|

市場調査レポート

商品コード

1851571

ヘルスケア包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Healthcare Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヘルスケア包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月07日

発行: Mordor Intelligence

ページ情報: 英文 102 Pages

納期: 2~3営業日

|

概要

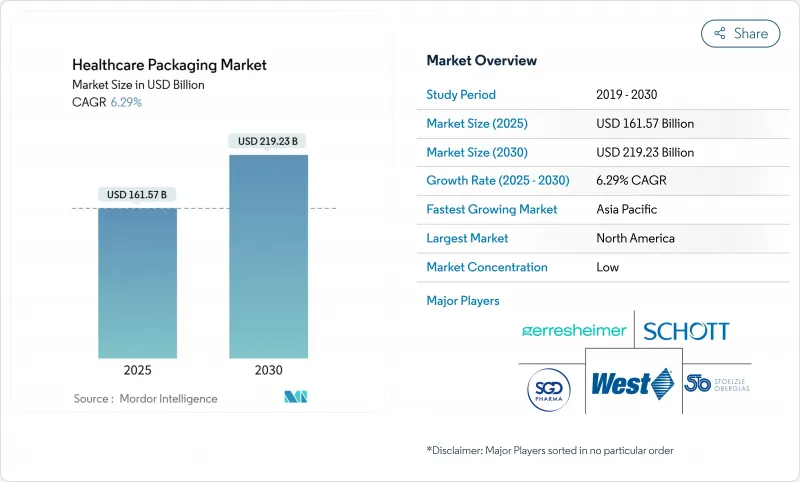

ヘルスケア包装市場規模は2025年に1,615億7,000万米ドルに達し、2030年にはCAGR 6.29%を記録して2,192億3,000万米ドルに成長すると予測されています。

生物学的製剤に対する需要の加速、在宅治療モデルの急速な拡大、シリアル化規制の強化がこの上昇軌道を支えています。人口動態の勢いは、欧州では65歳以上の人口が若者を上回り、使いやすく高齢者にも安全なパックのニーズが高まっていることからも明らかです。これと並行して、医薬品ブランドのオーナーは、偽造を防止するためにトレーサブルで改ざんが確認できるデザインを優先し、プライマリーパックに埋め込まれたスマートセンサーが治療のアドヒアランスを高めています。欧州連合(EU)や米国の一部の州における持続可能性規制は、バリア保護を損なうことなくリサイクル可能な単一素材構造をブランドオーナーに押し付けています。不安定なポリマー原料価格と医療用ガラス生産能力の制約がコスト面での逆風となっているが、地域生産拠点への継続的な投資が供給リスクを緩和しています。

世界のヘルスケア包装市場の動向と洞察

セルフケア・在宅診断機器の需要急増

糖尿病治療機器への年間医療技術資本支出は2024年に70億9,000万米ドルに達し、そのうち27億米ドルは小売対応無菌包装を必要とする持続グルコースモニターに充当されます。BDのPIVO ProとMiniDrawの発売は、各ブランドが病院レベルの無菌性を確保しつつ、通信販売に適したサイズの開封防止パウチをどのように指定しているかを示しています。メドトロニックのFDA認可のInPen-Simplera Smart MDIシステムは、包装が薬剤だけでなく、組み込まれた電子機器やコンパニオンアプリも保護しなければならないことを強調しています。したがって、ヘルスケア包装市場は、小児用でありながら高齢者にも優しいクロージャー、センサー用の多層キャビティ、遠隔医療ワークフローに適合するQR対応説明書などに軸足を置いています。在宅介護の普及が進むにつれ、ヘルスケア包装市場は力強い成長の弧を描いています。

シリアライゼーションと偽造防止の義務化

米国では2024年11月にDSCSAが完全施行され、データ交換におけるエラー率は最大30%に達し、コードが不一致の場合、1日あたり11万パックを隔離する危険性があります。BDのiDFill RFIDシリンジは、プライマリーレベルに識別子を埋め込むことで、企業がセカンダリーラベルを省略し、ラインスピードを加速できることを示しています。欧州のFMD規則は、人間と機械が読み取り可能な二重コードを要求しており、ヘルスケア包装市場をデジタル・インフラ投資へとさらに押し上げています。シリアライゼーションの複雑化に伴い、ハードウェア、ソフトウェア、有効なクラウドサービスをバンドルできるサプライヤーがシェアを拡大します。

石油系樹脂の価格変動

LyondellBasellのヒューストン製油所の操業停止とFormosaの新ポリプロピレンプラントの稼働により、プロピレンの供給が逼迫し、Argusは2025年に2桁の価格上昇を予想しています。エンジニアリング樹脂コストは2025年3月に再び上昇し、コンバーターのマージンを侵食しました。FDA認可の材料コードに縛られているヘルスケアブランドは、樹脂をすぐに切り替えることができないため、小規模のコンバーターは流動性不足に直面しています。ヘルスケア包装市場では、大手企業が長期ヘッジとマルチソーシングを利用してボラティリティを鈍らせる一方、バリア不良のリスクを冒すことなくダウンガウジングを可能にする、よりバリア性の高いモノPPラミネートを評価しています。

セグメント分析

2024年のヘルスケア包装市場シェアは引き続きプラスチックが70.12%を占め、比類のないコスト効率と柔軟な加工窓を反映しています。逆にガラスは、ゼロイオン溶出容器を必要とする生物製剤に後押しされ、10.42%のCAGRで前進しています。ショットファーマの3億7,100万米ドルを投じたノースカロライナ工場は、401人の雇用を創出し、GLP-1注射剤用のホウケイ酸塩シリンジ生産能力を拡大する予定であり、プレミアムバイアルに対する長期的な信頼を証明するものです。高価値ガラス製バイアル、カートリッジ、シリンジのヘルスケア包装市場規模は、mRNA、遺伝子編集、細胞治療が臨床から撤退するにつれて拡大すると思われます。

吸入器、フレキシブル点滴バッグ、点眼器では先端プラスチックが優位を保っているが、特定のフッ素樹脂コーティングに対するPFAS規制により、樹脂配合業者は新たなバリア化学物質の開発を余儀なくされています。TekniPlex社のリサイクル可能な透明ブリスターラミネートのようなハイブリッド・ソリューションは、PETとEVOHを組み合わせることで、従来はホイルにのみ使用されていた水蒸気透過性の目標を達成します。板紙は、EUのリサイクル義務化により、二次包装では前進しているが、一次医薬品接触層への浸透はまだ限定的です。加圧式ドラッグデリバリー用エアロゾルでは金属が引き続き使用されているが、欧州市場では推進剤の段階的廃止が進み、現在初期試験が行われている藻類ベースのバイオマテリアルに白羽の矢が立っています。原材料の多様化により、市場情勢は、治療クラスが容器の選択を左右するような微妙な状況になっています。

ボトルと容器は2024年のヘルスケア包装市場で40.21%のシェアを維持するが、ブリスターパックはCAGR 8.67%で先行します。Amcor社のリサイクル対応AmSkyシステムは、PVCからHDPEに置き換え、温室効果ガス排出量を70%削減しながらも、湿気に敏感な降圧剤に求められるバリア仕様を維持しています。NFCタグを搭載したコンプライアンス・ブリスター・カードは、摂取イベントを記録し、臨床医に服薬アドヒアランス・ダッシュボードを提供します。バイアルとアンプルは依然として凍結乾燥原薬に義務付けられているが、Stevanato社のEZ-fillプラットフォームにより、ニプロは交換時間を80%短縮するD2FのReady-to-fillガラスバイアルを商品化しました。

ウェアラブルインジェクターと組み合わせたカートリッジは、高粘度の生物製剤を扱うために8mmの薄肉カニューレに軸足を移しています。パウチは、薄型のレターボックス出荷形式を可能にし、消費者直販の診断キットには欠かせないものとなっています。その他」のカテゴリーは、RFIDセンサー付きの乾燥剤入りパウチがスマートパックに組み込まれ、湿度異常が発生すると薬剤師に警告を発するようになり、膨張しています。結局のところ、ヘルスケア包装市場は、分子の感受性、用法用量、eコマースの新たな規範によって各フォーマットの役割が決まる、フォームファクター階層を包含しています。

地域分析

北米は2024年にヘルスケア包装市場シェアの36.35%を占め、利益率の高いコーディング機器を強制するFDAのシリアル化規則がこれを支えています。サプライチェーンの混乱は続いており、プロバイダーの80%は供給不足の深刻化を予想しており、中規模システムでは年間350万米ドルのコスト増を見込んでいます。BDの25億米ドルの国内生産能力増強は、貿易の混乱からヘルスケア包装市場を守るリショアリングの論理を強調しています。しかし、医療機器に対する関税は現在25%に達しており、コンバーターはメキシコとカナダから金型を二重調達する動機付けとなっています。

アジア太平洋地域は、インド、中国、ASEANにおけるジェネリック医薬品の拡大と公的医療資金を背景に、CAGR 9.32%を記録し、最も急成長している地域です。AmcorによるPhoenix Flexiblesの買収は、インドにおけるクリーンルーム用ラミネーションの生産能力を倍増させ、現地供給へのコミットメントを示しました。日本の健康2025博覧会では、クライオバリデーションされたバイアルを必要とする再生医療パッケージングにスポットライトが当てられました。TOPPANとDNPはファイバーベースの滅菌パックを展示し、この地域がサーキュラー素材に傾いていることを示しました。

欧州は規制の変化にもかかわらず、力強い処理能力を維持しています。今後予定されているリサイクル義務化は、従来の多層フォイルに課題を突きつけているが、バイオベースのバリア層の研究開発資金を後押ししています。ドイツはガラスシリンジ生産で不釣り合いなシェアを占めているが、生産能力の制約がスペインとチェコ共和国への投資に拍車をかけています。中東・アフリカではサウジアラビアとエジプトで基礎的ジェネリック医薬品工場の拡張が続き、GMPグレードフィルムのグリーンフィールド需要が拡大します。南米は一桁台半ばの成長で、ブラジルのANVISAはカートンサイズを小さくするeリーフレットを導入し、物流コストを削減しました。これらの動きを総合すると、ヘルスケア包装の市場力学は各大陸で拡大し、多国籍コンバーターのリスクポートフォリオを多様化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- セルフケア・在宅診断機器の需要急増

- シリアライゼーションと偽造防止の義務化

- 高齢化と慢性疾患の蔓延

- サステナビリティ主導の素材代替

- 細胞・遺伝子治療用低温パッケージング

- アドヒアランス追跡用RFID/NFC付きスマートパック

- 市場抑制要因

- 石油系樹脂価格の変動

- 複数の管轄区域にまたがる複雑な廃棄物処理規則

- 医療用ガラスの生産能力ボトルネック

- コネクテッドパッケージングにおけるサイバーセキュリティリスク

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 業界間の競争

第5章 市場規模と成長予測

- 材料別

- ガラス

- プラスチック

- 紙・板紙

- 金属・箔

- 製品タイプ別

- ボトルと容器

- バイアルおよびアンプル

- カートリッジとプレフィルドシリンジ

- ブリスターパック

- パウチとバッグ

- その他の製品タイプ

- 包装レベル別

- 一次包装

- 二次包装

- 三次包装

- エンドユーザー別

- 医薬品製造

- 医療機器OEM

- 栄養補助食品とOTC

- 在宅ヘルスケア・プロバイダー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア、ニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor plc

- Gerresheimer AG

- SCHOTT AG

- Corning Incorporated

- West Pharmaceutical Services

- AptarGroup Inc.

- Becton Dickinson & Co.

- SGD Pharma

- Nipro Corporation

- Piramal Glass

- Oliver Healthcare Packaging

- Smurfit WestRock

- Sealed Air Corp.

- Sonoco Products Co.

- Catalent Inc.

- Beatson Clark PLC

- Shandong Medicinal Glass

- Sisecam Group

- Arab Pharmaceutical Glass Co.

- Stolzle-Oberglas GmbH