|

市場調査レポート

商品コード

1630184

耐薬品性コーティング:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Chemical Resistant Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 耐薬品性コーティング:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

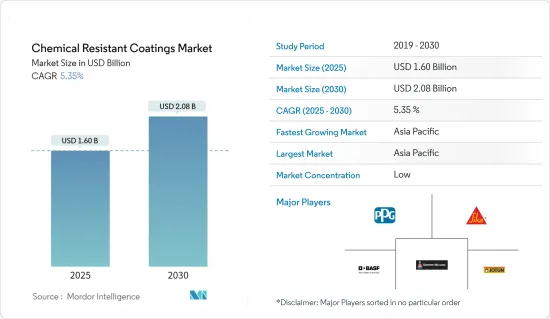

耐薬品性コーティング市場規模は2025年に16億米ドルと推定され、予測期間(2025~2030年)のCAGRは5.35%で、2030年には20億8,000万米ドルに達すると予測されます。

COVID-19により、耐薬品性コーティング市場はマイナスの影響を受けています。2020年上半期にはロックダウンが課せられ、旅行制限もあったため、上半期の大半は産業が停止しました。石油・ガス需要は、世界各国の政府による規制のために大幅に減少しました。しかし、下半期には、ほとんどの産業が最小限の生産能力で稼働しており、渡航制限の解除と操業停止の緩和は、調査対象市場にとって明るい兆しです。

主要ハイライト

- 短期的には、アジア太平洋におけるインフラ整備と工業化活動の拡大、アジア太平洋と北米地域における石油・ガス活動の拡大が市場成長の主要要因です。

- その反面、複雑な製造プロセスと高い投資コストが市場成長の妨げになると予想されます。

- リグニン系ポリウレタンの開発は、市場に成長の機会を与えると予想されます。

- 予測期間中、アジア太平洋が最も大きな市場シェアを占めると予想されます。

耐薬品性コーティングの市場動向

石油・ガスセグメントが市場を独占する

- 石油・ガスセグメントは、耐薬品性コーティング市場の主要なエンドユーザーの一つです。このセグメントでは、事業運営に高温環境が伴うため、本質的に耐薬品性が必要とされます。さらに、高温以外にも、コーティングは金属や鉄骨構造物が湿気や湿気の多い気候条件にさらされるため、腐食や化学品から防ぐために使用されます。

- 石油・ガスの海洋生産は、最も過酷な条件のひとつです。そのため、そこで使用されるコーティングシステムも、同様の条件を満たす必要があります。

- オフショアでは、浸透する紫外線に長時間さらされ、荒い海水と常に接触するため、耐薬品性コーティングの必要性が高まっている

- 米国は、過去6年連続で世界有数の原油生産国としての地位を維持しています。2023年には1,290万バレル/日(b/d)という記録的な平均原油生産量を達成し、2019年に樹立したこれまでの記録を上回った。2023年12月、米国の月平均原油生産量は1,330万バレル/日(b/d)を突破し、月間過去最高を記録しました。

- テキサス州西部とニューメキシコ州東部にまたがるパーミアン・ベースンは、近年の米国全体の原油・天然ガス総生産量の急増を牽引する極めて重要な役割を果たしています。米国は現在、日量約1,350万バレルというかつてない量の原油を生産しています。また、テキサス州やニューメキシコ州のパーミアン・ベースンからの生産量を増やすため、大手エネルギー企業の事業統合が進んでいます。ExxonMobilはシェール大手のPioneer Natural Resourcesを約600億米ドルで買収する意向で、ChevronはHessを530億米ドルで買収する計画です。

- インドゥアでは2024年1月、Oil and Natural Gas Corporation(ONGC)がベンガル湾沖のクリシュナ・ゴダヴァリ盆地にある深海鉱区から石油生産を開始しました。同鉱区の残りの油田・ガス田は2024年半ばまでに操業を開始し、ピーク時の生産量は石油が日量4万5,000バレル、ガスが日量1,000万立方メートルを超えると予想されています。

- 世界の確認石油埋蔵量の約17%を有するサウジアラビアは、世界第2位の確認石油埋蔵量を誇り、最も重要な石油純輸出国にランクされています。石油輸出で得た収益は、インフラの近代化、雇用の創出、社会指標の改善に使われてきました。主要総合エネルギー・化学企業であるサウジアラムコは、上流、中流、下流の各セグメントで幅広く事業を展開しています。

- 2023年3月、Aramcoは2023年度の資本支出目標を450億~550億米ドルと発表しました。この計画は、2027年までに石油生産を日量1,300万バレルまで増加させることを目的としていました。しかし、2024年1月のサウジエネルギー省の命令による混乱により、Aramcoは原油生産能力を日産1,200万バレルから1,300万バレルに引き上げる計画を中止しました。

- したがって、石油・ガスセクターの成長は、予測期間中、調査対象市場の需要を押し上げると予想されます。

アジア太平洋市場を独占する中国

- アジア太平洋では、中国がGDPで最大の経済大国です。中国は、住宅やインフラプロジェクトへの多額の投資により、アジア太平洋の建設状況を支配しています。

- 中国国家統計局のデータによると、2023年の建設セクターのGDPへの寄与率は約6.8%でした。

- 住宅・都市農村開発省が2024年1月に発表したところによると、2023年、中国は都市部の老朽化した5万3,700の住宅コミュニティの改修プロジェクトを実施し、897万世帯に恩恵をもたらしました。これらの改修プロジェクトは、1年間で2,400億人民元(約337億8,000万米ドル)近くの多額の投資を集めました。

- 近年では、大手建設業者(欧州連合)の中国進出が、この産業の成長をさらに後押ししています。さらに、中国は2030年までに約13兆米ドルを建築に費やすと予想されています。

- 国家エネルギー局によると、2023年の中国の原油・天然ガス合計生産量は石油換算で3億9,000万トンを超え、過去最高を更新すると予測されました。原油生産量は2億800万トンを超え、2022年比で300万トン以上の伸びを示しました。さらに、中国の天然ガス生産量は過去7年間、毎年100億立方メートルずつ着実に増加し、前年には2,300億立方メートルに達しました。

- 中国の国営石油会社(NOC)は、2021~2025年までの5年間に、掘削と坑井サービスに1,200億米ドル以上を投じると予想されています。中国の石油・ガス需要の増大により、同国では今後数年間、高水準の掘削活動が確認されると予想されます。

- 上記の要因から、アジア太平洋における耐薬品性コーティングの需要は予測期間中に大幅に増加すると予想されます。

耐薬品性コーティング産業概要

耐薬品性コーティング市場はセグメント化されており、大手多国籍企業が存在します。主要参入企業には、PPG Industries Inc.、Sika AG、The Sherwin-Williams Company、BASF SE、Jotunなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア太平洋と北米における石油・ガス活動の拡大

- アジア太平洋におけるインフラ整備と工業化の進展

- 抑制要因

- 複雑な生産プロセスと高い投資コスト

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 樹脂

- エポキシ樹脂

- ポリエステル

- フッ素樹脂

- ポリウレタン

- その他

- 技術

- 100%固体

- 溶剤系

- 粉末

- 水性

- エンドユーザー産業

- 化学

- 石油・ガス

- 海洋

- 建設インフラ

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- Akzonobel NV

- Daikin Industries Ltd

- Hempel AS

- Jotun

- Kansai Paint Co. Ltd

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

- VersaFlex Incorporated

第7章 市場機会と今後の動向

- リグニン系ポリウレタンの開発

- その他の機会

The Chemical Resistant Coatings Market size is estimated at USD 1.60 billion in 2025, and is expected to reach USD 2.08 billion by 2030, at a CAGR of 5.35% during the forecast period (2025-2030).

Due to COVID-19, the chemical resistant coatings market has been negatively impacted. Due to the imposed lockdowns in the first half of 2020, and travel restrictions, the industries were shut for the most part of the first half of the year. The Oil and gas demand has fallen drastically due to the restrictions imposed by the governments across the globe. However, in the second half of the year most of the industries were working at a minimum capacity, and the lifting of travel restrictions and relaxation of the lockdowns are a positive sign for the market studied.

Key Highlights

- Over the Short term, the major factor driving the growth of the market studied include growing infrastructure and industrialization activities in Asia-Pacific region and expansion in oil and gas activities in Asia-pacific and North America region.

- On the flipside, complex production process and high investment cost are expected to hinder the growth of the market studied.

- The development of lignin-based polyurethanes is expected to give the market a chance to grow.

- Asia-Pacific is expected to hold the most considerable market share over the forecast period.

Chemical Resistant Coatings Market Trends

Oil and Gas Segment to Dominate the Market

- Oil and gas sector is one of the major end-users for the chemical resistant coatings market. The sector essentially requires chemical resistance, owing to a high temperature environment in its business operations. In addition, apart from high-temperature, the coating is used to prevent metal and steel structures from corrosion and chemicals, as they are exposed to moist and damp climatic conditions.

- Offshore oil and gas production has some of the most demanding conditions. Therefore, coating systems used in it are to be equipped likewise.

- Offshore, prolonged exposure to penetrating UV rays and constant contact with rough seawater increases the need for chemical-resistant coatings.

- The United States has maintained its position as the leading crude oil producer globally for the past six consecutive years. In 2023, the country achieved a record-breaking average crude oil production of 12.9 million barrels per day (b/d), surpassing the previous record set in 2019. In December 2023, the average monthly crude oil production in the United States reached a monthly record high, surpassing 13.3 million barrels per day (b/d).

- The Permian Basin, spanning western Texas and eastern New Mexico, has played a pivotal role in driving the surge in total crude oil and natural gas production across the United States in recent years. The United States is currently producing an unprecedented volume of oil, reaching approximately 13.5 million barrels per day. In addition, major energy corporations are consolidating their operations to boost production from the Permian Basin in Texas and New Mexico. ExxonMobil intends to acquire the shale giant Pioneer Natural Resources for nearly USD 60 billion, while Chevron is planning to purchase Hess for USD 53 billion.

- in Indua, in January 2024, the state-run Oil and Natural Gas Corporation (ONGC) initiated oil production from its deep-water block in the Krishna-Godavari basin off the coast of the Bay of Bengal. The block's remaining oil and gas fields are anticipated to commence operations by mid-2024, with peak production estimated at 45,000 barrels of oil per day and over 10 million metric standard cubic meters per day of gas.

- With approximately 17% of the world's proven petroleum reserves, Saudi Arabia ranks among the most significant net petroleum exporters, boasting the second-largest proven oil reserves globally. Proceeds generated from oil exports have been used to modernize infrastructure, create employment, and improve social indicators. Saudi Aramco, a leading integrated energy and chemicals company, operates extensively across upstream, midstream, and downstream segments.

- In March 2023, Aramco unveiled a capital expenditure goal of USD 45-USD 55 billion for FY 2023, representing its most significant capital spending plan. This initiative aimed to support an increase in oil production to 13 million barrels per day by 2027. However, the disruption caused by the Saudi Ministry of Energy's order in January 2024 prompted Aramco to halt its plans to elevate crude production capacity from 12 million to 13 million barrels daily

- Therefore, the growing oil and gas sector is expected to boost the demand for the market studied, during the forecast period.

China to Dominate the Asia-Pacific Market

- In Asia-Pacific, China is the largest economy, in terms of GDP. China is the dominant force in the Asia-Pacific construction landscape, fueled by substantial investments in residential and infrastructure projects.

- Data from China's National Bureau of Statistics highlights that in 2023, the construction sector contributed approximately 6.8% to the nation's GDP.

- In 2023, China undertook renovation projects for 53,700 aging residential communities in urban areas, benefiting 8.97 million households, as the Ministry of Housing and Urban-Rural Development reported in January 2024. These renovation endeavors attracted hefty investments of nearly CNY 240 billion (around USD 33.78 billion) for the year.

- In the recent years, the entry of major construction players (from the European Union) in China has further fueled the growth of this industry. Moreover, China is expected to spend nearly USD 13 trillion on building by 2030.

- According to the National Energy Administration, China's combined crude oil and natural gas production in 2023 was forecasted to exceed 390 million tons of oil equivalent, reaching a new historical high. Crude oil output exceeded 208 million tons, indicating a growth of over 3 million tons compared to 2022. Additionally, China's natural gas production steadily increased by 10 billion cubic meters annually for the past seven years, reaching 230 billion cubic meters in the preceding year.

- China's national oil companies (NOCs) are expected to splurge more than USD 120 billion on drilling and well services in the five years between 2021 and 2025. Due to China's growing demand for oil and gas, the country is expected to witness a high level of drilling activity in years to come.

- Owing to above-mentioned factors, the demand for chemical resistant coatings in Asia-Pacific is expected to increase significantly over the forecast period.

Chemical Resistant Coatings Industry Overview

The chemical resistant coatings market is fragmented, with the presence of majorly multi-national players. Some of the major players include PPG Industries Inc., Sika AG, The Sherwin-Williams Company, BASF SE, and Jotun, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Expansion of Oil and Gas Activities in APAC and North America

- 4.1.2 Growing Infrastructure and Industrialization in the Asia-Pacific Region

- 4.2 Restraints

- 4.2.1 Complex Production Process and High Investment Cost

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin

- 5.1.1 Epoxy

- 5.1.2 Polyester

- 5.1.3 Fluoropolymers

- 5.1.4 Polyurethane

- 5.1.5 Other Resins

- 5.2 Technology

- 5.2.1 100% Solids

- 5.2.2 Solvent Borne

- 5.2.3 Powder

- 5.2.4 Water-borne

- 5.3 End-user Industry

- 5.3.1 Chemical

- 5.3.2 Oil and Gas

- 5.3.3 Marine

- 5.3.4 Construction and Infrastructural

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Qatar

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Akzonobel NV

- 6.4.3 Daikin Industries Ltd

- 6.4.4 Hempel AS

- 6.4.5 Jotun

- 6.4.6 Kansai Paint Co. Ltd

- 6.4.7 PPG Industries Inc.

- 6.4.8 RPM International Inc.

- 6.4.9 Sika AG

- 6.4.10 The Sherwin-Williams Company

- 6.4.11 VersaFlex Incorporated

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Lignin-based Polyurethanes

- 7.2 Other Opportunities