|

市場調査レポート

商品コード

1851086

基板ライクPCB:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Substrate-Like-PCB - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 基板ライクPCB:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月20日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

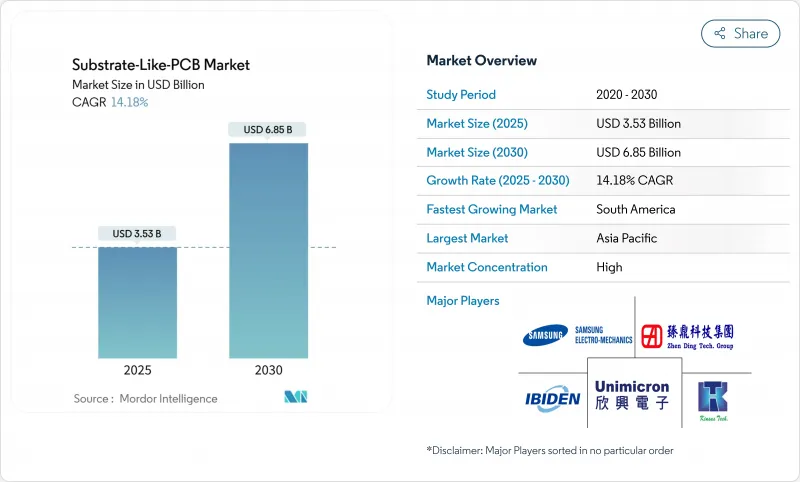

基板ライクPCB市場規模は2025年に35億3,000万米ドルに達し、2030年には68億5,000万米ドルに拡大すると予測され、CAGRは14.18%です。

OEMが従来の高密度相互接続基板から、半導体パッケージングに完全に移行せずにIC基板レベルの配線密度を実現するソリューションに移行するにつれて需要が加速します。数量成長は、シグナルインテグリティのために<=25µmライン/スペースジオメトリを必要とする5G無線、人工知能プロセッサ、車載ADASコントローラに集中しています。アジア太平洋は、半導体鋳造工場とPCBファブリケーター間の緊密な連携と、改良型セミアディティブ処理ラインへの持続的な投資により、2024年の売上高の69%を獲得しました。ABFビルドアップフィルムは低損失の誘電特性を強みに材料選択を支配しているが、供給基盤が集中しているため、ティアワン・ファブリケーターによる垂直統合の動きが活発化しています。25µm以下の歩留まり最適化は、AIを活用した検査に依存する傾向が強まっており、プロセス制御のリーダーは構造的なコスト優位性を獲得しています。米国国防総省の3,000万米ドルの助成金など、地政学的なリショアリングのインセンティブは、新規参入企業の資格要件を厳しくする一方で、地域の多様化をもたらします。

世界の基板ライクPCB市場の動向と洞察

スマートフォンOEMによる高密度相互接続の採用が急増

ベンダーは、Substrate-Like PCB市場技術を利用して回路密度を約30%向上させ、デバイスの厚さをフラットに保ちながら、5Gモデム、AIコプロセッサ、マルチレンズカメラ制御のためのスペースを拡大した。フラッグシップモデルからのスケールメリットは中位機種の携帯電話にも流れ込み、より幅広いポートフォリオで資本コストを償却する大量生産を維持します。

5G通信モジュールの需要増加

ミリ波ベースステーション・ボードや民生用5G無線カードでは、挿入損失やクロストークを抑制するために<=25µmの配線が必要です。ネットワークOEMは、マッシブMIMOアレイやビームフォーミングフロントエンド向けにSubstrate-Like PCB市場設計を指定し、基板密度とスペクトル効率目標をリンクさせます。同じ設計ルールは、期待されるデータレートが上昇するにつれて、スマートフォンやタブレットにも移行します。

SLP生産ラインの高CAPEX

グリーンフィールドのサブストレートライクPCB市場ラインは、精密レーザードリル、直接画像フォトリソグラフィ、クラス1000のクリーンルームスペースを必要とします。1億米ドルの出費は、小規模ファブリケーターにジョイントベンチャーの設立や撤退を迫り、バランスシートの厚みを誇る既存企業に生産能力を集約させる。

セグメント分析

スマートフォンは、2024年のSubstrate-Like PCB市場収益の47%を占め、2025年も引き続き主要顧客です。このセグメントは、世界の携帯電話出荷に内在するSubstrate-Like PCB市場規模の優位性を活用し、急速な生産能力増強を引き受ける。AIエンジンと5アンテナ5G無線を組み合わせたプレミアムデバイスは、<=25µm配線を必要とし、最先端での需要を強化します。その後、コスト曲線が連鎖的に変化することで、フラッグシップのリフレッシュを超えたボリューム可視性が拡大し、中位層の採用が可能になります。

ウェアラブルは、CAGR 15.4%で最も急成長しているニッチ分野であり、健康モニタリングの義務化と拡張現実ヘッドセットによって促進されます。サプライヤーは、高効率の電源管理ICを基板に直接組み込むことでエネルギー密度を最適化し、SLPの0.5mm以下のビアピッチの価値を証明しています。オートモーティブ・エレクトロニクスは、OEMが冗長センサー融合ボードを指定することで、収益源を多様化します。ネットワーキング・インフラとエッジコンピューティング・ゲートウェイは、熱とレイテンシの目標を達成するためにSLPを採用し、産業用システムと医療用システムは厳しい信頼性によりプレミアムASPを獲得しています。

10~12層は2024年の生産量の37%を占め、配線ヘッドルームと管理可能な歩留まりリスクのバランスをとっています。この層は、スマートフォン基板に関連するSubstrate-Like PCB市場規模の主力です。12層を超えるデザインは、チップレットベースのAIアクセラレータや車載ドメインコントローラを背景にCAGR13%で拡大しています。ここで、"Substrate-Like PCB市場シェア"は、連続したラミネーションサイクルで累積ワープ制御をマスターするファブリケータにもたらされます。レイヤ数は8-10で、コスト重視の消費者向けIoT製品に対応し、SLPに向けてスキルアップするHDIベンダーにエントリーパスを提供します。

基板ライクPCB市場は、アプリケーション別(スマートフォン、タブレット、ウェアラブル、カーエレクトロニクス、その他)、積層数別(8~10層、10~12層、その他)、基材別(ABF、変性エポキシ/FR-4、その他)、ライン/スペース解像度別(30/30mm、25/25mm、<=20/20mm)、地域別に分類されています。市場予測は金額(米ドル)で提供されます。

地域別分析

アジア太平洋地域は、台湾、韓国、日本を中心に、2024年の売上シェア69%を維持。鋳造に隣接したエコシステムは、PCBベンダーが半導体顧客からR&Dを共同利用することで、製造のための設計サイクルを加速させる。中国のファブリケーターは生産能力を積極的に拡大。Zhen Dingは2024年に23%のトップライン成長を記録し、2027年までのIC基板収益のCAGR50%に向けて舵を切っています。日本の材料メジャーはABFフィルムをこの地域に供給し、地域のサプライチェーン密度を強化しています。

北米の2024年の寄与率は18%だが、3,000万米ドルの国防資金とCHIPS法の優遇措置の恩恵を受けており、先進的なツーリング費用を負担しています。TTMテクノロジーズのシラキュース施設は1億3,000万米ドルで、北米大陸で最大の超HDI投資であり、セキュアサプライの防衛ワークロードをターゲットとしています。自動車の電動化とプライベートネットワーク5Gの展開は、この地域の需要に構造的な足かせを与えます。

欧州の小規模ながら戦略的なフットプリントはAT&Sが主導しており、ADASボードを必要とするドイツのOEMにサービスを提供するためにマレーシアでの生産を拡大した。技術主権をターゲットとするEUの助成金は、特に自動車と医療分野向けのSLPラインの増設を支援します。

南米は低水準からのスタートであったが、ニアショアリングによって軽組み立てがドミニカ共和国とメキシコにシフトし、CAGR12.2%を記録しました。政府は雇用創出のためにエレクトロニクスクラスターを推進し、自由貿易協定に沿ったパイロットSLP投資を誘致しています。

中東とアフリカはまだ発展途上だが、政府系多様化ファンドが半導体のバックエンドエコシステムに資本を投入することで、アップサイドを維持し、地域のデザインハウスが成熟すれば、将来のサブストレートライクPCB市場への浸透を可能にします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高密度相互接続に対するスマートフォンOEM採用の急増

- 5G通信モジュール需要の高まり

- ウェアラブルとIoTデバイスの小型化動向

- プリント基板の複雑化が進む車載ADASとEVエレクトロニクス

- 異種集積を可能にするSLP上のフリップチップ

- オンショア先端PCBファブへの政府補助金

- 市場抑制要因

- SLP製造ラインのCAPEXが高め

- <25mL/Sにおけるプロセス収率の課題

- 特殊ビルドアップ化学物質に関する環境規制

- ベンダーが限られることによるABF樹脂の供給リスク

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターズファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- ライバルの激しさ

- 業界バリューチェーン分析

第5章 市場規模と成長予測

- 用途別

- スマートフォン

- タブレット

- ウェアラブル

- カーエレクトロニクス

- ネットワークおよび通信インフラ

- IoT/エッジ・デバイス

- 産業用および医療用エレクトロニクス

- ビルドアップ層数別

- 8~10層

- 10~12層

- >12層

- 基材別

- ABF(味の素ビルドアップフィルム)

- 変性エポキシ/FR-4

- その他(PTFE、BTレジン)

- ライン/スペース解像度別

- 30/30µm

- 25/25µm

- 20/20µm

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Kinsus Interconnect Technology Corp.

- Ibiden Co., Ltd.

- Compeq Manufacturing Co., Ltd.

- Daeduck Electronics Co., Ltd.

- Unimicron Technology Corp.

- Zhen Ding Technology Holding

- TTM Technologies

- Meiko Electronics Co., Ltd.

- ATandS AG

- Korea Circuit Co., Ltd.

- LG Innotek Co., Ltd.

- Samsung Electro-Mechanics

- Shennan Circuits Co., Ltd.

- Tripod Technology

- Fujitsu Interconnect

- Wus Printed Circuit

- HannStar Board Corp.

- Nippon Mektron Ltd.

- NCAB Group AB

- Multek Ltd.