|

市場調査レポート

商品コード

1630228

エンタープライズAI-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Enterprise AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エンタープライズAI-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

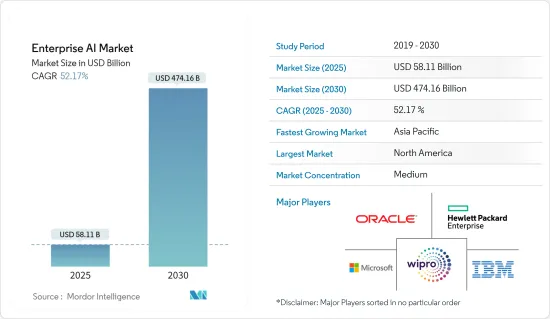

エンタープライズAI市場規模は2025年に581億1,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは52.17%で、2030年には4,741億6,000万米ドルに達すると予測されます。

企業は、人工知能をビジネスプロセスに組み込むことの価値を認識しており、プロセスフローの自動化によって効率を改善し、コストを削減しています。最も重要なことは、企業がビジネス成果を予測し、収益性を高めるのに役立っていることです。

主要ハイライト

- 企業のデジタル化は市場で最も支配的な動向です。第4次産業革命(インダストリー4.0)は、モノのインターネット、人工知能、インテリジェントロボット、ユビキタス・モバイルスーパーコンピューティング、情報管理、分析など、物理的かつ先進的デジタル技術を特徴とし、様々な産業に大きな影響を与えています。

- インダストリー4.0の普及に伴う産業オートメーションのブームは、製造プロセスの効率を高めるためのロボットや自動化技術の導入を促進しています。例えば、バンク・オブ・アメリカによると、ロボット工学とAIの産業用ロボットセグメントは、2025年までに約240億米ドルの価値が見込まれています。この動向は、AIの重要な側面であるロボティックプロセスオートメーション(RPA)を企業間で強化しています。

- さらに、2022年6月には、インダストリー4.0に焦点を当てた製造実行システム(MES)を提供するCritical Manufacturingが、SwissSEMの生産プロセスの最適化に採用されたと発表しました。この決定は、同社の非常に複雑な生産ラインの運用コストの最小化と運用効率の強化に基づき、より大きなデジタルオートメーションに移行するために行われました。クリティカル・マニュファクチャリング社の新しい製造実行システム(MES)は、生産プロセスに関する正確でリアルタイムの情報を容易にし、継続的なプロセス改善、品質向上、コスト削減の基盤を確立します。

- エッジコンピューティング、拡張現実、バーチャルリアリティ、産業用ロボット、自動運転車、デジタル製造、IIOT、デジタルマニュファクチャリングなどの新技術により、さまざまな製造業が目覚ましい発展を遂げています。これらのソリューションは、生産プロセスの個別化、適応性、敏捷性を高め、市場成長をさらに促進する可能性があります。

- 2022年2月、米国鉄鋼とロボット工学・AIスタジオのCarnegie Foundryは、戦略的投資と関係を発表しました。ピッツバーグを拠点とする2つの新興企業は、最先端のロボット工学と人工知能を活用した産業オートメーションの加速と拡大に共同で取り組んでいく。カーネギー鋳造は今回の資金調達により、高度製造、産業用ロボット、統合システム、自律型モビリティ、音声分析などのセグメントにおけるロボット工学とAI技術の産業オートメーション・ポートフォリオを販売し、規模を拡大します。

- US Steelによると、この協働により、同社は産業用ロボットと独立系ソリューションの革新の最前線に立つことになります。鉄鋼メーカーによると、堅牢で弾力性のあるサプライチェーンに対する顧客の期待に応えるためには、先進的技術が必要になるといいます。

- さらに、エンタープライズAIはデジタルトランスフォーメーションの重要な実現手段です。今後数年のうちに、ほぼすべての企業向けソフトウェア・アプリケーションがAIに対応するようになると考えられます。そのため、エンタープライズAIアプリケーションを大規模に構築、展開、運用する能力を開発することは、ビジネス存続のために必須となりつつあります。

- O'ReillyのエンタープライズAI導入に関する2022年レポート(エンタープライズAI導入に関するアンケートに対するニュースレター受信者の回答による)によると、AIを使用していないと回答した企業は31%(最近の13%から増加)、導入を評価中が43%、AIアプリケーションを導入済みは26%でした。AIを導入している製造業の回答者が18%から31%に急増したのはオセアニア地域でした。相当数の組織がAIガバナンスを欠いています。AI製品を生産している回答者の26%のうち、プロジェクトがどのように作成され、測定され、観察されるかを監督するガバナンス・プランを持っているのは49%だけである(持っていない回答者は51%)。

- 近年、インダストリー4.0に関連するソリューションに焦点を当てた様々なパートナーシップが、研究市場の成長をさらに加速させています。例えば、2022年1月、Telefonicaのデジタルサービス部門であるTelefonica Techは、スペインのエンジニアリングサービス会社であるGrupo Alavaと契約を結び、スペインの通信事業者のプライベート5G、ビッグデータ「AI」分析、クラウドとエッジコンピューティングも活用したインダストリー4.0市場向け予測分析ソリューションを導入しました。

エンタープライズAIソフトウェア市場動向

クラウド導入が市場を大きく成長させる見込み

- 以前は概念であったAIクラウドは、現在ではAIとクラウドコンピューティングを組み合わせて、企業によって導入され始めています。クラウドコンピューティングに新たな価値向上をもたらすAIツールやソフトウェアなどが、その大きな促進要因となっています。クラウドは経済的なデータストレージと計算オプションであり、AIの導入に一役買っています。

- Flexera Softwareによると、企業の回答者の75%が、2023年にパブリッククラウドの利用にMicrosoft Azureを採用すると回答しています。AWS、Microsoft Azure、Google Cloud、またはハイパースケーラは、世界で最も高いクラウドコンピューティングプラットフォーム・プロバイダーの1つです。

- AIクラウドは主にAIの使用事例のための共有インフラで構成され、クラウドインフラ上で複数のプロジェクトとAIワークロードを常時同時にサポートします。AIクラウドは、AIハードウェアとソフトウェアを組み合わせ、ハイブリッド・クラウドインフラ上でAI Software-as-a-Serviceを提供することで、組織にAIへのアクセスを提供し、AI能力をより活用できるようにします。

- クラウドにおけるAIの最も魅力的な利点の1つは、それが解決する課題です。AIを大幅に民主化し、よりアクセスしやすくします。導入コストを下げ、共創とイノベーションを促進することで、AIを活用した企業変革が推進されます。

- 世界中の組織でクラウドソリューションの導入が進んでいます。例えば、2022年7月、B2Bの仮想ネットワーク事業者(VNO)であるCloud Connect Communicationsは、電気通信省(DoT)からムンバイとアーメダバードでの事業免許を取得しました。Cloud Connectは、クラウドベースの統合コミュニケーションソリューション、CRM(顧客関係管理)とプログラマブルAPIを通じたテレフォニーとの統合、国内外市場でのフォーラムへの通話と管理アクセスを備えた企業向け通話管理システムを記載しています。

- さらに2022年1月、OracleはOracle Cloud for Telcosを発表しました。Oracle Cloud for Telcosは、Oracle Cloud Infrastructure上に構築された完全なクラウドソリューション・スイートです。OCIは分散型クラウドアーキテクチャーで利用できるクラウドプラットフォームで、世界に36のパブリック・クラウド地域を持っています。さらに、60を超える産業アプリケーション・スイートを備えたOCIプラットフォームは、サードパーティ、カスタム、Oracle Fusion Cloud Applications Suiteのワークロードを可能にします。

大幅な市場成長を遂げる欧州

- 欧州では、産業革命や自動化などの主流動向により、需要が増加しています。同地域の企業は、機械学習の開発に伴い、ロボット工学、人工知能など、さまざまな自動化技術に投資していることが確認されています。

- 多くの政府資金援助も、この地域の製造業における最新技術の採用を支援しています。例えば、2022年10月、英国研究開発(UKRI)は、製造業のエネルギー効率、生産性、成長を向上させる技術を開発するため、12のスマート工場プロジェクトに1,370万英ポンドの資金を授与しました。予算獲得企業には、AIを利用して鉄鋼生産の非効率を発見する企業や、3Dプリンティングでリサイクル材料を利用する企業などが含まれます。これは、英国の製造業における技術利用の拡大を目指す、政府によるより広範な1億4,700万英ポンドのMade Smarter Innovation Challengeの一環です。

- さらに、地域の主要企業がエンタープライズAI市場に投資し、その能力を拡大しています。例えば、オラクルは2022年9月、エンタープライズ・クラウドサービスへの需要が急速に高まっているスペインに対応するため、スペイン初のオラクル・クラウドインフラ(OCI)地域の設立を発表しました。マドリードに新地域が開設されたことで、スペインにおけるオラクルの公共部門と民間部門の顧客とパートナーは、アプリケーションの更新、データと分析の実験、データセンターからOCIへのミッションクリティカルなワークロードの移行に役立つさまざまなクラウドサービスを利用できるようになります。

- 例えば、Hewlett Packard Enterpriseは2022年5月、欧州のスーパーコンピューター・サプライチェーンを強化するため、チェコ共和国に新拠点を開設すると発表しました。この新工場では、科学研究の推進、AL/ML構想の成熟、イノベーションの加速を目的とした同社のカスタム設計ソリューションが製造される予定です。

- さらに、2022年5月には、欧州の暖炉サプライヤー上位3社の1社であるJotulと、ビジネスクラウドプロバイダーのInforが提携を結びました。Jotulは、産業最大級の販売組織と代理店の世界ネットワークを通じて市場に製品を供給しています。Jotulは、現在のERPソリューションから、標準化された産業用製造ソリューションであるInfor M3 CloudSuiteとInfor Consulting Servicesにアップグレードします。

- このようなコグニティブ・コンピューティングの台頭は、人間の感覚的知覚、推論、思考、学習、意思決定能力を地域企業全体で再現することを可能にすると期待されています。膨大なコンピューティングパワーを活用する能力により、このパラダイムは、スピードと能力の両面で人間による複製を超え、パターンを識別し、個人が知覚する能力を備えていない可能性のある解決策を提供し、AIソリューションの利用を拡大する態勢が整っています。

- さらに、製造部門における自動化の普及率の上昇、製造コストの削減ニーズの高まり、マシン・ツー・マシン(M2M)技術の浸透が、この地域における自動化の導入を後押ししており、産業用制御システムの需要を促進すると予想されます。さらに、ドイツは世界第5位のデジタル経済大国であり、工業生産のデジタル化のためのインダストリー4.0が広く導入されている(GTAIによる)。また、Bitkomデジタルアソシエーションの調査によると、ドイツでは62%の企業がインダストリー4.0関連の技術やソリューション(ソフトウェア、ITサービス、ハードウェア)を利用しています。

エンタープライズAIソフトウェア産業概要

エンタープライズAI市場の競争企業間の敵対関係は、多くの重要な参入企業がいるため高いです。IBM、SAP SE、Hewlett Packard Enterprise、Google Inc.、Microsoft Corporation、Oracle Corporation、その他多くの企業が、ユーザー向けに新しく革新的な製品を設計することで、最大の市場シェアを獲得しようとしています。研究開発、M&A、戦略的拡大、資金調達、戦略的パートナーシップなどへの多額の投資により、競争上の優位性を獲得しています。

2024年8月ベンガルールを拠点とし、昨年設立されたばかりの新興企業Sarvam AIは、生成AIモデルを搭載した一連のB2B製品を発表しました。金融サービス、法律サービス、消費財、技術、メディア、通信などのセグメントを対象に、サルバムは火曜日に多様な製品ラインアップを発表しました。このラインナップには、Sarvam Agents、Sarvam 2B、Shuka 1.0、A1、様々な言語向けに調整された複数のSarvamモデルがあります。

Fujitsuは2024年7月、セキュリティとデータプライバシーに特化したエンタープライズAI企業であるCohere Inc.と戦略的パートナーシップを締結しました。このパートナーシップは、企業に先進的日本語能力を装備する大規模言語モデル(LLM)を開発・提供することで、顧客と従業員の体験を向上させることを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因の採用

- 市場促進要因

- 自動化とAIベースのソリューションに対する需要の高まり

- 指数関数的に増加するデータセットの分析ニーズの高まり

- 市場抑制要因

- 採用率の低迷

- 産業の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- 主要コンポーネント分析

- AIが半導体に与える影響

- COVID-19の市場への影響評価

第5章 市場セグメンテーション

- タイプ別

- ソリューション

- サービス別

- 展開別

- オンプレミス

- クラウド

- エンドユーザー産業別

- 製造業

- 自動車

- BFSI

- IT・通信

- メディア・広告

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- IBM Corporation

- Oracle Corporation

- Wipro Limited

- Hewlett Packard Enterprise

- Microsoft Corporation

- Amazon Web Services

- Google Inc.

- Intel Corporation

- SAP SE

- Sentient Technologies

- AiCure LLC

- NEC Corporation

- NVIDIA Corporation

第7章 投資分析

第8章 市場の将来

The Enterprise AI Market size is estimated at USD 58.11 billion in 2025, and is expected to reach USD 474.16 billion by 2030, at a CAGR of 52.17% during the forecast period (2025-2030).

Enterprises recognize the value of incorporating artificial intelligence into their business processes, improving efficiency and reducing costs by automating process flows. Most importantly, it has helped enterprises predict business outcomes, driving profitability.

Key Highlights

- The digitalization of enterprises is the most dominant trend in the market. The fourth industrial revolution (Industry 4.0) is characterized by physical and advanced digital technologies, such as the Internet of Things, artificial intelligence, intelligent robots, ubiquitous mobile supercomputing, information management, and analytics, which significantly impact various industries.

- The boom of industrial automation, with the widespread adoption of Industry 4.0, is driving the adoption of robots and automated technologies to enhance the efficiency of manufacturing processes. For instance, according to Bank of America, the industrial robot segment of robotics and AI is expected to be valued at about USD 24 billion by 2025. This trend has augmented robotic process automation (RPA) among enterprises, a significant aspect of AI.

- Additionally, in June 2022, Critical Manufacturing, a provider of an Industry 4.0-focused Manufacturing Execution System (MES), announced that it was selected by SwissSEM to optimize its production processes. This decision is made to move towards greater digital automation based on minimizing operating costs and enhancing operating efficiency for its highly complex production line. The new Manufacturing Execution System (MES) from Critical Manufacturing will facilitate accurate, real-time information about production processes, establishing a basis for continuous process improvement, enhanced quality, and reduced costs.

- Various manufacturing industries have experienced tremendous development due to new technologies, including edge computing, augmented and virtual reality, industrial robots, self-driving cars, digital manufacturing, IIOT, and digital manufacturing. These solutions enhance production processes' personalization, adaptability, and agility, which may further drive market growth.

- In February 2022, United States Steel and Carnegie Foundry, a robotics and AI studio, announced a strategic investment and relationship. The two Pittsburgh-based startups will work together to accelerate and expand industrial automation using cutting-edge robotics and artificial intelligence. Carnegie Foundry will use this funding to market and scale its industrial automation portfolio of robotics and AI technologies in advanced manufacturing, industrial robots, integrated systems, autonomous mobility, speech analytics, and other areas.

- According to US Steel, the collaboration keeps the company at the forefront of growing innovation in robotics and independent solutions for the industry. According to the steelmaker, highly advanced technology will be required to meet its client's expectations for a robust and resilient supply chain.

- Furthermore, Enterprise AI is a significant enabler of digital transformation. Nearly every enterprise software application will be AI-enabled in the years to come. Developing competencies in the capability to build, deploy, and operate enterprise AI applications at scale, therefore, is becoming imperative for business survival.

- According to O'Reilly's 2022 report on enterprise AI adoption (based on the answers given by recipients of its newsletters to a questionnaire on enterprise AI adoption), 31% of companies report not using AI (up from 13% recently), 43% are evaluating adoption, and 26% have implemented AI applications. The immediate increase, from 18% to 31%, in manufacturing respondents with AI was in Oceania. A considerable number of organizations lack AI governance. Of the 26% of respondents with AI products in production, only 49% have a governance plan to oversee how projects are created, measured, and observed (versus 51% for those without).

- In recent years, various partnerships focused on solutions related to Industry 4.0 have further accelerated the studied market's growth. For instance, in January 2022, Telefonica Tech, the digital services arm of Telefonica, signed a deal with Spanish engineering services company Grupo Alava to introduce a predictive analytics solution for the Industry 4.0 market that also leverages private 5G, big-data 'AI' analytics, and cloud and edge computing from the Spanish operator.

Enterprise AI Software Market Trends

Cloud Deployment is Expected to Experience a Significant Market Growth

- The AI cloud, which was previously a concept, has now started to be implemented by enterprises, combining AI with cloud computing. Some significant factors driving it include AI tools and software that deliver new, increased value to cloud computing. It is an economical data storage and computation option and plays a role in AI adoption.

- According to Flexera Software, 75% of enterprise respondents indicated adopting Microsoft Azure for public cloud usage in 2023. AWS, Microsoft Azure, and Google Cloud, or hyper scalers, are among the highest cloud computing platform providers worldwide.

- An AI cloud primarily consists of a shared infrastructure for AI use cases, supporting multiple projects and AI workloads simultaneously on cloud infrastructure at any given time. The AI cloud combines AI hardware and software to deliver AI software-as-a-service on hybrid cloud infrastructure, providing organizations with access to AI and enabling them to harness AI capabilities more.

- One of the most compelling advantages of AI in the cloud is the challenges it addresses. It significantly democratizes AI, making it more accessible. Lowering the adoption costs and facilitating co-creation and innovation drive AI-powered transformation for enterprises.

- Organizations across the world are increasingly adopting cloud solutions. For instance, in July 2022, Cloud Connect Communications, a B2B virtual network operator (VNO), was licensed by the Department of Telecommunications (DoT) to operate in Mumbai and Ahmedabad. CloudConnect would deliver corporate call management systems with Integrated Cloud-based Communication Solutions, CRM (customer relationship management) Integration with telephony through programmable APIs, and calls and administrative access to the forum in local and foreign markets.

- Further, in January 2022, Oracle introduced Oracle Cloud for Telcos. Oracle Cloud for Telcos is a complete suite of cloud solutions built on Oracle Cloud Infrastructure. OCI is a cloud platform that can be utilized in dispersed cloud architecture and has 36 public cloud regions globally. Moreover, with over 60 industry application suites, the OCI platform enables third-party, custom, and Oracle Fusion Cloud Applications Suite workloads.

Europe to Experience Significant Market Growth

- The European region is witnessing increased demand due to mainstream trends, such as the industrial revolution and automation. The regional firms have been identified to invest in various automation technologies, such as robotics, artificial intelligence, etc., with developments in machine learning.

- Many government fundings also aid the adoption of the latest technologies in the manufacturing industry in the region. For Instance, in October 2022, UK Research and Innovation (UKRI) awarded 12 smart factory projects a share of GBP 13.7 million in funding to develop technologies that improve energy efficiency, productivity, and growth in manufacturing. The budget recipients include companies using AI to spot inefficiencies in steel production and using recycled materials in 3D printing. It is a part of the government's broader GBP 147 million Made Smarter Innovation Challenge that seeks to increase the use of technology within UK manufacturing.

- Moreover, major regional players are investing and expanding their capabilities in the Enterprise AI market. For Instance, in September 2022, to address the country's quickly growing demand for enterprise cloud services, Oracle announced the creation of the first Oracle Cloud Infrastructure (OCI) region in Spain. With the opening of the new territory in Madrid, Oracle's public and private sector clients and partners in Spain will have access to various cloud services that will help them update their applications, experiment with data and analytics, and move mission-critical workloads from their data centers to OCI.

- For Instance, in May 2022, Hewlett Packard Enterprise announced the launch of its new site in the Czech Republic to strengthen Europe's Supercomputer Supply Chain. The new factory will likely manufacture the company's custom-designed solutions to advance scientific research, mature AL/ML initiatives, and accelerate innovation.

- Moreover, in May 2022, one of the top three suppliers of fireplaces in Europe, Jotul, and Infor, the business cloud provider, established a partnership. Jotul supplies the markets through one of the largest industry-wide global networks of its sales organizations and distributors. Jotul will upgrade to Infor M3 CloudSuite, a standardized industrial manufacturing solution, and Infor Consulting Services from its present ERP solution.

- This rise in cognitive computing is expected to enable the replication of human sensory perception, deduction, thinking, learning, and decision-making capabilities across regional enterprises. The ability to harness considerable amounts of computing power is poised to take this paradigm beyond human replication, both in terms of speed and capacity, to distinguish patterns and provide potential solutions that individuals may not be equipped to perceive, thus augmenting the use of AI solutions.

- Furthermore, a rise in the penetration of automation in the manufacturing sector, the rising need to mitigate manufacturing costs, and the penetration of machine-to-machine (M2M) technologies are encouraging the adoption of automation in the region, which is anticipated to propel the demand for industrial control systems. In addition, Germany is the fifth largest digital economy in the world, and Industry 4.0 for the digitalization of industrial production is being widely implemented in the country (as per GTAI). Also, 62% of companies utilize Industrie 4.0-related technologies and solutions (software, IT services, and hardware) in Germany, according to a Bitkom digital association study.

Enterprise AI Software Industry Overview

The competitive rivalry in the Enterprise AI Market is high due to many significant players. Players like IBM, SAP SE, Hewlett Packard Enterprise, Google Inc., Microsoft Corporation, Oracle Corporation, and many more are trying to achieve maximum market share by designing new and innovative products for users. Their significant investments in research and Development, mergers & acquisitions, strategic expansion, funding, strategic partnership, etc., have allowed them to gain a competitive advantage.

August 2024: Sarvam AI, a startup based in Bengaluru and established just last year, unveiled a range of B2B products powered by its generative AI models. Targeting sectors such as financial services, legal services, consumer goods, technology, media, and telecom, Sarvam introduced a diverse product lineup on Tuesday. This lineup features Sarvam Agents, Sarvam 2B, Shuka 1.0, A1, and multiple Sarvam models tailored for various Indic languages.

In July 2024, Fujitsu entered into a strategic partnership with Cohere Inc., an enterprise AI company specializing in security and data privacy, with offices in Toronto and San Francisco. This partnership aims to develop and provide a large language model (LLM) that equips enterprises with advanced Japanese language capabilities, thereby enhancing customer and employee experiences.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increasing Demand for Automation and AI-based Solutions

- 4.3.2 Increasing Need to Analyze Exponentially Growing Data Sets

- 4.4 Market Restraints

- 4.4.1 Sluggish Adoption Rates

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technology Snapshot

- 4.6.1 Major Component Analysis

- 4.6.2 Impact of AI on the Semicondu

- 4.7 Assessment of the impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Solution

- 5.1.2 Service

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By End-user Industry

- 5.3.1 Manufacturing

- 5.3.2 Automotive

- 5.3.3 BFSI

- 5.3.4 IT and Telecommunication

- 5.3.5 Media and Advertising

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia

- 5.4.4 Australia and New Zealand

- 5.4.5 Latin America

- 5.4.6 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corporation

- 6.1.2 Oracle Corporation

- 6.1.3 Wipro Limited

- 6.1.4 Hewlett Packard Enterprise

- 6.1.5 Microsoft Corporation

- 6.1.6 Amazon Web Services

- 6.1.7 Google Inc.

- 6.1.8 Intel Corporation

- 6.1.9 SAP SE

- 6.1.10 Sentient Technologies

- 6.1.11 AiCure LLC

- 6.1.12 NEC Corporation

- 6.1.13 NVIDIA Corporation