drive growth in the gears market, as specialized gears are essential for operating and maintaining LNG plants. This development is expected to stimulate innovation and investment in gear manufacturing technologies.

- The downstream segment is another critical end user of gears in the oilfield equipment market. Gears are used in various equipment within refineries and processing plants, such as pumps, compressors, mixers, and conveyor systems. The driving factors for gear demand in the downstream segment include the increasing global demand for refined petroleum products, the need for more efficient and environmentally friendly refining processes, and the growth of the petrochemical industry.

- Therefore, as per the above points, the oil and gas equipment end-user industry is expected to grow during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is a pivotal segment in the global gear market. With a burgeoning population and robustly growing economies, nations such as India, China, South Korea, and those in the ASEAN region are actively strengthening their industrial and manufacturing industries. This concerted effort creates a favorable market environment for the gears market.

- The automotive industry is one of the primary end users of gears in Asia-Pacific, with countries like Japan, South Korea, China, and India being major automotive manufacturing hubs. The segment's demand for gears spans a wide range, from transmission systems and differentials to steering mechanisms and engine components.

- According to the International Organization of Motor Vehicle Manufacturers, automobile manufacturing in Asia-Pacific significantly rose between 2022 and 2023. In 2023, the region manufactured 5,51,15,837 automobiles, resuming a 10% growth rate. The annual average growth rate between 2019 and 2023 was over 12%, signifying the rising demand for gears in the region.

- Similarly, the industrial segment is experiencing significant growth in the area, and the demand for gears is increasing with the expanding industrial segment. Gears are crucial in various applications, such as machine tools, material handling equipment, and heavy machinery used in construction and mining. The rapid industrialization across Asia-Pacific, particularly in countries like China, India, and Southeast Asia, has driven substantial demand for industrial gear.

- For instance, in the financial year 2023, India's manufacturing exports hit a record high, reaching USD 447.46 billion, marking a 6.03% growth from the previous year's (FY22) USD 422 billion. The manufacturing industry, contributing to 17% of India's GDP and employing over 27.3 million workers, is pivotal in the nation's economy. With various initiatives and policies, the Indian government aims to elevate manufacturing's market share to 25% by 2025.

- Additionally, the aerospace and defense industry represents another significant end user of gears in Asia-Pacific. Countries such as Japan, South Korea, China, and India are expanding their aerospace manufacturing capabilities. This expansion drives the demand for high-precision gears in aircraft engines, landing gear systems, and various control mechanisms.

- Therefore, as mentioned above, Asia-Pacific is expected to dominate the market during the forecast period.

Global Gear Industry Overview

The global gear market is fragmented. Some key players in this market (in no particular order) are Cleveland Gear Co., Siemens AG, Martin Sprocket & Gear Inc., Hota Industrial Mfg. Co. Ltd, and Bharat Gears Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Focus on Industrial Automation

- 4.5.1.2 Growing Wind Energy Installation

- 4.5.2 Restraints

- 4.5.2.1 High Production Cost

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Gear Type

- 5.1.1 Spur Gear

- 5.1.2 Helical Gear

- 5.1.3 Planetary Gear

- 5.1.4 Rack and Pinion Gear

- 5.1.5 Worm Gear

- 5.1.6 Bevel Gear

- 5.1.7 Other Gear Types

- 5.2 End-user Industry

- 5.2.1 Oilfield Equipment

- 5.2.2 Mining Equipment

- 5.2.3 Industrial Machinery

- 5.2.4 Power Plants

- 5.2.5 Construction Machinery

- 5.2.6 Other End-user Industries

- 5.3 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 NORDIC

- 5.3.2.7 Russia

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 South Korea

- 5.3.3.6 Malaysia

- 5.3.3.7 Thailand

- 5.3.3.8 Indonesia

- 5.3.3.9 Vietnam

- 5.3.3.10 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 Nigeria

- 5.3.4.4 Egypt

- 5.3.4.5 Qatar

- 5.3.4.6 South Africa

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Colombia

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Cleveland Gear Co.

- 6.3.2 Siemens AG

- 6.3.3 Martin Sprocket & Gear Inc.

- 6.3.4 Hota Industrial Mfg. Co. Ltd

- 6.3.5 OKUBO GEAR Co. Ltd

- 6.3.6 Bharat Gears Ltd

- 6.3.7 Elecon Engineering Company Limited

- 6.3.8 Precipart

- 6.3.9 Kohara Gear Industry Co. Ltd

- 6.3.10 Aero Gear Inc.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Customization Offerings

世界の歯車-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日