|

市場調査レポート

商品コード

1630251

ドイツの包装産業:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Germany Packaging Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツの包装産業:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 108 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

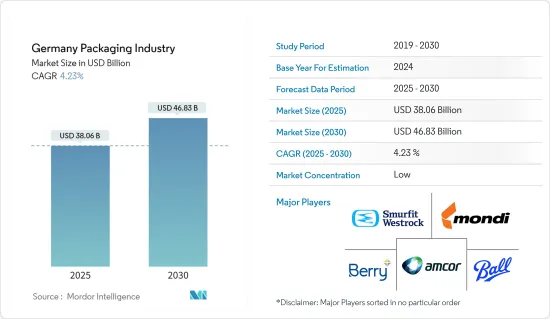

ドイツの包装産業の予測期間(2025~2030年)のCAGRは4.23%で、2025年の380億6,000万米ドルから2030年には468億3,000万米ドルに成長すると予測されます。

主要ハイライト

- ドイツではeコマースの急増により包装資材の需要が高まっています。これに対応するため、地域の包装企業は軸足を移し、オンライン小売向けに特別に設計された、コスト効率が高く、安全で軽量なソリューションを提供しています。

- これらの製品は、材料の使用量を最適化しながら、輸送中に製品を保護する革新的なデザインを特徴としています。オンライン注文の増加に対応するため、これらの企業は、ロボットシステムやAIを活用した仕分けツールなど、最先端の自動梱包技術への投資を進めています。こうした自動化は、作業を合理化するだけでなく、包装品質の均一性も保証します。

- ドイツの包装食品とパーソナルケア部門は、今後数年間で勢いを増すと思われる傾向として、より小さなパックサイズへの需要の高まりを目の当たりにしています。このシフトは、単身世帯の増加、リシーラブルで持ち運びに便利な包装への嗜好、賞味期限への配慮といった要因によるものです。

- こうした動きは、ソースやドレッシングから菓子類や加工果物に至るまで、包装資材の必要性を増幅させています。これに応えるため、メーカーは製品の鮮度を優先し、無駄を最小限に抑え、ポーションコントロールを強化する革新的な包装ソリューションを考案しています。

- 軟質プラスチック包装のニーズは、その軽量性と適応性によって増加傾向にあります。この動向は、コンパクトで使い勝手の良い包装を好む傾向やデザインの先進性によって後押しされています。軟質プラスチックは賞味期限を延ばし、輸送コストを削減するだけでなく、製品の保護も強化します。環境への配慮から、メーカー各社はリサイクルや生分解が可能な軟質プラスチックの開発を優先しています。

- 環境に優しい包装材料への消費者のシフトは顕著です。アルミニウムとガラスは、環境面での利点とリサイクル可能性が評価され、この地域で人気を集めています。この動向は、従来のプラスチックからの脱却という、より広範な動きを裏付けています。

- さらに、欧州理事会は、使い捨てプラスチックを対象とし、野心的なリサイクル目標を設定する新しいEU全体の規制を展開しました。これらの規制は、市場の情勢に影響を与えることになると考えられます。

ドイツの包装市場の動向

規制強化の中で成長を続けるドイツのプラスチック包装セクター

- ドイツでは、ソリューションサプライヤーとエンドユーザーの先進的な取り組みにより、プラスチック包装ソリューションの導入が進んでいます。「メイド・イン・ドイツ」の評判は、この地域のプラスチック包装企業にとって有益な環境を育んできました。しかし、ドイツ政府はプラスチック包装産業に厳しい規制を課しています。ドイツの包装法は、包装をリサイクルできるように設計し、リサイクル性を重視し、リサイクル可能で再生可能な材料を使用することを義務付けています。

- メーカー各社は、様々なセグメントでの需要増加に伴い、プラスチックボトルの使用拡大を目の当たりにしています。例えば、2023年6月、Coca-Cola Europacific Partners Germanyは、バートノイエナールの施設で未使用のリターナブルPETラインを稼動させました。このラインは、コカ・コーラ、ファンタ、スプライトを含む人気の炭酸飲料をボトリングし、無糖のバリエーションを再導入します。

- 清涼飲料、特に炭酸飲料は、主にプラスチックボトル、特にポリエチレンテレフタレート(PET)ボトルで包装されています。消費量の増加に伴い、こうしたペットボトルの需要も増加し、プラスチック包装部門の成長に拍車をかけています。非アルコール飲料経済協会(wafg)のデータによると、2023年にはドイツ人の平均的なソフトドリンク消費量は約124.5リットルとなり、2020年の114.7リットルから増加します。

- このような消費動向は、リサイクル材料や生分解性プラスチックなど、サステイナブルプラスチック包装ソリューションに軸足を移す可能性があります。企業は、環境責任に対する消費者や規制当局の要求に応えるため、こうしたイノベーションに投資することになると考えられます。

- プラスチックボトルや容器は、その費用対効果、扱いやすさ、割れにくさから、シャンプー、コンディショナー、ローションなどのパーソナルケア製品に好まれています。さらに、リサイクルや生分解性オプションなど、環境に優しいプラスチック材料の進歩により、持続可能性への懸念が緩和され、環境意識の高い消費者にとってより魅力的なものとなっています。例えば、2024年8月、Alpla Werke Alwin Lehner GmbH &Co KGとzerooo initiator SEA ME GmbHは、化粧品とパーソナルケア製品に合わせた、再利用可能で完全にリサイクル可能なPETボトルを発表しました。

ドイツの包装産業は食品動向と環境問題に牽引されている

- 在宅勤務の根強い動向に後押しされた食品セグメントが、主にドイツの包装産業を牽引しています。軽量でコスト効率が高く、デザインに柔軟性のあるプラスチックが食品包装の主流を占めており、製品の保管や使用が容易で理想的です。

- 硬質プラスチック包装は大量生産に有利なコスト優位性を誇るが、紙や段ボール包装の人気も高まっており、その携帯性と利便性が挙げられています。これらの材料は、冷蔵せずに賞味期限を延ばすだけでなく、環境への優しさも裏付けています。

- 経済が繁栄するにつれ、スーパーマーケットからコンビニエンスストアまで、近代的な小売店は、特に冷凍食品の提供において、その視野を広げています。この小売業の進化は、シュリンクフィルム、軟質バッグ、蓋フィルム、ハイバリア材料、熱成形フィルム、スキンフィルムなど、新興市場における多様な包装技術の採用を加速させています。

- 環境に対する懸念の高まりを受けて、ドイツの大手FMCG企業は食品包装におけるプラスチック使用を意欲的に削減し、環境に優しい材料に軸足を移しており、紙ベースの包装が顕著な急増を確認しています。

- 消費者に安全に届けるために、食品包装は極めて重要な役割を果たしています。機能的で見た目にも美しい包装への需要が高まる中、食品包装セグメントの企業はこうした期待に応えるべく準備を整えています。

- トレイからパウチ、箱に至るまで多様な包装ニーズを持つ調理済み食品は、包装市場の技術革新を牽引しています。メーカー各社は、こうした需要に応えるため、多様なソリューションを積極的に開発しています。

- Statistisches Bundesamtのデータによると、ドイツのレディミールの売上高は顕著に増加しており、2021年の439万米ドルから2023年には635万米ドルにまで急増しています。数量の増加を示すこの売上急増は、各惣菜が独自の包装を必要とするため、包装資材の需要増に直結します。

ドイツの包装産業概要

細分化されたドイツの包装市場には、市場で大きな存在感を示す様々な世界企業が含まれます。主要参入企業には、Amcor plc、Berry Global Inc.、Mondi plc、O-I Germany GmbH &Co.KG(Owens-Illinois Inc.の子会社)、Smurfit WestRock plc、Ball Corporationなどが挙げられます。ドイツの包装産業では、戦略的成長を目指した製品発売、買収、企業間とそのユニット間の提携といった動向が一貫して見られます。

- 2024年11月、Mondi plcはドイツに革新的なハブを開設し、軟質包装ソリューションの未来を共同創造することを目指します。これらの体験型スタジオは、モンディの顧客がイノベーションプロセスに直接関与できるように設計されています。この実践的な関与により、顧客はモンディの豊富な専門知識、最先端技術、軟包装セグメントにおけるサステイナブル変革推進へのコミットメントを活用することができます。パイロット・ライン、テスト能力、コラボレーション・スペースを統合することで、Mondiは新しい包装とペーパーソリューションの市場導入を加速する態勢を整えています。

- 2024年10月、Ardagh Group S.A.の一部門であるArdagh Glass Packaging-Europe(AGP-Europe)は、標準的なワインボトルの新しい軽量シリーズを発表しました。ドイツで製造されたこれらのボトルは、特に欧州市場に対応しています。特筆すべきは、ボトルが410gから360gに軽量化されたことです。この軽量化は、再生ガラスカレットを最大80%使用することで可能となり、その結果、ボトル1本あたりの二酸化炭素排出量を12%削減することに成功しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 各国の先進技術導入による革新的でカスタマイズ型包装ソリューションへの需要

- 環境に優しく便利な包装ソリューションへの需要の高まり

- 市場抑制要因

- 政府の規制と環境問題

第6章 市場セグメンテーション

- 材料別

- 紙と板紙

- ガラス

- プラスチック

- 金属

- その他

- 包装タイプ別

- 硬質

- 軟質

- 産業別

- 食品

- 飲料

- 医薬品

- 家庭用品・パーソナルケア

- その他のエンドユーザー産業別

第7章 競合情勢

- 企業プロファイル

- Amcor plc

- Berry Global Inc.

- Mondi plc

- Ball Corporation

- Ardagh Group S.A.

- Crown Holdings, Inc.

- O-I Germany GmbH & Co. KG(Owens-Illinois Inc.)

- Smurfit WestRock plc

- Stora Enso Oyj

- Constantia Flexibles GmbH

第8章 投資分析

第9章 市場機会と今後の動向

The Germany Packaging Industry is expected to grow from USD 38.06 billion in 2025 to USD 46.83 billion by 2030, at a CAGR of 4.23% during the forecast period (2025-2030).

Key Highlights

- In Germany, the surge of e-commerce has led to a heightened demand for packaging materials. In response, regional packaging companies are pivoting, providing cost-effective, secure, and lightweight solutions specifically designed for online retail.

- These offerings feature innovative designs that safeguard products during transit while optimizing material usage. To handle the uptick in online orders, these firms are channeling investments into cutting-edge automated packing technologies, including robotic systems and AI-driven sorting tools. Such automation not only streamlines operations but also guarantees uniformity in packaging quality.

- Germany's packaged food and personal care sectors are witnessing an escalating demand for smaller pack sizes, a trend poised to gain momentum in the coming years. This shift is attributed to factors like the rise of single-person households, a preference for resealable, on-the-go packaging, and best-before-date considerations.

- These dynamics amplify the need for packaging materials in items ranging from sauces and dressings to confectionery and processed fruits. In response, manufacturers are crafting innovative packaging solutions that prioritize product freshness, minimize waste, and enhance portion control.

- The need for flexible plastic packaging is on the rise, driven by its lightweight nature and adaptability. This trend is bolstered by the preference for compact, user-friendly packaging and design advancements. Flexible plastics not only extend shelf life and cut transportation costs but also bolster product protection. In light of environmental concerns, manufacturers are prioritizing the development of recyclable and biodegradable flexible plastic variants.

- There's a noticeable consumer shift towards eco-friendly packaging materials. Aluminum and glass are gaining traction in the region, celebrated for their environmental benefits and recyclability. This trend underscores a broader movement away from traditional plastics.

- Additionally, the European Council has rolled out new EU-wide regulations targeting single-use plastics and setting ambitious recycling goals. These regulations are poised to influence the market landscape.

German Packaging Market Trends

Germany's Plastic Packaging Sector Navigates Growth Amidst Stricter Regulations

- Germany is increasingly adopting plastic packaging solutions, driven by advancements from solution suppliers and end users. The "Made in Germany" reputation has fostered a conducive environment for the region's plastic packaging companies. However, the German government has imposed stringent regulations on the plastic packaging industry. The German Packaging Law mandates that packaging be designed for recycling, emphasizing recyclability and using recyclable and renewable materials.

- Manufacturers are witnessing an expansion in the use of plastic bottles, with rising demand across various sectors. For instance, in June 2023, Coca-Cola Europacific Partners Germany activated an unused returnable PET line at its Bad Neuenahr facility. This line will bottle popular carbonated soft drinks, including Coca-Cola, Fanta, and Sprite, and reintroduce sugar-free variants.

- Soft drinks, especially carbonated ones, are primarily packaged in plastic bottles, especially polyethylene terephthalate (PET) bottles. As consumption rises, so does the demand for these plastic bottles, fueling growth in the plastic packaging sector. Data from the Economic Association of Non-Alcoholic Beverages (wafg) indicates that in 2023, the average German consumed approximately 124.5 litres of soft drinks, up from 114.7 litres in 2020.

- This growing consumption trend may lead to a pivot towards sustainable plastic packaging solutions, such as recycled materials or biodegradable plastics. Companies will likely invest in these innovations to align with consumer and regulatory demands for environmental responsibility.

- Plastic bottles and containers are favoured for personal care products like shampoos, conditioners, and lotions due to their cost-effectiveness, ease of handling, and resistance to breakage. Moreover, advancements in eco-friendly plastic materials, including recycled and biodegradable options, have alleviated sustainability concerns, making them more appealing to environmentally conscious consumers. For instance, in August 2024, Alpla Werke Alwin Lehner GmbH & Co KG and zerooo initiator SEA ME GmbH unveiled a reusable and fully recyclable PET bottle tailored for cosmetics and personal care products.

Germany's Packaging Industry is Driven by Food Trends and Environmental Concerns

- The food sector, bolstered by the persistent work-from-home trend, primarily drives Germany's packaging industry. Lightweight, cost-effective, and design-flexible, plastics dominate food packaging, making them ideal for easy product storage and use.

- While rigid plastic packaging boasts cost advantages for large-scale production, paper and cardboard packaging are rising in popularity, mentioned for their portability and convenience. These materials not only extend shelf life without refrigeration but also back environmental friendliness.

- As economies flourish, modern retail outlets, from supermarkets to convenience stores, are broadening their horizons, especially in frozen food offerings. This retail evolution accelerates the adoption of diverse packaging technologies in emerging markets, including shrink films, flexible bags, lidding films, high-barrier materials, thermoforming films, and skin films.

- In response to growing environmental concerns, major FMCG companies in Germany are ambitiously cutting down on plastic use in food packaging, pivoting towards eco-friendly materials, with paper-based packaging witnessing a notable surge.

- Ensuring safe delivery to consumers, food packaging plays a pivotal role. As demand rises for both functional and visually appealing packaging, companies in the food packaging sector are gearing up to meet these expectations.

- Ready meals, with their diverse packaging needs ranging from trays to pouches and boxes, are driving innovation in the packaging market. Manufacturers are actively developing varied solutions to cater to these demands.

- Data from Statistisches Bundesamt reveals a notable uptick in Germany's ready meals revenue, soaring from USD 4.39 million in 2021 to USD 6.35 million in 2023. This revenue surge, indicative of heightened sales volumes, directly correlates to an increased demand for packaging materials, as each ready meal necessitates its own packaging.

German Packaging Industry Overview

The fragmented German packaging market includes various global players with significant market presence. Key players encompass Amcor plc, Berry Global Inc., Mondi plc, O-I Germany GmbH & Co. KG (a subsidiary of Owens-Illinois Inc.), Smurfit WestRock plc, and Ball Corporation, among others. The German packaging industry has consistently witnessed trends such as product launches, acquisitions, and collaborations among businesses and their units, all aimed at strategic growth.

- November 2024: Mondi plc has inaugurated an innovative hub in Germany, aimed at co-creating the future of flexible packaging solutions. These experiential studios are designed for Mondi's customers to engage directly in the innovation process. This hands-on involvement allows them to leverage the company's vast expertise, cutting-edge technology, and commitment to driving sustainable change in the flexible packaging sector. By consolidating pilot lines, testing capabilities, and collaborative spaces, Mondi is poised to accelerate the market introduction of its new packaging and paper solutions.

- October 2024: Ardagh Glass Packaging-Europe (AGP-Europe), a division of Ardagh Group S.A., has unveiled a new lightweight range of standard wine bottles. Manufactured in Germany, these bottles cater specifically to the European market. Notably, the bottles have undergone a weight reduction from 410g to 360g. This achievement was made possible by incorporating a high recycled glass cullet level of up to 80%, resulting in a commendable 12% decrease in carbon emissions for each bottle produced.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGTHS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Innovative and Customized Packaging Solution Aided with Country-s Adoption of Advanced Technology

- 5.1.2 Increasing Demand for Eco-friendly and Convenient Packaging Solution

- 5.2 Market Restraints

- 5.2.1 Government Regulations and Environmental Concerns

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Paper and Paperboard

- 6.1.2 Glass

- 6.1.3 Plastic

- 6.1.4 Metal

- 6.1.5 Other Materials

- 6.2 By Packaging Type

- 6.2.1 Rigid

- 6.2.2 Flexible

- 6.3 By End-user Vertical

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Pharmaceutical

- 6.3.4 Household and Personal Care

- 6.3.5 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor plc

- 7.1.2 Berry Global Inc.

- 7.1.3 Mondi plc

- 7.1.4 Ball Corporation

- 7.1.5 Ardagh Group S.A.

- 7.1.6 Crown Holdings, Inc.

- 7.1.7 O-I Germany GmbH & Co. KG (Owens-Illinois Inc.)

- 7.1.8 Smurfit WestRock plc

- 7.1.9 Stora Enso Oyj

- 7.1.10 Constantia Flexibles GmbH