|

市場調査レポート

商品コード

1851760

フレキシブルパイプ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Flexible Pipe - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フレキシブルパイプ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月13日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

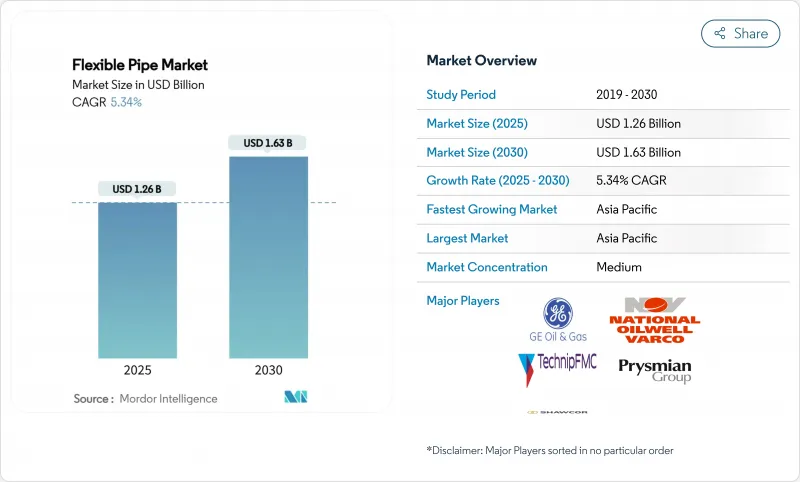

フレキシブルパイプの市場規模は2025年に12億6,000万米ドル、2030年には16億3,000万米ドルに達すると予測され、予測期間中のCAGRは5.34%です。

この成長は、深海・超深海探査プログラム、腐食を緩和する急速な材料革新、ブラジルとガイアナにおけるプレソルト開発の拡大に起因しています。業界大手は、リアルタイムで完全性データを提供する光ファイバーセンサーを埋め込み、ダウンタイムを削減すると同時に資産の寿命を延ばしています。アジア太平洋は、中国、インド、オーストラリアのオフショア・プログラムに後押しされ、物流コストを下げる国内製造に支えられて、突出した地位を占めています。素材面では、高密度ポリエチレン(HDPE)が依然として事業者の既定の選択肢となっているが、軽量化の要請が強まるにつれて、炭素繊維やその他の複合素材によるソリューションが牽引力を増しています。SaipemとSubsea7の合併案のような垂直統合戦略の加速は、エンジニアリング、調達、建設、据付(EPCI)能力を1つの企業傘下にまとめることによって、競争ラインを引き直そうとしています。

世界のフレキシブルパイプ市場の動向と洞察

深海・超深海開発の拡大

複雑な海底地形では硬質鋼管システムが不経済になるため、オペレーターは1,500mを超えるプロジェクトを認可するようになっています。ChevronのAnchorフィールドでは、フレキシブルパイプ市場に新たな性能基準を設定する20ksiの海底ハードウェアが稼働を開始しました。ブラジルのプレソルト層では、水深2,900mでCO2による腐食応力が発生するため、実績のある複合材技術を持つサプライヤーが有利です。TechnipFMCのiEPCIのようなシステムレベルの契約モデルは、スケジュールを最大20%圧縮し、統合されたフレキシブル・ソリューションへの需要を強化しています。

腐食した鋼製ラインの複合材への置き換え

オフショアの年間腐食費用は25億米ドルに達し、カソード保護を回避する複合材による改修の経済性が高まっています。サイペムのプラスチックライニング・パイプライン技術は、1,000バールの定格を維持しながらコストを40%削減します。北海のオペレーターは、1990年以前に遡る10,000kmのレガシーグリッドに直面しています。フレキシブルパイプシステムは、重いリフトスプレッドを使用せずに既存の通路に挿入でき、改修のダウンタイムを削減します。ベーカーヒューズの非金属製品に内蔵されたセンサーは、労働集約的な検査ラウンドを置き換える完全性分析を提供します。

原油価格の変動がCAPEXを抑制

1バレルあたり70~90米ドルの価格変動は、最終的な投資決定を遅らせる。金利の上昇はハードルの閾値を引き上げ、認可をさらに先延ばしにします。成熟した北海とメキシコ湾の油田は特に脆弱で、フレキシブルパイプがプロジェクトの総CAPEXの最大20%を占め、経済性が価格に敏感になっているからです。

セグメント分析

HDPEのフレキシブルパイプ市場規模は2024年に4億5,000万米ドルに達し、35.75%の売上高を占めました。事業者は、コスト効率の高い押出成形、化学的不活性、溶接のない継ぎ手などの点で、HDPEを高く評価しています。それでも、炭素繊維や先端ポリマーを中心とするその他の素材は、CAGRで8.42%のCAGRを記録し、浮体式生産システムが上面への積載を容易にするための大量節約を追い求める中、既存企業を凌駕しています。シドニー大学は、CFRPの廃棄物量が2030年までに50万トンに達すると予測しており、循環型経済への圧力が強まり、研究開発がリサイクル可能な樹脂に方向転換する可能性があります。

疲労寿命と温度窓の強化でフレキシブルパイプのシェア拡大を推進する材料イノベーターたち。先進的なPAとPVDF層は130℃のサービスを提供し、高HTHP油井へのフレキシブルな展開を拡大します。熱可塑性コンポジットパイプ(TCP)は、炭素繊維引張ケーシングとPA12ライナーを結合させ、腐食ゼロと低摩擦フロープロファイルを実現します。深海での活動が拡大するにつれて、複合材料の採用が進み、2030年までにはその他の材料の寄与がフレキシブルパイプ市場の3分の1にまで高まると予想されます。

アンボンドアーキテクチャーは、フープ荷重とアキシャル荷重を切り離す多層装甲を活用し、2024年の世界売上高の45.65%を占めました。補修が可能なため、動的なライザー用途に適しています。しかし、金属カーカスを使用しない強化熱可塑性パイプは、オペレーターが腐食のない性能とデッキ荷重の軽さを目標としているため、CAGR 7.34%で拡大します。FlexSteelのスプール可能なRTPソリューションは、陽極やコーティングキャンペーンを不要にし、ブラウンフィールドのタイインにおけるOPEXを削減します。

フレキシブルパイプ市場における構造の選択は、疲労、圧力、化学物質への暴露プロファイルにかかっています。ボンデッドパイプは、ニッチな超高圧フローラインの役割を果たすが、現場での補修オプションが限られており、コストが高いというハンディキャップがあります。アラミドやガラス繊維の巻線における技術革新は、疲労蓄積を追跡するデジタルツインと相まって、かつては強度の限界によって参入が阻まれていたライザー業務にRTPを浸透させることができるようになると思われます。

地域分析

アジア太平洋は、南シナ海の深海ブロックとオーストラリアのLNG埋め戻しプログラムを背景に、2024年の売上高の38.23%を維持した。同地域のフレキシブルパイプ市場規模はCAGR 8.35%で上昇し、他を圧倒すると予測されます。中国やインドの事業者向けにリール敷設のリードタイムを短縮する東南アジアのTechnipFMCの工場のような、地域製造ハブの建設に拍車をかける。日本と韓国では、洋上風力発電の導入が拡大しており、海底電力ケーブルとダイナミックアンビリカルに対する需要が波及し、複合材料の相互肥沃化がさらに促進されています。

北米は、20ksiのフレキシブル・ジャンパーを必要とするメキシコ湾の超深海制裁に支えられ、第2位の地域となっています。アナダルコ盆地のギャザリングラインとパーミアンの水素実証プロジェクトが、陸上でのスプーラブル採用を後押ししています。しかし、アジア太平洋地域のCAGRは、メキシコ湾のリプレースの波が発見率の停滞によって相殺されているため、遅れています。

欧州は、北海の延命プロジェクトと、ノルウェーと英国における初期の水素バックボーンパイロット事業によって、バランスの取れた成長を示しています。厳しい廃炉法が老朽化した鋼材の撤去を加速させ、タイバック・スキームにおけるフレキシブルなライン代替のためのレトロフィットの機会を提供します。しかし、リサイクルの義務化により、サプライヤーはポリマー回収のためのクローズドループモデルを提案する必要があり、総設備コストが上昇する可能性があります。

中東とアフリカでは、カタールエナジーのノースフィールド・コンプレッション・プログラムと西アフリカのFPSOキャンペーンが、腐食に強い複合材料を求めており、急速な採用が進んでいます。サイペムがカタールで40億米ドルのEPCを受注したことは、ハイスペックなフローラインと光ファイバー入りアンビリカルに対するこの地域の意欲を裏付けるものです。トルコのSakaryaフェーズ2では、2,200m定格のパイプが158km敷設される予定であり、黒海流域の成熟を示すものです。ブラジルのプレソルトとガイアナのスタブロエク・ブロックを中心とする中南米は、世界のSURFバックログの大部分を占め、リオ近郊にスプール基地を併設するというメーカーの決定を後押ししています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 深海・超深海開発の拡大

- 腐食した鋼製ラインの複合材料への置き換え

- ブラジルとガイアナにおけるSURFメガプロジェクトのパイプライン

- カーボンファイバー装甲パイプがFPSOを軽量化

- 組み込み型光ファイバー健康モニタリング

- 水素とCO2のフレキシブル輸送需要

- 市場抑制要因

- 原油価格の変動が設備投資を抑制

- リジッド・スチールに比べ初期費用が高め

- ポリマーパイプの使用済みリサイクルのギャップ

- 20k-psi定格パイプのタイトな能力

- サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 素材タイプ別

- 高密度ポリエチレン(HDPE)

- ポリアミド(PA)

- ポリフッ化ビニリデン(PVDF)

- その他素材タイプ

- パイプ構造タイプ別

- アンボンドフレキシブルパイプ

- 接着フレキシブルパイプ

- 強化熱可塑性プラスチックパイプ(RTP)

- 機能用途別

- フローライン

- ライザー

- ジャンパーとタイアップ

- 輸出/ローディングホース

- 設置環境別

- オフショア

- 浅瀬(500m未満)

- 深海(500-1500 m)

- 超深海(1500m以上)

- オンショア

- オフショア

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア、ニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- TechnipFMC plc

- National Oilwell Varco(NOV)

- Saipem S.p.A.

- Prysmian Group

- Shawcor Ltd

- Strohm(formerly Airborne Oil & Gas)

- Magma Global Ltd

- SoluForce BV

- ContiTech AG

- Chevron Phillips Chemical Co.

- FlexSteel Pipeline Technologies Inc.

- GE Oil & Gas(Baker Hughes)

- Aker Solutions ASA

- Wellstream Processing(NOV)

- Subsea 7 S.A.

- Oceaneering International

- Hunan Great Steel Pipe Co.

- JDR Cable Systems Ltd

- Polyflow LLC

- Cosmoplast Industrial Co.