|

|

市場調査レポート

商品コード

1630330

Roll to Rollフレキシブルエレクトロニクス:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Roll To Roll Flexible Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| Roll to Rollフレキシブルエレクトロニクス:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 104 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

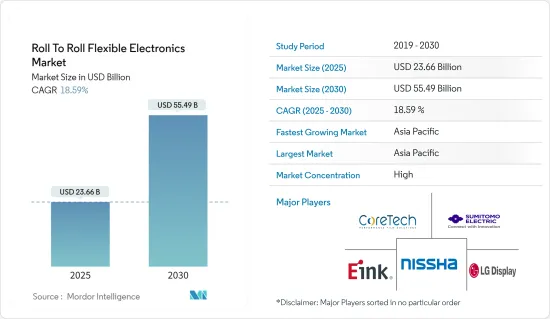

Roll to Rollフレキシブルエレクトロニクスの市場規模は、2025年に236億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは18.59%で、2030年には554億9,000万米ドルに達すると予測されます。

Roll to Roll(R2R)プリント・フレキシブル回路は、従来のリジッド回路の適合性とスペースの制約に対処します。適応可能な基板上に構築されたR2Rフレキシブル回路は、特に今日のスペース制限を考慮すると、電子機器設計においてますます重要性を増しています。その結果、メーカー各社は、民生用電子機器におけるこれらの回路に対する需要の急増に対応するため、よりコンパクトなデバイスを製造しています。これらの回路は、その機能を損なうことなく曲げたりねじったりすることができるため、最新の電子機器に最適です。

Roll to Roll(R2R)フレキシブルエレクトロニクス市場の主な促進要因には、エネルギー効率が高く、薄型でフレキシブルコンシューマーエレクトロニクスを求める動きや、電子部品の生産におけるR2R印刷の顕著なコストメリットなどがあります。フレキシブルエレクトロニクスの採用はヘルスケア・アプリケーションで増加しています。これらのアプリケーションは、ウェアラブル健康モニターからフレキシブル医療センサーまで幅広く、さまざまな分野におけるR2R技術の汎用性と重要性の高まりを浮き彫りにしています。

手頃な価格のモデルやインターネットアクセスの普及に牽引されたスマートフォンの世界の普及の急増は、Roll to Rollフレキシブルエレクトロニクス市場の主な起爆剤となっています。人口が急増し、可処分所得が増加している中国やインドなどの国々は、スマートフォンの分野で支配的なプレーヤーとして台頭しつつあります。これらの地域ではスマートフォンの普及が進んでおり、メーカーが高度な機能をデバイスに組み込もうとしているため、フレキシブルエレクトロニクスの需要が大幅に伸びると予想されます。

しかし、研究開発(R&D)とインフラの要件が高いため、Roll to Roll(R2R)ベースのフレキシブルエレクトロニクス需要の伸びを抑制する課題がいくつかあります。研究開発とインフラ整備に多額の初期費用がかかるため、企業や消費者を含む潜在的な採用企業は、フレキシブルエレクトロニクス技術への投資を躊躇してしまいます。このような消極的な姿勢は、投資収益率(ROI)や初期展開の手ごろさに対する懸念から生じています。

COVID-19パンデミック後の通信機器、デジタル化動向、スマートビルディング、ADASベースの自動車、インダストリー4.0などの出現がスマートエレクトロニクス、IIOTs、通信機器の需要を高め、市場成長を後押ししています。

そのため、パンデミック後のインターネット普及の拡大や自動化動向に伴う電子デバイスの需要が、調査対象市場の成長を支えています。

Roll to Rollフレキシブルエレクトロニクス市場動向

コンシューマーエレクトロニクスが大きな成長を遂げる

- 消費者は、スリムで軽量、持ち運び可能な機器をますます好むようになっています。そのため、スマートフォン、タブレット端末、ウェアラブル端末などでは、軽量でフレキシブルなエレクトロニクスへのニーズが高まっています。その結果、こうした仕様を実現するため、メーカーは電子部品をコスト効率よく、柔軟に、大規模に製造できるR2Rプリンティングに移行しつつあります。

- 手ごろな価格のモデルやインターネットアクセスの普及に後押しされたスマートフォンの世界の普及の急増は、Roll to Rollフレキシブルエレクトロニクス市場の主な触媒となっています。人口が急増し、可処分所得が増加している中国やインドなどの国々は、スマートフォンの分野で支配的なプレーヤーとして台頭しつつあります。これらの地域ではスマートフォンの普及が進んでおり、メーカーが先進的な機能をデバイスに組み込もうとしているため、フレキシブルエレクトロニクスの需要が大幅に伸びると予想されます。

- コンシューマー・エレクトロニクスの小型化動向は、R2Rプリンティング・エレクトロニクスの採用を大きく後押ししています。デバイスが小型化し、携帯性が向上するにつれて、メーカーは部品や機能を縮小生産できる製造方法を求めており、R2Rプリンティングは薄型で柔軟性があり、軽量な電子部品の生産を可能にします。製造コストの低減と材料廃棄物の削減が、家電メーカーのR2Rプリンティング採用を後押ししています。

- 民生用電子機器の技術動向は、R2Rフレキシブル電子機器の需要を加速させています。ウェアラブル機器や折りたたみ式スマートフォンの人気が高まっているため、これらの機器にシームレスに統合できるフレキシブル・ディスプレイやその他の部品が必要とされています。さらに、電子機器の超薄型・軽量化の動向は、メーカーが新しい材料や製造プロセスを模索し、家電製品向けのR2Rフレキシブルエレクトロニクスに対応することを後押ししています。

大きな成長を記録するアジア太平洋地域

- アジア太平洋地域のRoll to Rollフレキシブルエレクトロニクス市場では、ベンダーが研究開発を重視し、業界内でパートナーシップを結び、潜在的な製造機会を狙っています。このような提携により、産業パートナーは新製品の少量生産を試行することができ、リスクを最小限に抑えることができます。

- 中国のフレキシブルエレクトロニクス部門は、世界な舞台でフォロワーから圧倒的なリーダーへと変貌を遂げました。新たなチャンスを生かすため、ベンダーは戦略的に産業レイアウトに注力し、「チャイナ・カーボン・バレー」と呼ばれる産業基盤を構想しています。各ベンダーの取り組みは、コア技術の研究、フレキシブルエレクトロニクスの革新と開発、革新的な潜在能力をフルに活用するための人材育成への投資など多岐にわたる。

- インドでは、表面コーティング分野のRK PrintCoat Instruments UKが、インド工科大学カーンプル校(IITK)の国立フレキシブルエレクトロニクス・センター(FlexEセンター)と提携しました。両者の協力は、フレキシブルエレクトロニクスの研究開発とプロトタイピングに対応する、特殊なRoll to Roll(R2R)パイロット・ラインの設計、製造、供給に焦点を当てています。

- オーストラリア先端太陽光発電センター(Australian Center for Advanced Photovoltaics)は、太陽エネルギーの進化に注目しています。従来のパネルや電池がその重要性を維持する一方で、今後20年間は太陽光発電技術の飛躍的な進歩が期待されます。薄くてフレキシブルなフィルムやソーラー・ウィンドウのような革新的技術が登場します。2050年までのオーストラリアのネットゼロ目標に沿うためには、太陽光発電部門は2030年までに電力需要の20%から40%に倍増し、2050年までに再生可能エネルギー100%を目指す必要があります。

Roll to Rollフレキシブルエレクトロニクス業界の概要

Roll to Rollフレキシブルエレクトロニクス市場はまだ黎明期にあるため、直接的な競争企業間の敵対関係はないです。技術に投資している企業のほとんどは、異なる領域や産業をターゲットにしています。したがって、調査対象市場における競争企業間の敵対関係を読み解くのはまだ早いです。

製造施設の建設と生産開始に必要な投資が高額なため、新規参入業者の脅威は低いと推定されます。これらの製品はさまざまな電子部品のサイズとコストの削減に役立つため、世界中の政府政策がこの産業を支援しています。

このため、新規参入者はこの機会を利用して市場に参入し、存在感を示そうとします。しかし、スイッチング・コストには大きなものがあり、その後、新規参入者がそれを取り除く手段を作り出すことができない場合もあります。Roll to Rollフレキシブルエレクトロニクスを生産する工場を設立するには、高度な製造機械と研究開発資源が必要なため、莫大な費用がかかります。そのため、新規事業が市場に参入するのは非常に難しいです。

技術に対する認識や専門知識が低いという現状も、この市場に投資する新規参入企業の数を制限しています。しかし、Roll to Rollフレキシブルエレクトロニクス技術の潜在市場は巨大であるため、商業化の進展に伴い、新規参入業者の脅威は高まると予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19とマクロ経済動向の市場への影響分析

- 技術スナップショット(印刷技術)

第5章 市場力学

- 市場促進要因

- IoTアプリケーションにおけるフレキシブル電子部品の展開

- 軽量、機械的柔軟性、コスト効率に優れた製品へのニーズの高まり

- 市場の課題/抑制要因

- 研究開発(R&D)とインフラに必要な資本の高さ

第6章 市場セグメンテーション

- 用途別

- センサー

- ディスプレイ

- 電池

- 太陽電池

- エンドユーザー産業別

- コンシューマー・エレクトロニクス

- 自動車・輸送機器

- ヘルスケア

- 航空宇宙・防衛

- その他エンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- E Ink Holdings Inc.

- Nissha GSI Technologies Inc.

- CoreTech Films(Saint-Gobain High Performance Solutions)

- LG Display Co. Ltd

- Sumitomo Electric Industries Inc.

- Zinergy

- Fujikura Ltd

- Multek Corporation

- Ynvisible Interactive Inc.

第8章 投資分析

第9章 市場機会

The Roll To Roll Flexible Electronics Market size is estimated at USD 23.66 billion in 2025, and is expected to reach USD 55.49 billion by 2030, at a CAGR of 18.59% during the forecast period (2025-2030).

Roll-to-roll (R2R) printed flexible circuits address the conformability and space constraints of traditional rigid circuits. These R2R flexible circuits, built on adaptable substrates, are increasingly pivotal in electronic device design, especially given today's space limitations. As a result, manufacturers are crafting more compact devices to meet the surging demand for these circuits in consumer electronics. The ability to bend and twist these circuits without compromising their functionality makes them ideal for modern electronic devices.

Key drivers of the roll-to-roll (R2R) flexible electronics market include the push for energy-efficient, thin, and flexible consumer electronics and the notable cost benefits of R2R printing in producing electronic components. The adoption of flexible electronics is rising in healthcare applications. These applications range from wearable health monitors to flexible medical sensors, highlighting the versatility and growing importance of R2R technology in various sectors.

The global surge in smartphone adoption, driven by affordable models and widespread internet access, is a primary catalyst for the roll-to-roll flexible electronics market. Countries like China and India, with their burgeoning populations and rising disposable incomes, are emerging as dominant players in the smartphone arena. The increasing penetration of smartphones in these regions is expected to drive significant growth in the demand for flexible electronics as manufacturers seek to incorporate advanced features into their devices.

However, the high requirement for research and development (R&D) and infrastructure poses several challenges restraining the demand growth for roll-to-roll (R2R) based flexible electronics. The significant upfront costs of R&D and infrastructure development deter potential adopters, including businesses and consumers, from investing in flexible electronics technologies. This reluctance stems from concerns over return on investment (ROI) and the affordability of initial deployment.

The demand for communication devices, digitalization trends, and the emergence of smart buildings, ADAS-based automobiles, Industry 4.0, and others after the COVID-19 pandemic have raised the growth of smart electronics, IIOTs, and communication devices, which have fueled the market growth.

Therefore, the demand for electronic devices, in line with the growth of Internet penetration and automation trends in the post-pandemic period, has supported the growth of the studied market.

Roll To Roll Flexible Electronics Market Trends

Consumer Electronics to Witness Major Growth

- Consumers increasingly prefer devices that are slim, lightweight, and portable. Thus, the need for lightweight, flexible electronics has increased for devices like smartphones, tablets, and wearables. As a result, to obtain these specifications, manufacturers are shifting to R2R printing, which enables them to manufacture electronic components cost-effectively, flexibly, and on a larger scale.

- The global surge in smartphone adoption, driven by affordable models and widespread internet access, is a primary catalyst for the roll-to-roll flexible electronics market. Countries like China and India, with their burgeoning populations and rising disposable incomes, are emerging as dominant players in the smartphone arena. The increasing penetration of smartphones in these regions is expected to drive significant growth in the demand for flexible electronics as manufacturers seek to incorporate advanced features into their devices.

- The trend toward miniaturization in consumer electronics has significantly driven the adoption of R2R printing electronics. As devices become smaller and more portable, manufacturers are seeking manufacturing methods that can produce components and features on reduced scales, where R2R printing allows the production of thin, flexible, and lightweight electronic components. The lower manufacturing cost and reduced material waste have driven R2R printing adoption among consumer electronics manufacturers.

- Technological trends in consumer electronics are accelerating the demand for R2R flexible electronics. The increasing popularity of wearable devices and foldable smartphones requires flexible displays and other components that can be integrated seamlessly into these devices. In addition, the trend toward ultra-thin and lightweight electronics is pushing manufacturers to explore new materials and manufacturing processes and cater to R2R flexible electronics for consumer electronics products.

Asia-Pacific to Register Major Growth

- In the Asia-Pacific roll-to-roll flexible electronics market, vendors are emphasizing R&D, forging partnerships within the industry, and eyeing potential manufacturing opportunities. Such collaborations enable industrial partners to trial low-volume manufacturing of new products, minimizing risks.

- China's flexible electronics sector has transitioned from being a follower to a dominant leader on the global stage. To capitalize on emerging opportunities, vendors are strategically focusing on industrial layouts, laying the groundwork for the envisioned "China Carbon Valley" industrial base. Their efforts encompass core technology research, innovation and development in flexible electronics, and investing in personnel training to harness the full innovative potential.

- In India, RK PrintCoat Instruments UK, a player in the surface coating domain, teamed up with the National Centre of Flexible Electronics (FlexE Centre) at the Indian Institute of Technology, Kanpur (IITK). Their collaboration focuses on designing, manufacturing, and supplying a specialized roll-to-roll (R2R) pilot line, catering to R&D and prototyping in flexible electronics.

- The Australian Center for Advanced Photovoltaics highlights the evolving landscape of solar energy. While traditional panels and batteries will maintain their significance, the next two decades promise breakthroughs in PV technology. Innovations like thin, flexible films and solar windows are on the horizon. To align with Australia's net-zero goal by 2050, the solar sector must double its contribution from 20% to 40% of electricity demand by 2030, aiming for a 100% renewable target by 2050.

Roll To Roll Flexible Electronics Industry Overview

There is no direct competitive rivalry, as the roll-to-roll flexible electronics market is still in the nascent stage. Most of the companies that have invested in technology are targeting different domains and industries. Therefore, it is early to decipher the competitive rivalry in the studied market.

Due to the high investments required to construct a manufacturing facility and initiate production, the threat of new entrants is estimated to be low. Government policies across the world support this industry, as these products help reduce the sizes and costs of various electronic components.

This encourages new entrants to use the opportunity to enter the market and mark their presence. However, there are significant switching costs, and subsequently, a new entrant may not be able to create a means to remove them. It costs a lot of money to set up a plant to produce roll-to-roll flexible electronics because it needs sophisticated manufacturing machinery and R&D resources. This makes it very difficult for new businesses to enter the market.

The current low state of technology awareness and expertise is also limiting the number of new players making investments in the market. However, the potential market is massive for roll-to-roll flexible electronics technology; hence, with rising commercialization, the threat of new entrants is expected to grow.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/ Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact Analysis of COVID-19 and Macroeconomic Trends on the Market

- 4.4 Technology Snapshot (Printing Technologies)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Deployment of Flexible Electronic Components in IoT Applications

- 5.1.2 Emerging Need for Lightweight, Mechanically Flexible, and Cost-effective Products

- 5.2 Market Challenges/restraints

- 5.2.1 High Capital Requirement for Research and Development (R&D) and Infrastructure

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Sensors

- 6.1.2 Displays

- 6.1.3 Batteries

- 6.1.4 Photovoltaics Cells

- 6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive and Transportation

- 6.2.3 Healthcare

- 6.2.4 Aerospace and Defense

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 E Ink Holdings Inc.

- 7.1.2 Nissha GSI Technologies Inc.

- 7.1.3 CoreTech Films (Saint-Gobain High Performance Solutions)

- 7.1.4 LG Display Co. Ltd

- 7.1.5 Sumitomo Electric Industries Inc.

- 7.1.6 Zinergy

- 7.1.7 Fujikura Ltd

- 7.1.8 Multek Corporation

- 7.1.9 Ynvisible Interactive Inc.