掘削オートメーション:市場シェア分析、産業動向、成長予測(2025~2030年)

Drilling Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1630450

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

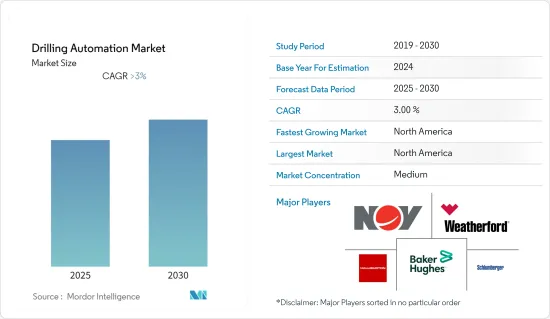

掘削オートメーション市場は予測期間中に3%を超えるCAGRで推移すると予想されます。

市場は、原油価格の暴落によるCOVID-19の発生によってマイナスの影響を受けました。現在、市場は流行前のレベルに達しています。

主要ハイライト

- 深度の増加や複数の水平坑井の使用による坑井の複雑化、リグ数の増加、天然ガス生産量の増加などの要因が市場を牽引すると予想されます。

- しかし、原油・天然ガスの変動が市場の成長を抑制すると予想されます。

- ガスハイドレート生産は、経済的に実行可能なその生産が、より優れた掘削オートメーション技術を必要とする新たな問題を引き起こす可能性があるため、市場参入企業にとって好機となる可能性があります。

- シェールオイル・ガスの生産量が多いことから、予測期間中は北米が最大の市場になると予想され、需要の大部分は米国とカナダからもたらされます。

掘削オートメーション市場の動向

オフショアセグメントが著しい成長を遂げる

- 掘削オートメーションは、石油・ガス井の実際の掘削に必要なダウンホール活動が中心です。これには、掘削プロセスの安全性と効率を向上させるために、地表と坑内の測定値をほぼリアルタイムの予測モデルとリンクさせることが含まれます。オフショアセグメントでは、水面下でドリルを操作するために先進的専門知識が必要とされるため、掘削オートメーションがその信頼性を証明し、市場の成長を刺激する可能性があります。

- 技術は絶え間なく改良されているが、石油・ガス掘削産業にパラダイム・シフトを起こすことが期待されています。環境と個人の安全に対する懸念は、技術の大規模な運用化によって緩和されることが期待され、特に安全が重要な関心事であるオフショアセグメントでは、市場の成長を助けると予想されます。

- 2022年1月、ADNOCはウムシャイフ油田の長期開発に10億米ドルを投資すると発表しました。その過程で同社は、同鉱区の開発、効率性の向上、長期的なポテンシャルの強化を目的とした契約をNational Petroleum Construction Companyに発注しました。この投資は、2030年までに日量500万バレルの生産能力計画を達成するというADNOCの目標に沿ったものです。

- 非在来型の陸上生産が大きく伸びているが、2021年の石油・ガス生産全体の約28%を占めるのは海上生産です。炭化水素資源に対する需要の増加により、石油・ガスの海洋生産は増加すると予想されます。オフショア部門の増加が市場の成長に寄与すると予想されます。

- 世界の天然ガス生産量は、2020年の3兆8,615億立方メートルから2021年には4.8%増の4兆369億立方メートルに増加しました。天然ガスの有用性が高まったことで、世界の消費量を満たすために天然ガス生産量の増加が命じられました。

- したがって、オフショアセグメントは、フリーキャッシュフローの増加、技術の進歩、石油生産の増加により、予測期間中に成長を示すと予想されます。

北米が市場を独占する

- 北米地域は、最大の掘削オートメーション市場の1つであり、今後数年間もその優位性を維持すると予想されます。この地域は、世界最大の石油・ガス生産盆地から成り、産業のさらなる成長のための肥沃な土壌を提供しています。

- 米国は、掘削オートメーション市場の進歩に貢献したパーミアン盆地のような多くの陸上盆地でのシェール石油・ガスブームにより、この地域で最大の掘削オートメーションユーザーになると予想されます。シェールオイル・ガスは同国で着実に増加しており、シェール盆地でのマルチラテラル水平掘削における掘削オートメーションを増加させる基盤を提供する可能性があります。

- 北米の原油生産量は2020年の10億5,870万トンから2021年には10億7,470万トンと大幅に増加しました。一方、同地域のガス生産量は2020年の1兆1,121億立方メートルから2021年には1兆1,358億立方フィート/日に増加しました。石油・ガス生産の増加は、より優れた掘削オートメーション技術に対する需要を生み出し、それによって市場の成長を助けると予想されます。

- 2023年3月現在、米国では合計755基のロータリーリグが稼動しています。ロータリリグは、1週間の大半(7日のうち4日)を掘削している場合、稼動しているとみなされます。これは、同国の上流セグメントにおいて、掘削リグや生産プラットフォームなどの固定資産が優位を占めていることを示しています。

- したがって、北米地域は、その広大な原油・天然ガス上流部門、海洋産業における探査の高まり、化石燃料の需要増加により、市場を独占すると予想されます。

掘削オートメーション産業概要

掘削オートメーション市場は、部分的にセグメント化されています。この市場の主要企業(順不同)には、Schlumberger Limited、Halliburton Company、Baker Hughes Company、Weatherford International PLC、National-Oilwell Varco, Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 展開場所

- オンショア

- オフショア

- 地域

- 北米

- アジア太平洋

- 欧州

- 南米

- 中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Weatherford International plc

- National-Oilwell Varco Inc.

- Baker Hughes Company

- Schlumberger Ltd

- Halliburton Company

- Superior Energy Services, Inc.

- Sekal AS

- MHWirth

第7章 市場機会と今後の動向

目次

The Drilling Automation Market is expected to register a CAGR of greater than 3% during the forecast period.

The market was negatively impacted by the outbreak of COVID-19 due to the crude oil price crash. Currently, the market has reached pre-pandemic levels.

Key Highlights

- Factors such as an increase in the complexity of the wellbore due to increased depth and the use of multiple horizontal wells, an increase in the number of rigs, and rising production of natural gas are expected to drive the market.

- However, the volatility of crude oil and natural gas is expected to restrain the market's growth.

- Gas hydrate production may become an opportunity for market players as its economically viable production may pose new problems that may require better drilling automation techniques.

- Due to the high output of shale oil and gas, North America is expected to be the largest market during the forecast period, with the majority of demand coming from the United States and Canada.

Drilling Automation Market Trends

Offshore Segment to Witness Significant Growth

- Drilling automation is centered on the downhole activities necessary for the actual drilling of an oil or gas well. This involves linking surface and downhole measurements with near-real-time predictive models to improve the safety and efficiency of the drilling process. In the offshore segment, a high level of expertise is required to maneuver the drill below the surface, and therefore, drill automation may prove its reliability, which may stimulate the growth of the market.

- Although technology is being continuously refined, it is expected to create a paradigm shift in the oil and gas drilling industry. Concerns over the environment and safety of individuals are expected to be mitigated with the large-scale operationalization of the technology, which is expected to aid the growth of the market, especially in the offshore segment where safety is a significant concern.

- In January 2022, ADNOC announced an investment of USD 1 billion in the long-term development of the Umm Shaif field. In the process, the company awarded National Petroleum Construction Company a contract to develop, increase efficiencies, and enhance the field's long-term potential. This investment aligns with ADNOC's aims to achieve production capacity plans of 5 million barrels per day by 2030.

- Although significant growth has taken place in unconventional onshore production, offshore production represented approximately 28% of overall oil and gas production in 2021. Offshore production of oil and gas is expected to increase due to the increasing demand for hydrocarbon resources. An increase in the offshore sector is expected to contribute to the growth of the market.

- The amount of natural gas produced in the world increased by 4.8%, to 4036.9 billion cubic meters in 2021 from 3861.5 billion cubic meters in 2020. The increased utility of natural gas has ordained an increase in natural gas production to meet the world's consumption.

- Hence, the offshore segment is expected to witness growth in the forecast period due to an increase in free cash flow, advancements in technology, and an increase in oil production.

North America to Dominate the Market

- The North American region is expected to be among the largest drilling automation markets and is likely to continue its dominance in the coming years. The region consists of the largest oil and gas production basins in the world, which provide fertile ground for further growth in the industry.

- The United States is expected to be the largest user of drilling automation in the region, especially with the boom in shale oil and gas in many onshore basins like the Permian basin that has contributed to advancements in the drilling automation market. Shale oil and gas have steadily increased in the country and may provide a platform for increasing drilling automation in multilateral horizontal drilling in the shale basins.

- North America increased its output of crude oil significantly to 1074.7 million tons in 2021 from 1058.7 million tons in 2020. Whereas the region's gas production increased from 1112.1 billion cubic meters in 2020 to 1135.8 billion cubic feet per day in 2021. Increasing production of oil and gas is expected to create demand for better drilling automation techniques and thereby aid the growth of the market.

- As of March 2023, the United States had a total of 755 active rotary rigs. A rotary rig is considered active when it is on location and drilling the majority of the week (4 days out of 7 days). This indicates the dominance of fixed assets such as drilling rigs and production platforms in the upstream segment of the country.

- Hence, the North America region is expected to dominate the market due to its vast crude oil and natural gas upstream sector, rising exploration in the offshore industry, and increasing demand for fossil fuels.

Drilling Automation Industry Overview

The drilling automation market is partially fragmented. Some of the key players in this market (in no particular order) are Schlumberger Limited, Halliburton Company, Baker Hughes Company, Weatherford International PLC, National-Oilwell Varco, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Asia-Pacific

- 5.2.3 Europe

- 5.2.4 South America

- 5.2.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Weatherford International plc

- 6.3.2 National-Oilwell Varco Inc.

- 6.3.3 Baker Hughes Company

- 6.3.4 Schlumberger Ltd

- 6.3.5 Halliburton Company

- 6.3.6 Superior Energy Services, Inc.

- 6.3.7 Sekal AS

- 6.3.8 MHWirth

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日