モータースターター:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Motor Starter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636217

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

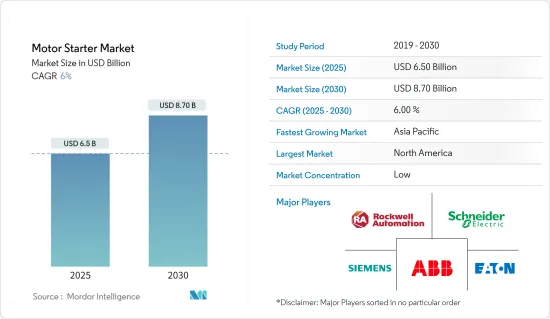

モータースターターの市場規模は2025年に65億米ドルと推計され、予測期間(2025-2030年)のCAGRは6%で、2030年には87億米ドルに達すると予測されます。

主なハイライト

- 環境問題への関心の高まりを受けて、産業界ではエネルギー消費の削減とモータ寿命の延長を目的に、ソフトスタータのようなエネルギー効率の高いモータースターターの採用が増加しています。同時に、モノのインターネット(IoT)の台頭がインテリジェントモータースターターの創造に拍車をかけ、遠隔監視と制御を可能にし、市場を進化させています。

- 電気自動車(EV)への世界のシフトは、自動車アプリケーションにおけるモータースタータを含む高度なモーター制御ソリューションへの需要を高めています。EVでは、モータースタータがバッテリー管理システムと連携して性能を最適化し、安全性を確保します。世界各国が内燃機関からEVに軸足を移す中、モータースタータの需要は急増すると予測されています。

- モータースタータ市場における最近の技術革新は、過負荷保護、温度監視、プログラム可能な設定などの高度な機能を備えた製品を導入し、信頼性と性能を高めています。メーカー各社は、さまざまな電圧レベル、定格電力、業界固有のニーズに対応したモータースターターの製品ラインを拡大しています。

- モータースターター市場は競争が激しく、多くのメーカーが市場シェアを争っています。この熾烈な競争は、しばしば価格圧力や製品差別化の課題につながります。

- マクロ経済動向、特に新興市場の力強い経済成長は、製造業や建設業におけるモータースタータの需要を促進しています。さらに、エネルギー効率と環境の持続可能性に関する規制の強化が市場力学に影響を与えています。とはいえ、同市場は継続的な成長が見込まれています。

モータースターター市場動向

製造業が市場の成長を牽引すると予測

- インダストリー4.0への移行は、製造業における自動化技術の普及に拍車をかけています。工場には高度なロボット工学や自動化システムが導入され、効率的なモータ制御が必要とされています。この進化は、多様な負荷を管理し、全体的な性能を向上させることができる洗練されたモータースターターへの需要を煽っています。

- 製造業へのIoTとスマートテクノロジーの導入は、施設運営に革命をもたらしています。リアルタイムの監視、診断、遠隔制御機能を備えたスマートモータースターターが人気を集めています。これらの進歩は、運転効率と予知保全を強化し、市場を促進しています。

- メーカー各社は、用途や運転条件に合わせてカスタマイズされたモータースターターを求めるようになっています。この需要により、モータースタータメーカーとエンドユーザーとの間で、独自の性能基準に適合するソリューションを作り上げることを目的とした協力的な取り組みが促進されています。

- メーカーが設備を近代化するにつれて、モータースターターを含むオートメーション機器への資本支出が顕著に増加しています。FREDのデータはこの動向を浮き彫りにしています。米国の新規製造施設に対する建設投資総額は、2023年に記録的な1,930億米ドルに急増し、2022年の1,243億米ドルから大きく飛躍しました。

- インフレ削減法(IRA)、超党派インフラ法(BIL)、CHIPS・科学法(CHIPS法)などの立法措置が、米国における半導体、電気自動車(EV)バッテリー、風力タービンをはじめとする国内製造業への投資を促進しています。この投資の勢いは米国にとどまらず、新興国でも工業化が急速に進んでおり、モータースターターの需要急増に貢献しています。

高い成長率が期待されるアジア太平洋地域

- 中国やインドのような国々では急速な工業化と都市拡大が進んでおり、複数のセクターでモータースタータの需要が高まっています。これらの産業が都市部のニーズに応えるために事業を拡大するにつれて、効率的なモーター制御システムの重要性がますます明らかになっています。

- アジア太平洋地域は、特にエレクトロニクス、自動車、機械分野の世界の製造拠点です。インド、中国、日本、東南アジア諸国のような主要企業が存在するこの地域の成長は、製造工程中の電気モーターの制御に不可欠なモータースターターの需要を促進しています。

- インドの製造業セクターは、投資の大幅な急増を目の当たりにしており、同国の経済発展において極めて重要な局面を迎えています。Colliers社のレポートによると、インドの製造業市場は2025-26年までに1兆米ドルの大台に乗ろうとしています。グジャラート州がトップランナーとして台頭し、インドの製造業大国としての地位を確立しつつあります。

- 自動車産業は、特に中国と日本で活況を呈しており、インドも大きく躍進していることから、電気自動車用モーター・スターターの需要に拍車をかけています。さらに、都市化と人口の増加に伴い、水処理施設のニーズが高まっており、ポンプや制御システムにおける信頼性の高いモータースタータの需要が高まっています。

- 中国の国家開発改革委員会によると、中国の汚泥量は2025年までに9,000万トンに達する可能性があります。専門家は、2021年から2025年にかけて、中国の汚泥処理施設の新設に約80億米ドルが投資されると予測しています。汚染レベルが上昇していることから、インドもこれに続くと予想されています。このような動向から、この地域のモータースターター市場は大きく成長する見込みです。

モータースターター業界の概要

市場競争は激しく、多国籍大企業と地域プレーヤーが混在しています。この情勢は、急速な技術進歩、戦略的提携、そして製品のカスタマイズ、エネルギー効率の向上、スマートテクノロジーの統合によって際立つ企業への差し迫ったニーズによって特徴付けられています。

この分野で著名なプレーヤーには、シュナイダーエレクトリック、シーメンスAG、ABB社、イートン社などがあります。これらの企業は、モータースタータ技術の開拓と改良に重点を置き、研究開発に投資しています。過負荷保護、サーマルモニタリング、スマートコネクティビティ、リアルタイム診断などの機能は、この競争市場で極めて重要な差別化要因として浮上しています。

インダストリー4.0が勢いを増す中、IoT機能、リアルタイム・モニタリング、予知保全をシームレスに製品に織り込んだ企業は、自動化されたデジタル・ソリューションを熱望する顧客を引き付ける態勢を整えています。さらに、特定の業界の明確な要件に対応するオーダーメイドのモータースターターを提供することで、顧客との関係を深めることができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19パンデミックの後遺症とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 産業オートメーションの成長

- エネルギー効率規制

- 市場抑制要因

- 可変周波数ドライブ(VFD)との競合

第6章 市場セグメンテーション

- タイプ別

- ダイレクトオンラインスターター

- ステータ抵抗スタータ

- スリップリングスタータ

- オートトランスフォーマースタータ

- スターデルタスターター

- ソフトスタータ

- 定格電力別

- 5 kW未満

- 5-50 kW

- 50 kW以上

- 業界別

- 製造業

- 石油・ガス

- 鉱業

- 上下水道治療

- 自動車

- 飲食品

- 建築・建設

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Schneider Electric SE

- Seimens AG

- ABB Group

- Eaton Corporation

- Rockwell Automation

- Mitsubishi Electric Corporation

- Fuji Electric FA Components & Systems Co. Ltd

- Toshiba Corporation

- Larsen & Toubro Limited

- WEG SA

- W.W. Grainger Inc.

- Danfoss

第8章 投資分析

第9章 市場の将来

目次

The Motor Starter Market size is estimated at USD 6.50 billion in 2025, and is expected to reach USD 8.70 billion by 2030, at a CAGR of 6% during the forecast period (2025-2030).

Key Highlights

- In response to growing environmental concerns, industries are increasingly adopting energy-efficient motor starters, like soft starters, to reduce energy consumption and extend motor lifespan. Concurrently, the rise of the Internet of Things (IoT) has spurred the creation of intelligent motor starters, enabling remote monitoring and control, thus evolving the market.

- The global shift toward electric vehicles (EVs) has heightened the demand for sophisticated motor control solutions, including motor starters in automotive applications. In EVs, motor starters collaborate with battery management systems to optimize performance and ensure safety. As countries pivot from internal combustion engines to EVs across the world, the demand for motor starters is projected to surge.

- Recent innovations in the motor starter market have introduced products with advanced features like overload protection, thermal monitoring, and programmable settings, boosting reliability and performance. Manufacturers are broadening their product lines to encompass motor starters tailored to various voltage levels, power ratings, and industry-specific needs.

- The motor starter market is fiercely competitive, with many manufacturers competing for a market share. This intense competition often results in pricing pressures and challenges in product differentiation.

- Macroeconomic trends, particularly robust economic growth in emerging markets, fuel the demand for motor starters in the manufacturing and construction sectors. Additionally, tightening regulations on energy efficiency and environmental sustainability are influencing market dynamics. Nevertheless, the market is poised for continued growth.

Motor Starter Market Trends

The Manufacturing Sector is Expected to Drive the Market's Growth

- The transition to Industry 4.0 has spurred the widespread adoption of automation technologies in manufacturing. Factories are deploying advanced robotics and automated systems, necessitating efficient motor control. This evolution fuels the demand for sophisticated motor starters capable of managing diverse loads and enhancing overall performance.

- The infusion of IoT and smart technologies into manufacturing is revolutionizing facility operations. Smart motor starters, equipped with real-time monitoring, diagnostics, and remote control features, are gaining traction. These advancements bolster operational efficiency and predictive maintenance, propelling the market.

- Manufacturers are increasingly seeking customized motor starters specifically designed for distinct applications and operating conditions. This demand has fostered collaborative initiatives between motor starter producers and end users, aiming to craft solutions that align with unique performance standards.

- With manufacturers modernizing their facilities, there has been a notable uptick in capital expenditure on automation equipment, including motor starters. Data from FRED highlights this trend: total construction investment in new manufacturing facilities in the United States soared to a record USD 193 billion in 2023, a significant leap from USD 124.3 billion in 2022.

- Legislative measures like the Inflation Reduction Act (IRA), Bipartisan Infrastructure Law (BIL), and CHIPS and Science Act (CHIPS Act) are catalyzing investments in domestic manufacturing sectors, notably semiconductors, electric vehicle (EV) batteries, and wind turbines in the United States. This investment momentum is not confined to the United States, with emerging economies witnessing rapid industrialization, contributing to the surging demand for motor starters.

Asia-Pacific is Expected to Witness a High Growth Rate

- Countries like China and India are witnessing rapid industrialization and urban expansion, leading to a heightened demand for motor starters across multiple sectors. As these industries scale operations to cater to urban needs, the importance of efficient motor control systems becomes increasingly evident.

- Asia-Pacific is a global manufacturing hub, especially in the electronics, automotive, and machinery sectors. With key players like India, China, Japan, and several Southeast Asian nations, the region's growth propels the demand for motor starters, which are vital for controlling electric motors during manufacturing processes.

- The Indian manufacturing sector is witnessing a significant surge in investments, marking a pivotal moment in the country's economic journey. A report by Colliers highlights that the Indian manufacturing market is on track to hit the USD 1 trillion mark by 2025-26. Gujarat is emerging as the frontrunner, establishing itself as India's manufacturing powerhouse, closely trailed by Maharashtra and Tamil Nadu, which are expected to make substantial contributions to the market.

- The automotive industry, particularly booming in China and Japan, with India making significant strides, is fueling the demand for motor starters in electric vehicles. Furthermore, as urbanization and population grow, there is a rising need for water treatment facilities, underscoring the demand for dependable motor starters in pumps and control systems.

- According to the PRC's National Development and Reform Commission, China's sludge volume could hit 90 million tons by 2025. Experts project an investment of around USD 8 billion in new sludge processing facilities in China from 2021 to 2025. Given the escalating pollution levels, India is anticipated to follow suit. With such trends, the motor starter market in the region is poised for significant growth.

Motor Starter Industry Overview

The market is fiercely competitive, featuring a blend of large multinational corporations and regional players. This landscape is marked by rapid technological advancements, strategic collaborations, and a pressing need for companies to stand out through product customization, enhanced energy efficiency, and the integration of smart technologies.

Prominent players in the arena include Schneider Electric, Siemens AG, ABB Ltd, and Eaton Corporation. These companies are channeling investments into R&D, focusing on pioneering and refining motor starter technologies. Features like overload protection, thermal monitoring, smart connectivity, and real-time diagnostics have emerged as pivotal differentiators in this competitive market.

As Industry 4.0 gains momentum, companies that seamlessly weave in IoT capabilities, real-time monitoring, and predictive maintenance into their offerings are poised to attract a clientele eager for automated and digital solutions. Furthermore, companies can foster deeper relationships with their clients by providing tailored motor starters that address the distinct requirements of specific industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of the Aftereffects of the COVID-19 Pandemic and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Industrial Automation

- 5.1.2 Energy Efficiency Regulation

- 5.2 Market Restraints

- 5.2.1 Competition From Variable Frequency Drives (VFDs)

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Direct-on-Line Starter

- 6.1.2 Stator Resistance Starter

- 6.1.3 Slip Ring Starter

- 6.1.4 Auto Transformer Starter

- 6.1.5 Star Delta Starter

- 6.1.6 Soft Starter

- 6.2 By Power Rating

- 6.2.1 Up to 5 kW

- 6.2.2 5 - 50 kW

- 6.2.3 Above 50 kW

- 6.3 By End-user Vertical

- 6.3.1 Manufacturing

- 6.3.2 Oil and Gas

- 6.3.3 Mining

- 6.3.4 Water and Wastewater Treatment

- 6.3.5 Automotive

- 6.3.6 Food and Beverage

- 6.3.7 Building and Construction

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Seimens AG

- 7.1.3 ABB Group

- 7.1.4 Eaton Corporation

- 7.1.5 Rockwell Automation

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Fuji Electric FA Components & Systems Co. Ltd

- 7.1.8 Toshiba Corporation

- 7.1.9 Larsen & Toubro Limited

- 7.1.10 WEG SA

- 7.1.11 W.W. Grainger Inc.

- 7.1.12 Danfoss

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日