|

市場調査レポート

商品コード

1851526

タッキファイヤー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Tackifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タッキファイヤー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

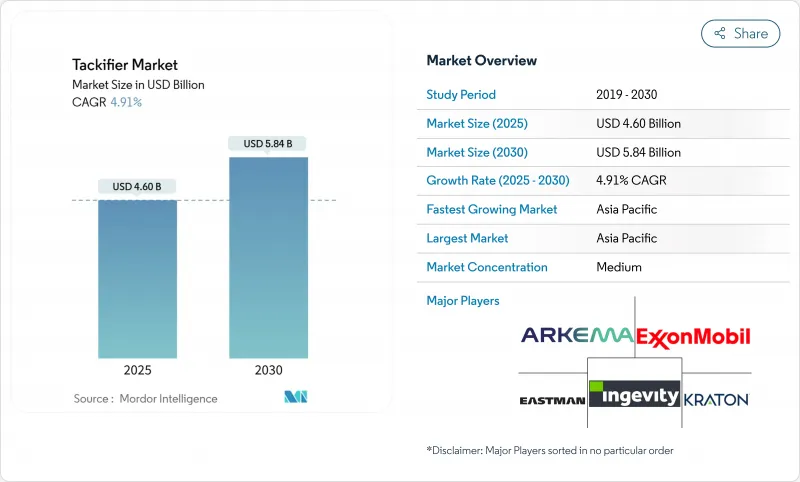

タッキファイヤー市場規模は2025年に46億米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは4.91%で、2030年には58億4,000万米ドルに達すると予測されます。

包装と衛生製品における感圧接着剤とホットメルト接着剤の持続的な需要が現在の収益を支えている一方、電気自動車のバッテリー組立、特殊建築、低VOC食品包装での使用拡大が将来の成長経路を広げています。アジア太平洋地域の急速なインフラ投資、北米と欧州の厳しい排出規制、バイオベース材料へのブランドオーナーのコミットメントなどが、市場の勢いを強めています。超低VOCグレード、高熱炭化水素樹脂、ロジン由来ディスパージョンなどのイノベーションにより、サプライヤーは接着性能を犠牲にすることなく、食品接触規制や環境規制の強化に対応することができます。タッキファイヤーフリーの反応性ホットメルトやダイナミックなポリウレタン化学への技術シフトは、原油価格の変動と並んで、収益性を低下させながらも研究開発の多様化に拍車をかける可能性のある包括的なリスクとして残っています。

世界のタッキファイヤー市場の動向と洞察

包装・衛生分野におけるホットメルト・PSA接着剤需要の増加

eコマースの小包量と高級衛生用品の組み合わせにより、ホットメルト接着剤と感圧接着剤の消費は引き続き増加しています。タッキファイヤー樹脂は、これらの高速生産ラインが必要とする、重要な初期つかみ強度と持続的な剥離強度を提供します。H.B.Fuller社のFull-Care 6217は、処方の微調整により、剥離性を向上させながら接着剤の使用量を20%削減できることを示しています。生分解性ロジン樹脂は、ブランドの持続可能性の誓約に沿い、紙を裏打ちしたテープで人気を集めています。フェミニンケア用パッドの水分管理機能により、サプライヤーは高湿度に耐えながらも臭いを抑える粘着剤を求めるようになります。エクソンモービルのEscorezポートフォリオは、透明性が最重要視される透明包装用フィルムに、淡色で熱安定性の高いグレードが求められていることを示しています。このような複合的なニーズにより、タッキファイヤー市場は2030年まで消費財の成長としっかりと結びついています。

APACの都市インフラ・ブームが建築用接着剤に拍車をかける

中国、インド、ASEAN諸国の大量輸送路線、空港、手頃な価格の住宅計画が、床材、屋根材、パネル接着剤の長期的な需要を支えています。湿気硬化型システムは熱帯の湿度において優れており、タッキファイヤー樹脂の初期ウェットアウトへの依存が販売量を増加させる。Master Builders Solutions社は、このような製品を強みに、2028年までにインドで500カロールインドルピーの売上を目指しています。軽量複合ファサードやサンドイッチパネルを推進する建築基準法は、熱安定性を提供する合成炭化水素系粘着剤の性能ウィンドウを広げています。中国粘着テープ協議会(China Adhesive Tape Council)は、建築用テープの数量増加を報告し、インフラと耐久消費財がいかに交差しているかを強調しています。これらの投資は、APACのタッキファイヤー市場成長におけるリーダーシップを維持しています。

石油・飼料価格の変動が炭化水素樹脂のマージンを圧迫

炭化水素のタッキファイヤーラインは、C5とC9ストリームがナフサクラッカーの製品別であるため、原油価格の変動を反映しています。価格高騰はマージンを悪化させ、設備投資を停滞させ、研究開発予算を制約します。2021年の欧州の物流逼迫時には、接着剤需要が5%減少し、供給途絶に対する脆弱性が浮き彫りになりました。スペシャリティケミカルのプランナーは現在、ヘッジと機動的な価格設定手段を重視しているが、小規模な独立系樹脂メーカーは依然としてリスクにさらされています。石油樹脂のシェアは65.45%を占めており、変動が拡大すれば、競合情勢を再構築し、バイオベースグレードにバイヤーを誘導する可能性があります。

セグメント分析

石油樹脂は2024年の売上高の65.45%を占め、信頼できる品質と価格性能のバランスでタッキファイヤー市場を支えています。C5-C9ハイブリッドは自動車内装や工業用テープのタックと耐熱性を確保します。一方、ロジングレードは、コンバーターがエコラベルや認定コンポスタブルパウチのために再生可能な含有量を追求するにつれて、CAGR 5.15%で拡大します。トール油ロジンの供給は、バイオ燃料精製業者が同じ原料プールから調達するため逼迫し、2030年までに8%の供給不足が予測されます。成功しているサプライヤーは、炭化水素系とロジン系を多様化し、価格変動をヘッジしながら、ブランドの持続可能性目標を達成しています。テルペン樹脂は、ニッチではあるが、天然ゴムや弾性基材との接着性を向上させる極性の利点を持っています。タッキファイヤー市場は、配合者がコスト、性能、グリーン含有量のバランスを取れるようにする、この混合原料アプローチから利益を得ています。

石油生産者は、安定性を保つために長期契約を結ぶことを目指すが、顧客がバイオ含有量に重点を置いた場合、そのような契約は柔軟性を低下させる。逆に、ロジンのイノベーターは、透明包装フィルムに要求される色や臭いの基準に適合させるために、水素添加の改良を利用しています。コスト変動と持続可能性に関する法律の相互作用が、今後10年間の原料戦略を決定します。

固形チップとペレットは2024年の売上高の81.56%を占めたが、これはコンバーターが供給が容易で粉塵が少なく、確立されたホットメルト装置との適合性を好むためです。150℃を超える溶融ピークにも酸化劣化することなく耐えるため、カートン・シーリングラインや木工ラインには欠かせないです。樹脂ディスパージョンはCAGR 5.32%で上回り、ラベルやフレキシブルラミネートにおける水性接着剤の成長に対応しています。これらのディスパージョンはVOC排出量を削減し、ラインのクリーンアップを簡素化します。リキッドタイプは、常温粘度が必要なリボンコートや溶剤システムに使用されるが、溶剤削減コストの中で市場シェアは低迷しています。メーカーにとって、マルチフォームのポートフォリオを提供することは、スイッチングの障壁を高め、カスタマイズされた粘度プロファイルを必要とする特殊な最終用途でのシェアを確保することになります。

地域分析

アジア太平洋は2024年の売上高の36.25%を占め、インフラ投資、コマースの急増、紙おむつの普及拡大に支えられ、CAGR 5.50%で成長します。中国の粘着テープ生産は、差別化された粘着剤を指定する建設やエレクトロニクスの垂直分野と連携し、1桁台の高い伸びを示しました。2025年に20,000カロールインドルピーとなるインドの建設用化学品市場は、建築サイクルを加速させる接着剤に対する地域的な需要を裏付けています。生分解性包装を支持する政府の政策がロジンベースの需要を押し上げる一方、トール油の供給が不安定なため、地元の配合業者が安定した原料を確保することが課題となっています。

北米は、厳しいVOC規制とFDAの食品接触規則により、超低臭気グレードの購入に舵を切っており、技術革新の主導権を維持しています。米国とメキシコでは自動車の電動化が進み、バッテリーセルスタックを保護する高熱合成樹脂の需要が高まっています。欧州は循環型経済目標とREACH遵守を重視し、コスト上昇にもかかわらずバイオ含有粘着付与剤に軸足を移しています。欧州の建築用接着剤の2025年の回復は、規制による逆風が持続可能な代替機会と共存できることを示唆しています。

南米と中東・アフリカは、規模は小さいもの、物流回廊、消費財の成長、製造業への海外直接投資に関連した上昇余地があります。サンゴバンによるFOSROCの10億2,500万米ドルの買収は、GCC諸国とインドにおける建築用接着剤の流通を強化するもので、グローバル企業が新興の需要センターに戦略的な賭けをする一例です。為替レートの変動と現地の樹脂生産能力の限界は当面の成長を抑制するが、緩やかな工業化により、今後10年間のタッキファイヤー普及の基盤が整う。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 包装・衛生分野におけるホットメルト接着剤とPSA接着剤の需要増加

- アジア太平洋地域の都市インフラ・ブームが建築用接着剤に拍車をかける

- eコマースの成長がテープ・ラベル消費を加速する

- 超低VOC、食品接触対応の樹脂グレードが選好されるようになる

- 高熱タッキファイヤーを必要とするEVバッテリーと軽量自動車アセンブリ

- 市場抑制要因

- 石油原料価格の変動が炭化水素樹脂のマージンを悪化させる

- タッキファイヤーフリーの反応性ホットメルトシステムの出現

- トール油とガムロジンの供給を制約している持続可能性認証

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 原料別

- ロジン樹脂

- 石油樹脂

- テルペン樹脂

- 形態別

- 固体

- 液体

- 樹脂分散

- タイプ別

- 合成

- 天然

- 用途別

- テープとラベル

- 組立

- 製本

- 履物、皮革、ゴム

- その他の用途

- エンドユーザー産業別

- パッケージ

- 建築・建設

- 自動車

- 不織布

- フットウェア

- その他のエンドユーザー産業

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Arakawa Chemical Industries, Ltd.

- Arkema

- Eastman Chemical Company

- Exxon Mobil Corporation

- Henkel AG & Co. KGaA

- Ingevity Corporation

- Kolon Industries, Inc.

- Kraton Corporation

- Lawter, a Harima Chemicals, Inc. Company

- Natrochem, Inc.

- SI Group, Inc.

- Teckrez, Inc.

- TWC Group

- Yasuhara Chemical Co., Ltd.